|

|

|

|

|||||

|

|

|

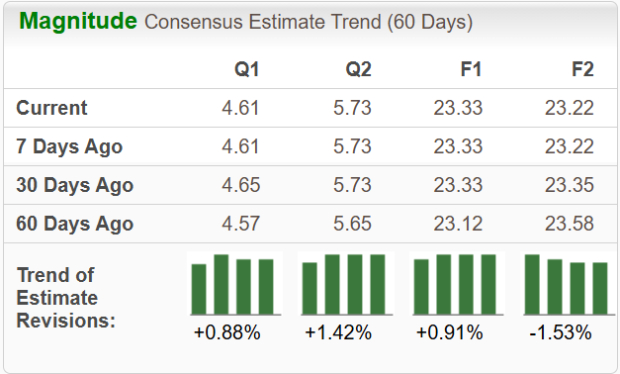

Jazz Pharmaceuticals JAZZ is set to report first-quarter 2025 earnings on May 6, after market close. The Zacks Consensus Estimate for the quarter’s sales and earnings is pegged at $978.6 million and $4.61 per share, respectively. The company’s earnings estimates for 2025 have risen from $23.12 per share to $23.33 in the past 60 days. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar)

Jazz Pharmaceuticals’ performance has been pretty decent, with its earnings exceeding expectations in three of the trailing four quarters while missing the mark on one occasion. It delivered a trailing four-quarter average earnings surprise of 3.20%. In the last reported quarter, the pharma giant delivered an earnings surprise of 13.99%.

Per our proven model, companies with the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) have a good chance of delivering an earnings beat. This is not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Jazz Pharmaceuticals has an Earnings ESP of -2.75% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Jazz reports financial figures under two segments — Neuroscience and Oncology.

The company derives a substantial portion of its revenues from the sale of its neuroscience drugs, especially the sleep disorder drug Xywav and the cannabidiol (CBD) drug Epidiolex. The Zacks Consensus Estimate for neuroscience product sales is pegged at $649 million, while our estimate for the same is pinned at $620 million.

Xywav sales have been rising in recent quarters, driven by encouraging uptake of the drug in narcolepsy and idiopathic hypersomnia (IH) indications. This trend is likely to have continued in the to-be-reported quarter. The Zacks Consensus Estimate for Xywav sales is pegged at $372 million, while our estimate for the same is pinned at $355 million.

We expect Epidiolex sales to have risen during the quarter, likely driven by geographic expansion in ex-U.S. markets. The Zacks Consensus Estimate and our model estimate for the same are pegged at $234 million and $229 million, respectively.

Sales of the legacy drug Xyrem are expected to decline, mainly due to patients switching to Xywav and the launch of high-sodium oxybate authorized generics (AGs) by Amneal Pharmaceuticals AMRX and Hikma Pharmaceuticals. We expect minimal Sativex sales for the quarter.

Revenues from the oncology franchise account for a significant portion of Jazz’s top line. The Zacks Consensus Estimate and our model estimates for sales from this segment are pegged at $269 million and $272 million, respectively.

Sales of the chemotherapy drug Rylaze are expected to have been negatively impacted in the to-be-reported quarter due to a recent update to pediatric acute lymphoblastic leukemia (ALL) protocols regarding the timing of asparaginase administration. The Zacks Consensus Estimate and our model estimates for this drug’s sales are both pegged at $103 million.

We expect sales of other oncology drugs — Zepzelca, Vyxeos and Defitelio — to grow at a mid-single-digit percentage during the quarter.

Nonetheless, a single quarter’s results are not so important for long-term investors. Let us delve deeper to understand whether to buy, sell, or hold the stock at present.

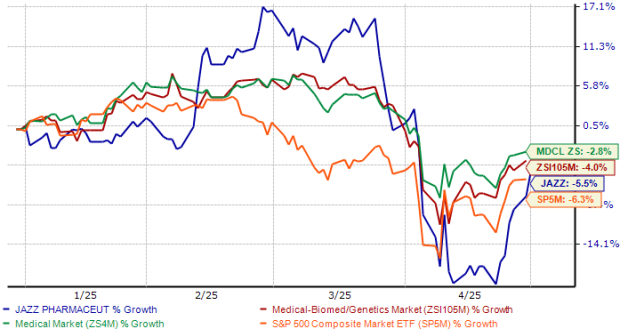

Shares of Jazz Pharmaceuticals have lost about 6% year to date compared with the industry’s 4% decline, as seen in the chart below. The stock is currently trading below its 50-day and 200-day moving averages.

From a valuation standpoint, JAZZ Pharmaceuticals is trading at a discount to the industry. Going by the price-to-sales value (P/S) ratio, the company’s shares are currently trading at 1.76, lower than 1.97 for the industry. The stock is also trading below its five-year mean of 2.70.

Jazz has built a strong portfolio that spans neuroscience and oncology. While we commend the company for diversifying beyond its oxybate portfolio and expanding into the oncology space, pipeline setbacks pose a concern. Earlier this year, Jazz decided to stop the development of suvecaltamide across both essential tremors and Parkinson's disease tremors after the drug failed to achieve the primary and key secondary endpoints in separate mid-stage studies.

The company’s strategic acquisitions have also been a key reason for its growing pipeline and expanding revenue base. Jazz currently markets five oncology products and is awaiting an FDA decision on a sixth — the glioma drug dordaviprone — expected by Aug. 18. The new drug was added to its portfolio through the recent acquisition of clinical-stage biotech Chimerix.

Despite pipeline setbacks, a diversified portfolio, rising EPS estimates for 2025 and robust cash reserve of $3.0 billion at the end of 2024 are good enough reasons to stay invested in Jazz Pharmaceuticals’ stock. Any major decline in the company’s share price could be an opportunity for long-term investors to add the stock to their portfolio. JAZZ’s shares are also currently trading at a discount to the industry.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 6 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 13 hours | |

| 13 hours | |

| 14 hours | |

| 15 hours | |

| 15 hours | |

| 16 hours | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite