|

|

|

|

|||||

|

|

|

Chipotle Mexican Grill, Inc. CMG shares have climbed 9.6% following the release of its first-quarter 2025 results, reflecting investor confidence in the company's long-term strategy despite near-term challenges.

While the quarter was impacted by macroeconomic headwinds, including adverse weather and cautious consumer spending, Chipotle demonstrated resilience and operational momentum. The company continued to elevate its restaurant performance through strategic enhancements, including innovations in kitchen efficiency and digital throughput. Notably, CMG expanded its footprint in both domestic and international markets, reinforcing its growth narrative.

A key highlight of the quarter was the successful debut of Chipotle Honey Chicken, which resonated well with customers, and contributed to a noticeable uptick in guest traffic and incremental transactions across the system.

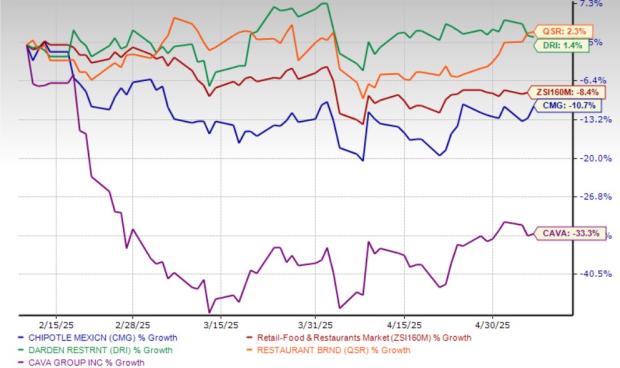

Closing at $51.64 in the last trading session, the stock stands 25.4% below its 52-week high of $69.26. Technically, CMG is trading above its 50-day moving average. In the past three months, the company’s shares have declined 10.7% compared with the industry’s fall of 8.4%. In the same time frame, shares of other industry players like Darden Restaurants, Inc. DRI have inched up 1.4% and Restaurant Brands International Inc. QSR has gained 2.3%, while CAVA Group, Inc. CAVA has moved down 33.3%.

The launch of Chipotle Honey Chicken in March was a standout.. Management highlighted it as the brand’s best-performing limited-time offer to date. The company plans to intensify marketing efforts through summer and beyond to elevate brand visibility and cultural relevance. These campaigns are expected to drive consumer engagement and support sales recovery in the second half of the year.

CMG has been indulging in investments that align with its digital innovation aspects and allow it to cater to the demands of its customers efficiently. Chipotle is actively rolling out back-of-house equipment enhancements designed to streamline prep and boost consistency without compromising quality. Innovations include a produce slicer for uniform cuts and an equipment package featuring a dual-sided plancha, high-capacity fryer and three-pan rice cooker. These upgrades are being deployed in new and existing locations, with full rollout expected over the next few years.

Chipotle is also progressing with proprietary equipment like Autocado (an avocado processing tool) and an augmented digital makeline. Both devices have gone through multiple test cycles and are currently being fine-tuned at CMG’s Cultivate Center. Autocado has returned to restaurants for further evaluation, while the digital makeline will be reintroduced later in the summer. The initiatives pave a path for enhanced kitchen efficiency and food preparation accuracy when fully deployed.

Strength in restaurant openings aided the company’s performance in the first quarter. In the reported quarter, Chipotle opened 57 restaurants in 48 locations, including a Chipotlane. It also opened two internationally licensed restaurants. New restaurant economics have been strong, with year-two cash-on-cash returns averaging around 60%. Overall, the company's cash-on-cash return stands in the low 80% range, reflecting ongoing improvements in the restaurant performance over time and supporting confidence in its long-term growth objectives.

In the Middle East, two additional restaurants were opened in February through the partnership with Alshaya Group, bringing the total to five — three in Kuwait and two in Dubai. Performance in the region continues to be strong, and the company plans to accelerate growth with Alshaya Group in the coming year.

Another partnership agreement was recently signed with Alsea, a major operator in Latin America and Europe, to open restaurants in Mexico. The first location is expected to open in early 2026, with the exploration of potential expansion into other regional markets also underway. Chipotle has opened development pipelines in Central London and Germany, and is actively scouting sites, although timelines for openings remain 18-24 months.

The company remains on track to open 315-345 locations this year, with approximately 80% featuring a Chipotlane. This includes 15-20 restaurants in Canada. Backed by impressive unit economics and the success of small-town locations, the company anticipates operating more than 7,000 restaurants in the long term in North America, with Chipotlanes.

Comparable restaurant sales in the first quarter fell 0.4% against 5.4% growth reported in the previous quarter. In the quarter, comps were hurt by lower transactions of 2.3%. However, this was partially mitigated by a 1.9% rise in average checks. Our model predicts second-quarter comps to decline 2.5% year over year.

The company, like other industry players, has been facing significant supply-chain challenges and inflation across most commodities and categories. In the first quarter of 2025, food, beverage and packaging costs, as a percentage of revenues, came in at 29.2%, compared with 28.8% in the prior-year quarter. The rise in costs was due to inflationary costs across avocados, dairy and chicken.

For the second quarter, labor costs are projected to be in the mid-24% range, with wage inflation anticipated in the low-single digits. Marketing expenses are expected to be in the mid-2% range for the second quarter and in the high-2% range for the full year. Other operating costs for the second quarter are forecast to be in the high-13% range. For 2025, our model predicts total operating expenses to rise 7.8% year over year to $10.13 billion.

Estimates for CMG’s 2025 earnings have moved down from $1.28 to $1.22 in the past 30 days. The company’s earnings in 2025 are likely to witness year-over-year growth of 8.9%. Then again, Darden Restaurants, Restaurant Brands and CAVA’s earnings for the current year are likely to witness year-over-year increases of 7%, 9.9% and 31%, respectively.

From the valuation point of view, the stock is still trading at a premium despite the recent decline. Chipotle’s forward 12-month price-to-earnings ratio stands at 39.89, significantly higher than the industry’s ratio of 25.75 and the S&P 500's ratio of 21.65. This suggests that investors may pay a high price relative to the company's expected earnings growth.

Chipotle’s recent stock rebound underscores investor optimism in the brand’s long-term prospects, driven by innovation, menu success, operational upgrades and robust unit expansion. The company continues to invest meaningfully in digital efficiency, kitchen modernization and international growth, which are expected to support stronger performance once macro pressures ease.

However, near-term headwinds, including soft comparable sales, inflationary cost pressures and difficult year-over-year comparisons, are likely to weigh on the results. Additionally, the stock remains richly valued relative to peers, limiting its near-term upside potential.

Given this backdrop, existing shareholders may benefit from holding their positions as Chipotle’s structural strengths and brand momentum remain intact. However, new investors may want to wait for a more attractive entry point aligned with improved earnings visibility and valuation support.

CMG currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 14 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Burger King is testing AI headsets that will know if employees say 'welcome' or 'thank you'

QSR

Associated Press Finance

|

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite