|

|

|

|

|||||

|

|

|

Leading buy now, pay later (BNPL) solution provider Affirm Holdings, Inc. AFRM is set to report its third-quarter fiscal 2025 results on May 8, 2025, after the closing bell. The Zacks Consensus Estimate for the to-be-reported quarter’s bottom line is currently pegged at a loss of 8 cents per shareon revenues of $783.1 million. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

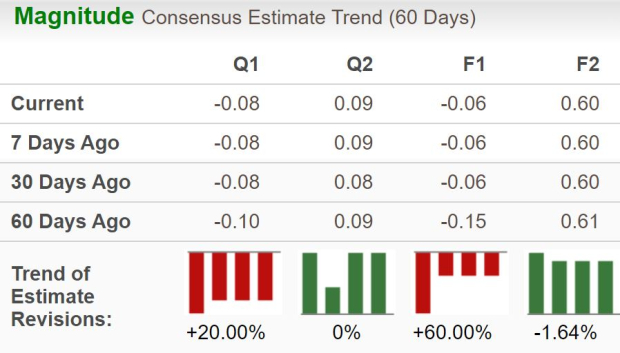

The fiscal third-quarter earnings estimate has improved by 2 cents over the past month. The bottom-line projection indicates an 81.4% year-over-year improvement. Also, the Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 35.9%.

For the current fiscal year, the Zacks Consensus Estimate for Affirm’s revenues is pegged at $3.2 billion, implying a rise of 37.1% year over year. The consensus mark for the current fiscal year’s EPS is pegged at a loss of 6 cents, implying an improvement of 96.4% on a year-over-year basis.

Affirmbeat the consensus estimate for earnings in each of the last four quarters, with the average surprise being 84.1%.

Affirm Holdings, Inc. price-eps-surprise | Affirm Holdings, Inc. Quote

Our proven model predicts a likely earnings beat for the company this time around as well. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is precisely the case here.

AFRM has an Earnings ESP of +63.27% and a Zacks Rank #1. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Let’s see how things have shaped up before the fiscal third-quarter earnings announcement.

Merchant network revenues are likely to have benefited from an expanding Gross Merchandise Volume (GMV). Also, the active merchants figure is expected to have witnessed a significant boost in the fiscal third quarter due to the company’s ability to strike deals with different businesses. The Zacks Consensus Estimate for merchant network revenues is pegged at $199.5 million, indicating a 25.2% rise from the prior-year quarter’s figure.

The consensus mark for GMV for the fiscal third quarter implies 29.2% growth from the prior-year quarter’s number. Management anticipates the metric to be in the range of $8-$8.3 billion.

An increase in the number of transactions conducted through the Affirm platform is likely to have been supported by higher active merchants and consumers. The Zacks Consensus Estimate for active consumers indicates 17.4% year-over-year growth. Also, the consensus mark for transactions per active consumer suggests a 16.5% rise from the year-ago period.

An increase in the usage of Affirm’s virtual cards is expected to have driven card network revenues. The consensus mark for card network revenues indicates a 30% improvement from the year-ago quarter’s number. Meanwhile, the Zacks Consensus Estimate for interest income is pegged at $414.4 million, which implies a 31.3% year-over-year rise.

A growing off-balance sheet platform portfoliois likely to have contributed to the rise in servicing income. The consensus mark for servicing income is pegged at nearly $31.3 million, which indicates a 23.6% jump from the year-ago quarter. However, the quarterly results are likely to have witnessed higher transaction costs. The company expects transaction costs to be in the range of $415-$430 million.

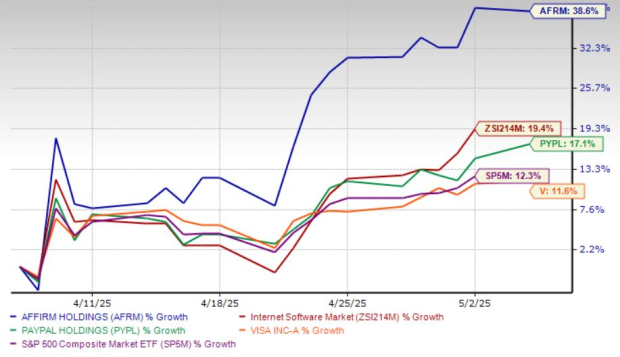

Affirm stock has exhibited an upward movement, gaining a notable percentage over the past month. It has jumped 38.6% compared with the industry’s growth of 19.4%. In comparison, PayPal Holdings, Inc. PYPL, which also has a major footprint in the BNPL space, grew 17.1% during this time. Visa Inc. V, which is a rather traditional credit and debit card solutionsprovider and a major footprint holder in the payments space, gained 11.6% in the past month. Meanwhile, AFRM stocks have outperformed the S&P 500 significantly, which has increased 12.3%.

Now, let’s look at the value Affirm offers investors at current levels.

Despite the share price appreciation, the company’s valuation looks relatively cheap compared with the industry average. Currently, AFRM is trading at 4.34X forward 12-month sales, below the industry’s average of 5.12X. So, there’s more room to grow.

Meanwhile, PayPal and Visa stocks are currently trading at 1.99X and 15.4X forward P/S.

The delay of Klarna’s IPO due to a broader tech sell-off and tariff-related uncertainties was a near-term win for Affirm, easing competitive pressure in the crowded BNPL space. Without Klarna raising fresh capital or drawing investor attention, Affirm stands to benefit as one of the few publicly traded BNPL players. Additionally, analysts expect concerns about Walmart dropping Affirm have been overblown; the retailer only contributed 5% to Affirm’s GMV and 2% of adjusted operating income in the second half of last year, and this allowed AFRM to avoid entering any unprofitable deal.

Affirm’s long-term outlook remains promising. The company is expanding internationally, entering the U.K. as a gateway to Europe, and is diversifying beyond BNPL with new debit products and banking features. These initiatives position it to compete with giants like Visa and PayPal. Crucially, Affirm is now focused on profitability, tightening underwriting standards and improving margins, a feat that should bolster investor confidence and support its case for durable growth. With strong momentum, a potential earnings beat on the cards, and an appealing valuation, Affirm stock presents a compelling buying opportunity for investors right now.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 40 min | |

| 3 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite