|

|

|

|

|||||

|

|

|

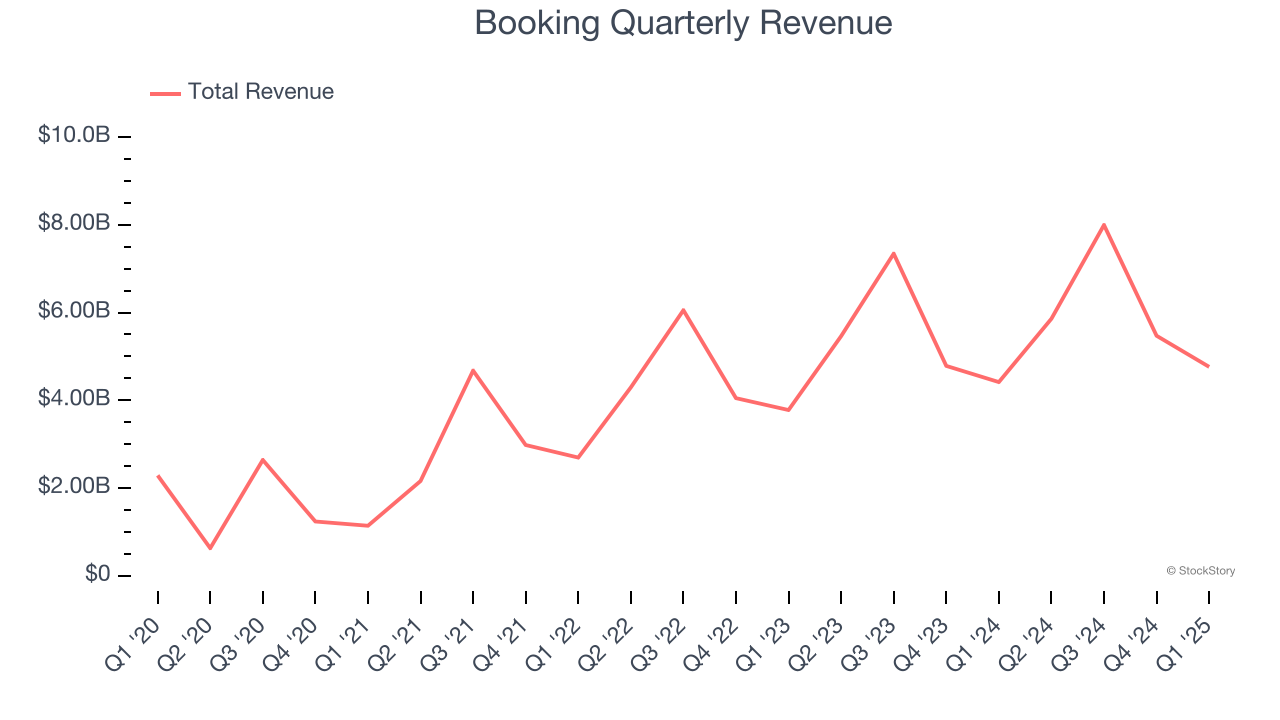

Online travel agency Booking Holdings (NASDAQ:BKNG) announced better-than-expected revenue in Q1 CY2025, with sales up 7.9% year on year to $4.76 billion. Its non-GAAP profit of $24.81 per share was 41.2% above analysts’ consensus estimates.

Is now the time to buy Booking? Find out by accessing our full research report, it’s free.

Formerly known as The Priceline Group, Booking Holdings (NASDAQ:BKNG) is the world’s largest online travel agency.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Booking grew its sales at an excellent 24.4% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Booking reported year-on-year revenue growth of 7.9%, and its $4.76 billion of revenue exceeded Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to grow 6% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

As an online travel company, Booking generates revenue growth by increasing both the number of stays (or experiences) booked and the commission charged on those bookings.

Over the last two years, Booking’s room nights booked, a key performance metric for the company, increased by 9.7% annually to 319 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

In Q1, Booking added 22 million room nights booked, leading to 7.4% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating booking growth just yet.

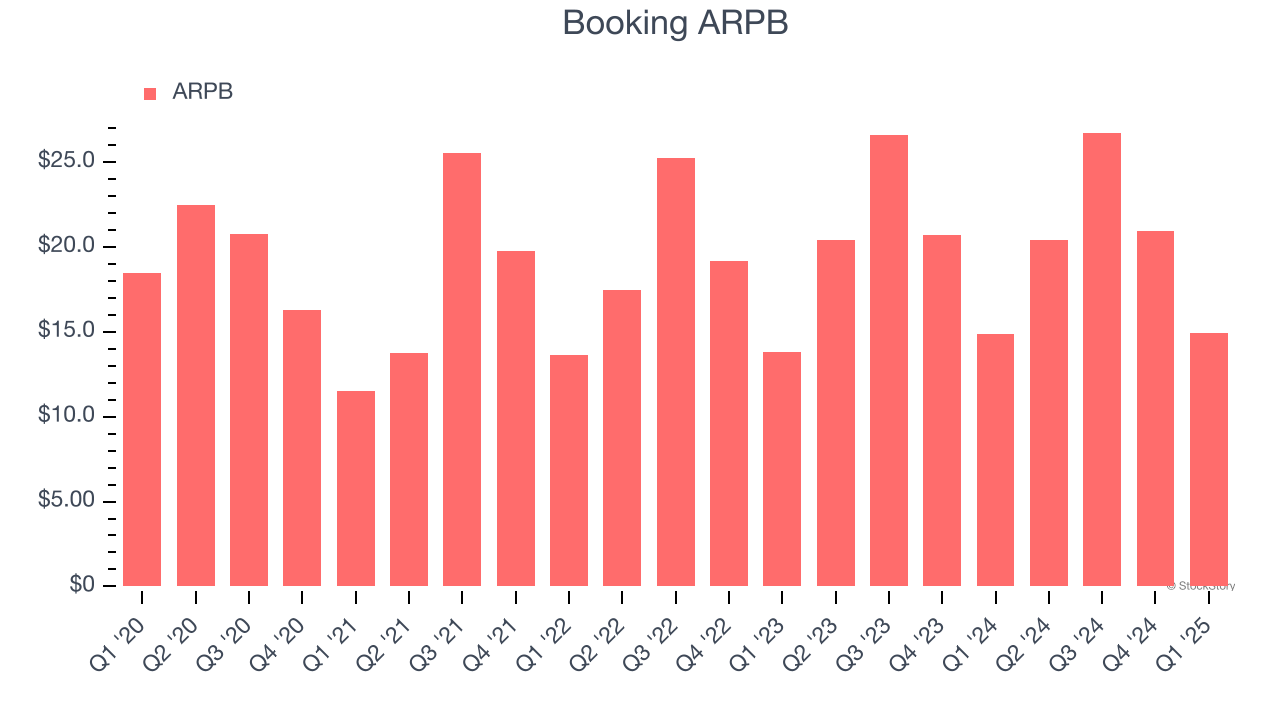

Average revenue per booking (ARPB) is a critical metric to track because it not only measures how much users book on its platform but also the commission that Booking can charge.

Booking’s ARPB growth has been decent over the last two years, averaging 5%. Its ability to increase monetization while effectively growing its room nights booked demonstrates the value of its platform.

This quarter, Booking’s ARPB clocked in at $14.93. It was flat year on year, worse than the change in its room nights booked.

We liked how Booking beat analysts’ revenue and EBITDA expectations this quarter. Despite the solid results, management called out "uncertainty in the market around the near-term geopolitical and macroeconomic environment." Shares traded down 3.6% to $4,740 immediately following the results.

So do we think Booking is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| 4 hours | |

| 6 hours | |

| 12 hours | |

| 13 hours | |

| 13 hours | |

| 13 hours | |

| 14 hours | |

| 19 hours | |

| 19 hours | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite