|

|

|

|

|||||

|

|

|

ADMA Biologics ADMA reported lower-than-expected results for the first quarter. Adjusted earnings per share of 14 cents missed the Zacks Consensus Estimate of 16 cents. Revenues of $114.8 million (up 40% year over year) also missed the Zacks Consensus Estimate of $119 million.

Consequently, the stock has plunged post the earnings announcement on May 7.

Nonetheless, the company raised its annual revenue guidance for 2025 and 2026, concurrent with the quarterly results.

A single quarter's results should not determine any investment decision. Let us delve into ADMA’s fundamentals, potential growth prospects, challenges and valuation levels to make a prudent choice.

ADMA Biologics markets plasma-derived biologics for the treatment of immune deficiencies and the prevention of certain infectious diseases.

The company’s top line currently comprises sales of three FDA-approved products — Bivigam (an Intravenous Immune Globulin [“IVIG”] product to treat primary humoral immunodeficiency), Asceniv (to treat primary immunodeficiency disease or PIDD) and Nabi-HB (to treat and provide enhanced immunity against the hepatitis B virus).

Asceniv, its lead product, is a plasma-derived IVIG that contains naturally occurring polyclonal antibodies. These antibodies are proteins used by the body’s immune system to neutralize microbes, such as bacteria and viruses, and prevent infection and disease.

Asceniv is indicated for the treatment of PIDD or inborn errors of immunity in adults and adolescents. It is manufactured using ADMA’s unique, patented plasma donor screening methodology and tailored plasma pooling design, which blends normal source plasma with respiratory syncytial virus plasma obtained from donors tested using the company’s proprietary microneutralization assay.

Demand was record high in the first quarter. Consequently, ADMA expects Asceniv’s total revenue share to expand throughout 2025 and beyond.

ADMA anticipates accelerating new patient starts and further penetration in existing institutions, which would significantly expand its peak revenue potential driven by ramp up of long-term high-titer plasma supply contracts and continued benefit in real-world patient outcomes.

ADMA expects to generate initial, proof-of-concept animal data before 2025-end for its lead R&D pipeline program, SG-001, a hyperimmune globulin targeting S. pneumonia.

ADMA believes that SG-001 has the potential to generate $300-500 million or more in high-margin annual revenues, with IP protection through at least 2037.

Along with providing first-quarter results, ADMA updated its outlook for 2025 and 2026. ADMA now expects to generate revenues of more than $500 million in 2025 and $625 million in 2026 (previous guidance: more than $490 million in 2025 and $605 million in 2026). Net income is projected to exceed $175 million in 20225 (same as before) and expected to increase to $245 million or more for 2026 (previous guidance: exceed $235 million in 2026).

ADMA recently authorized a common stock repurchase program of up to $500 million. The buyback will boost the bottom line.

Shares of ADMA have surged 37.7% year to date against the industry’s decline of 7.4%. The stock has outperformed the sector and the S&P 500 in this timeframe.

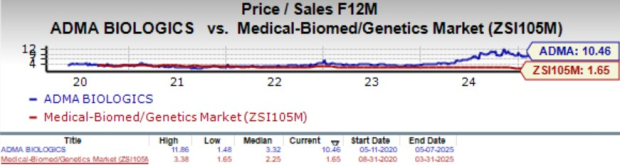

From a valuation perspective, ADMA is expensive at this moment. Going by the price/sales ratio, ADMA’s shares currently trade at 10.46x forward sales, higher than its mean of 3.32x and the industry’s 1.65x.

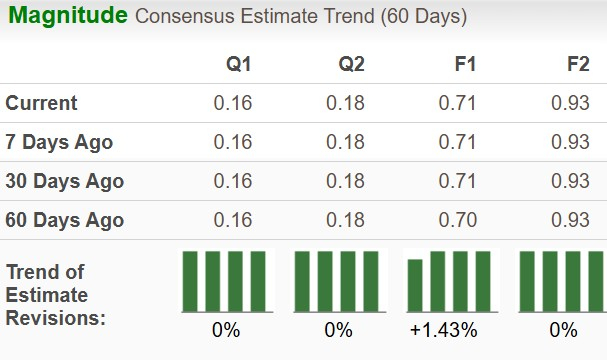

The EPS estimate for 2025 has moved north 1 cent to 71 cents but remained unchanged at 93 cents for 2026.

Large biotech companies are generally considered safe havens for investors interested in this sector. ADMA Biologics, which competes with Takeda TAK and Grifols GRFS in the U.S. market for plasma-derived products, should maintain momentum in the upcoming quarters. Incremental additional penetration of Asceniv should accelerate near-term revenue growth.

While the first-quarter performance was disappointing, the targeted market has significant growth potential. Management expects additional opportunities for ADMA to continue to grow substantially in the underserved, immune-compromised and co-morbid patient population despite the availability of standard-of-care therapy.

Additionally, ADMA conducts all its manufacturing operations, end-market sales, and customer engagements exclusively within the United States. The tariffs implemented on foreign goods, services, and manufacturing are not expected to have an impact on ADMA and its supply chain or production operations.

The recent FDA approval for its innovative yield enhancement production process supports revenue growth and margin expansion opportunities. Hence, any dip can be used as a buying opportunity. For investors already owning the stock, staying invested would be a prudent move.

ADMA currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| Jul-28 | |

| Jul-20 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-13 | |

| Jul-13 | |

| Jul-12 | |

| Jul-06 | |

| Jul-02 | |

| Jun-26 | |

| Jun-24 | |

| Jun-22 | |

| Jun-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite