|

|

|

|

|||||

|

|

|

Stride (LRN) stock has surged 35% in 2025 to new all-time highs as Wall Street clamors for its growth and ability to stay out of the tariff war.

The rapidly growing digital education company is far from a one-hit wonder, with Stride up 760% in the past 10 years to blow the S&P 500’s 174%. Despite long-term outperformance and breakout to new highs, it trades at a massive discount to its peaks in terms of forward earnings.

Stride is adapting alongside the changing economy and education system, ripping off a huge stretch of earnings and revenue growth in the past several years. LRN’s earnings outlook has jumped recently, earning it a Zacks Rank #1 (Strong Buy).

Now might be a good time to consider buying Stride ahead of its third quarter fiscal 2025 earnings release after the closing bell on Tuesday, April 29.

Stride’s digital education services attract students of all ages in the U.S. and globally. LRN’s growing portfolio serves K–12 students and parents, adult learners, school districts, businesses, the military, and beyond.

Stride is expanding as more people dive into digital education and re-evaluate college amid skyrocketing costs. Stride is gaining steam in its career learning segment, especially from its Middle - High School cohort.

The next-generation education firm is capitalizing on the digitalization of the U.S. economy. The firm offers courses such as MedCerts to help people land a new career in healthcare or IT. Meanwhile, its Tech Elevator program helps “students fully transition to a career as a software developer” and boasts a 90% job placement rate.

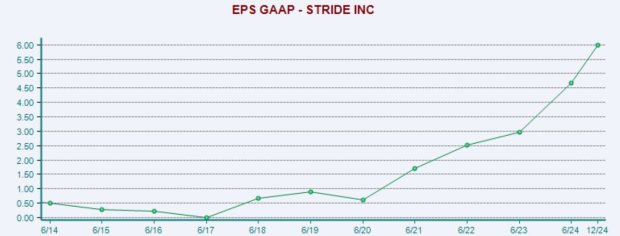

Stride grew its revenue from $400 million in 2010 to $2.04 billion in FY24. The tech education firm grew its revenue by an average of 10% in the trailing three years following a 48% Covid-boosted expansion.

The top-line growth was outmatched by its massive earnings boom, with GAAP EPS up 58% last year (+17% in FY23, +47% in FY22, and +182% in FY21).

Most recently, Stride grew its Q2 FY25 revenue by 16% and its earnings by 32%. Second quarter enrollments averaged 230.6K, up 19% YoY, with Career Learning enrollments 31% higher.

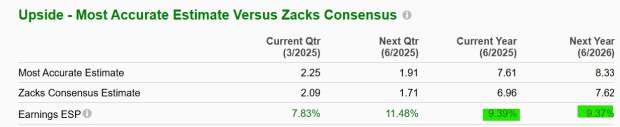

Stride is projected to grow its sales by 15% in FY25 and 7% in FY26. LRN is expected to expand its adjusted EPS by 48% and 10%, respectively.

Stride’s earnings outlook has climbed since its last release, and its Most Accurate Estimates came in well above consensus to help it land a Zacks Rank #1 (Strong Buy).

Stride stock has more than quadrupled the S&P 500 over the last decade and the past five years, including a 230% charge in the past 24 months.

LRN shares have surged 35% in 2025 to blow away the S&P 500’s -7% drop. Wall Street has continued to jump into the digital education standout because its business should remain as resilient to tariffs as possible. An economic shakeup and uncertainty might even drive more people to pursue more education.

Despite trading right near its peaks in terms of stock price, Stride trades at a 67% discount to its highs and 16% below its 10-year median at 19.4X forward 12-month earnings

Stride is growing its reach through expanded offerings in the rapidly evolving world of education, where more people are turning to digital education across different ages and demographics. LRN’s sturdy balance sheet supports its growth prospects.

The stock might be overheated in the near term. But if it can impress Wall Street with strong guidance, it could break out to fresh all-time highs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-17 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-10 | |

| Feb-08 | |

| Feb-08 | |

| Feb-05 | |

| Feb-04 | |

| Feb-04 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Feb-02 | |

| Jan-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite