|

|

|

|

|||||

|

|

|

Note: The following is an excerpt from this week’s Earnings Trends report. You can access the full report that contains detailed historical actual and estimates for the current and following periods, please click here>>>

Here are the key points:

Uncertainty about the overall macroeconomic picture continues to be a significant drag on the earnings outlook as a whole, prompting analysts to cut their estimates for the current and coming periods.

This uncertain environment makes it difficult for companies to provide explicit guidance for the coming periods. We had noted here how United Air Lines UAL had provided a two-pronged outlook, with one guidance a reiteration of their existing outlook and the second describing the earnings impact of a recessionary backdrop.

Since then, A.O. Smith AOS and 3M MMM followed United Air Lines’ lead by reiterating its outlook for the year, but 3M also provided a tariffs component that will potentially weigh on full-year EPS in the -2.5% to -5% range. A.O. Smith appears to have used price increases to offset the potential tariff impact that allowed it to maintain existing guidance. Many others have struggled with providing explicit guidance, for understandable reasons.

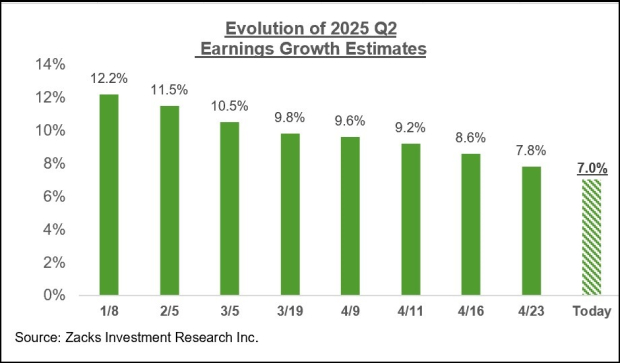

We are starting to see this in the revisions trend both for the current period (2025 Q2) and full-year 2025. The chart below shows how 2025 Q2 estimates have started coming down lately.

The chart below shows expectations for 2025 Q1 in terms of what was achieved in the preceding four periods and what is currently expected for the next three quarters.

The emerging negative revisions trend appears to be broad-based, with Aerospace and Construction as the only sectors experiencing modest positive revisions.

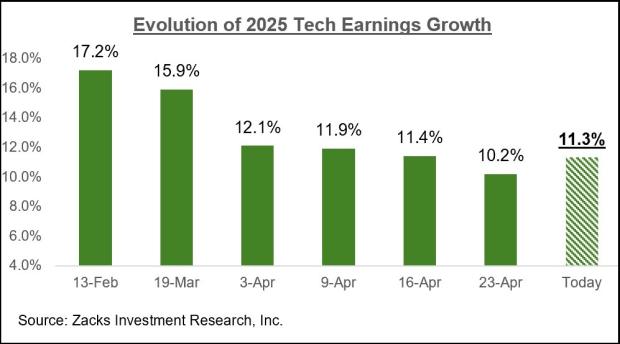

Of the sectors suffering negative estimate revisions, the case of the Tech sector is particularly significant as this sector had thus far been enjoying a very favorable revisions trend for more than a year now.

For 2025 Q2, the Tech sector is currently expected to bring in +11.7% more earnings relative to the same period last year. This growth expectation is down from +14.2% on April 2nd. For full-year 2025, the expectation is for sector earnings to increase by +11.3% from the 2024 level, a decline from the +12.1% growth expected on April 2nd. We should note, however, that estimates have modestly inched up again over the past few days.

The chart below shows how full-year 2025 aggregate earnings expectations for the sector have evolved over time.

The evolution of the Tech sector’s year-over-year earnings growth rate is shown in the chart below.

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

While estimates for this year have started coming down lately, there haven’t been a lot of changes to estimates for the next two years at this stage. The chart below should give you a sense of how rapidly this year’s estimates are getting adjusted lower.

Given all-around worries about the economy’s growth momentum, it is reasonable to expect these estimates to be lowered further in the days ahead as the tariffs impact starts showing up in data. The modestly negative GDP read for the first quarter of the year primarily reflected the anticipatory effects of the trade regime, with importers stocking up on supplies ahead of the new levies taking effect.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-09 | |

| Feb-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite