|

|

|

|

|||||

|

|

|

Earnings season is in full swing, with this week’s reporting docket notably stacked. Among the bunch are a few Mag 7 members, including Microsoft MSFT and Meta Platforms META.

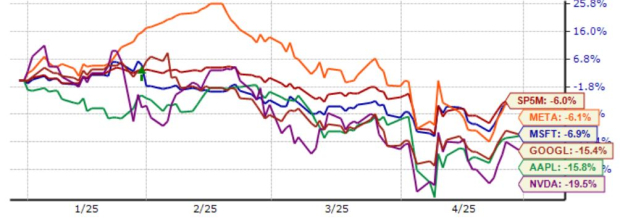

The broader Mag 7 trade has cooled off significantly recently, with investors reducing their exposure following massive runs and tariff uncertainty. Still, as shown below, both META and MSFT have weathered the storm the best, with shares of each reflecting the highest defense out of the bunch YTD.

But how do quarterly expectations stack up? Let’s take a closer look.

Down roughly 20% over the last three months, META shares have reflected big-time underperformers relative to the S&P 500. Shares did see a positive reaction following its latest quarterly release, but the above-mentioned tariff/economic worries stopped the fun shortly after.

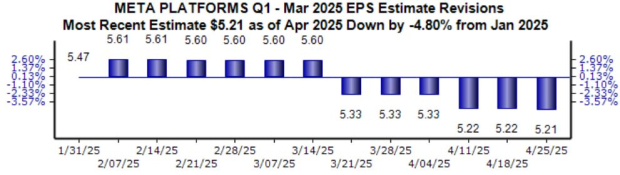

Analysts have taken their EPS expectations lower for the quarter to be reported over recent months, with the current $5.21 Zacks Consensus EPS estimate down nearly 5% since the beginning of February.

Top line expectations haven’t budged, with META forecasted to see 11% EPS growth on 13% higher sales.

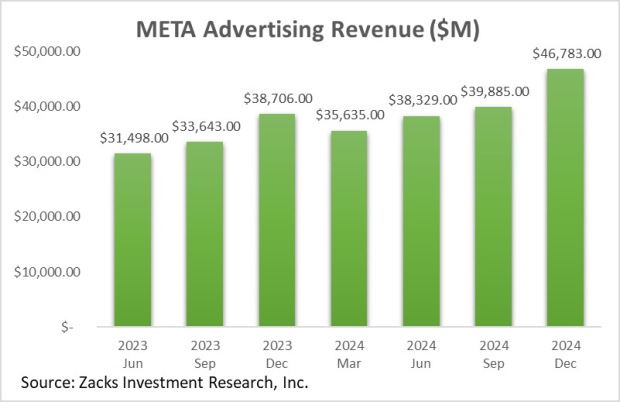

As usual, Advertising results will be a heavy focus, which account for the bulk of META’s revenues overall. For the quarter, the Zacks Consensus Estimate for Advertising sales stands at $40.4 billion, a 13.4% increase compared to the same period last year.

Below is a chart illustrating the company’s ad revenue on a quarterly basis.

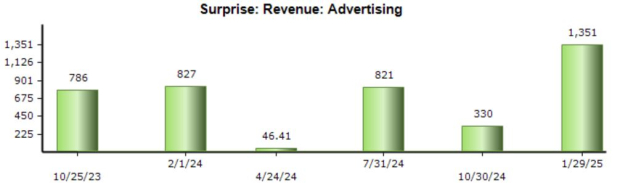

And as shown below, the results have regularly blown away our consensus estimates, with META delivering six consecutive beats.

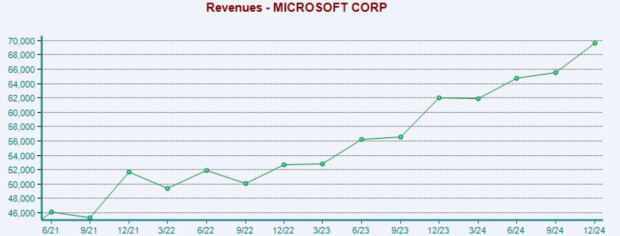

Both top and bottom line expectations for MSFT haven’t budged over recent months, reflecting an overall stable revisions trend relative to META. Current consensus expectations allude to 9% EPS growth on 11% higher sales, continuing the tech titan’s growth pace nicely.

Below is a chart illustrating the company’s sales on a quarterly basis.

Microsoft’s Intelligent Cloud results, which encompass Azure and other server products, will be an important focus as usual. The Zacks Consensus Estimate for Intelligent Cloud sales stands at $26.1 billion.

It’ll be interesting to see what the tech titan says concerning the cloud outlook, which will likely dictate the post-earnings move. Given recent market anxiety, it’ll likely need to deliver a sizable beat paired with positive guidance to wake investors back up.

Further, the CapEx picture remains a big focus among investors due to its massive spend on data center buildouts amid the AI frenzy. Interestingly, the company has dialed back some of its plans here already, and we’ll likely hear further information concerning the development in the release.

Bottom Line

The 2025 Q1 earnings cycle picks up notable steam this week, with several Mag 7 members headlining the reporting docket. Meta Platforms META and Microsoft MSFT are a part of the group, with both stocks reflecting the strongest Mag 7 performers YTD.

Concerning META, the advertising results remain key, which have shown great growth over recent periods thanks to successful AI implementations that provide users with more relevant results.

The cloud picture remains key for MSFT given the AI frenzy, with investors looking to hear positive commentary and be provided with a strong outlook given the massive amount of capital committed.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 22 min | |

| 38 min | |

| 39 min | |

| 1 hour | |

| 4 hours | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 |

Workers Are Afraid AI Will Take Their Jobs. Theyre Missing the Bigger Danger.

MSFT

The Wall Street Journal

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite