|

|

|

|

|||||

|

|

|

Heritage Insurance Holdings, Inc. HRTG reported mixed first-quarter 2025 results, wherein the bottom line beat the Zacks Consensus Estimate but the top line missed the same. Net premiums earned improved 11.5%, driven by the strong performance of operating businesses. Combined ratio improved 950 basis points (bps) from the prior-year quarter’s level to 84.5.

Heritage CEO Ernie Garateix stated, “The first quarter of 2025 marked the third consecutive quarter in which Heritage was impacted by significant catastrophe losses and also generated returns to shareholders.”

This super-regional U.S. property and casualty insurance holding company is poised to gain from prudent underwriting execution and rate adequacy initiatives pursued over the last three years.

First-quarter 2025 earnings per share of 99 cents beat the Zacks Consensus Estimate by 115.2%. The bottom line surged 110% year over year. Operating revenues of $212 million improved 11% year over year but missed the consensus estimate by 1.1%.

Premiums-in-force were $1.43 billion, up 3.3% year over year. Gross premiums written were $356 million, down 0.2% year over year, reflecting exposure management trends over the last several years for personal lines business.

Net combined ratio improved, driven by a lower net loss ratio and lower net expense ratio.

Return on equity expanded 1430 basis points to 39.3%.

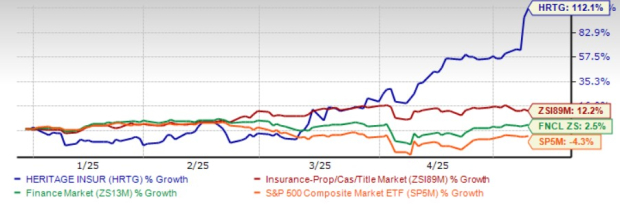

Shares of HRTG have rallied 112.1% year to date, outperforming the industry’s growth of 12.2%, the Finance sector's return of 2.5% and the Zacks S&P 500 composite’s decline of 4.3%.

Shares of HCI Group HCI and Universal Insurance Holdings UVE, two other insurers having a strong presence in Florida, have gained 32.1% and 20.8%, respectively, in the same time frame.

HCI Group is set to grow as it enters the commercial residential sector, strategic partnerships and licensing, ensuring new revenue streams, improved risk management and a stable financial position.

.

A solid market presence, technological advancement, a diversified portfolio lowering dependency on a single revenue stream, and financial stability position Universal Insurance for growth.

Shares of HRTG have been trading above its 50-day simple moving average (SMA) for some time, signaling a short-term bullish trend and making it an attractive option for investors from a technical perspective.

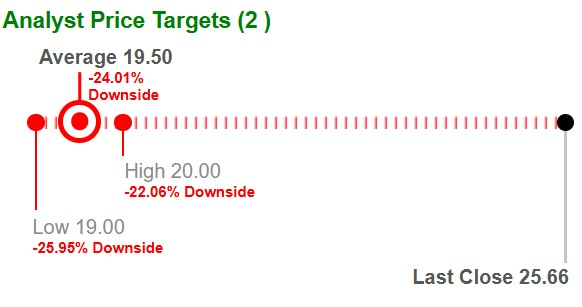

Based on short-term price targets offered by two analysts, the Zacks average price target is at $19.50 per share. The average suggests a potential 24% upside from the last closing price.

The Zacks Consensus Estimate for 2025 and 2026 implies a 20.9% and 28.6% respective year-over-year increase. It has a Growth Score of A.

Heritage Insurance is prioritizing profitability by ensuring rate adequacy, implementing profit-focused underwriting criteria, and limiting new business in saturated or low-performing markets. In response to declining returns and a tightening reinsurance market, the company stopped the issuance of new personal lines policies in Florida and the Northeast as of December 2022.

Its strategic initiatives for 2025 include re-opening profitable geographies and allocating capital to sustain profits and margins on a measured basis, focusing on rate adequacy, continuing data-driven analytics to drive exposure management, and leveraging infrastructure and capabilities to foster future growth.

The excess and surplus (E&S) segment represents a key area of growth, with Heritage Insurance actively exploring expansion into more states. Its reinsurance strategy offers robust protection against hurricane and severe weather risks in coastal regions. The insurer anticipates a significant drop in its ceded premium ratio, driven by both cost-effective improvements in its reinsurance structure and an increase in gross premiums earned. Recently, Heritage fully secured its 2025-2026 indemnity-based catastrophe excess-of-loss reinsurance program for its insurance subsidiaries.

Heritage is also channeling capital toward technology investments and high-margin business segments to support long-term growth. In addition, the insurer has approved a $10 million share buyback program as part of its efforts to return value to shareholders.

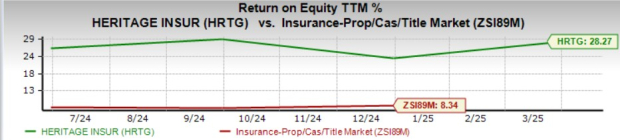

Return on equity in the trailing 12 months was 28.7%, higher than the industry average of 8.3%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders' equity.

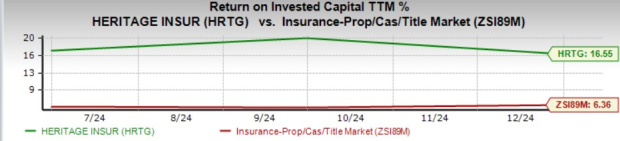

Its return on invested capital (ROIC) has been increasing for quite some time. This reflects HRTG’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 16.6%, higher than the industry average of 6.4%.

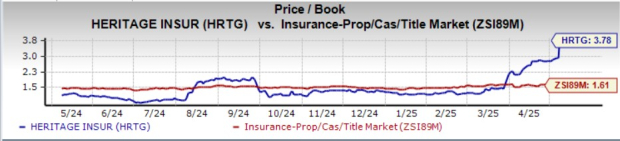

The stock is overvalued compared to its industry. It is currently trading at a price-to-book multiple of 3.78, higher than the industry average of 1.61. It has a Value Score of A.

Shares of HCI Group and Universal Insurance are trading at a multiple greater than the industry average.

A growing commercial residential business, improving E&S business, better pricing, increasing top line, expanding margins and solid earnings bode well for HRTG’s growth. Its VGM Score of A and strategic focus on accelerating growth raises optimism.

Despite premium valuation, it is worth adding this Zacks Rank #1 (Strong Buy) stock to your portfolio. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| 7 hours | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-08 | |

| Jul-08 | |

| Jun-17 | |

| Jun-01 | |

| May-28 | |

| May-28 | |

| May-08 | |

| May-08 | |

| May-07 | |

| May-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite