|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Under Armour, Inc. UAA reported fourth-quarter fiscal 2025 results, wherein both the top and bottom lines exceeded the Zacks Consensus Estimate. However, both metrics decreased year over year.

The company is laying the foundation for a more focused brand by elevating products and storytelling, tightening distribution and refining its operating model. The fourth-quarter performance supported fiscal 2025 results that surpassed initial expectations, showing clear progress in efforts to reignite brand relevance and drive sustainable, profitable growth.

Under Armour, Inc. price-consensus-eps-surprise-chart | Under Armour, Inc. Quote

The Baltimore, MD-based company reported an adjusted loss of eight cents a share, which fared better than the Zacks Consensus Estimate of an adjusted loss of nine cents. The reported figure decreased from 31 cents a share in the year-ago period. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

Meanwhile, net revenues of $1,180.6 million beat the Zacks Consensus Estimate of $1,163 million but decreased 11.4% from the prior-year quarter. The metric declined 10% on a currency-neutral basis.

Wholesale revenues fell 9.7% year over year to $767.6 million, while direct-to-consumer revenues declined 15.1% to $386.1 million. Revenues from company-owned and operated stores dipped 6%, whereas e-commerce revenues dropped 27% due to planned reductions in promotional activities. E-commerce accounted for 37% of the total direct-to-consumer business for the quarter.

By product category, Apparel revenues declined 11.1% year over year to $780.4 million, beating the Zacks Consensus Estimate of $765.8 million. Footwear revenues decreased 16.5% to $281.8 million, lagging the consensus estimate of $300.2 million. Revenues from the Accessories category rose 2.3% to $91.5 million, outperforming the consensus estimate of $80.2 million. Meanwhile, Licensing revenues dropped 14.9% to $24.2 million, falling short of the consensus estimate of $24.5 million.

Revenues from North America declined 10.7% to $689.4 million, exceeding the Zacks Consensus Estimate of $664.4 million. Meanwhile, revenues from the international business decreased 12.9% (down 10% on a currency-neutral basis) to $488.5 million.

Within the international segment, revenues from Europe, the Middle East and Africa (EMEA) decreased 1.9% year over year to $278.6 million, beating the consensus estimate of $275 million. Revenues from the Asia-Pacific dropped 27.3% to $164.8 million, lagging the consensus estimate of $174.6 million. Latin America saw a 10.3% decline to $45.1 million, lagging the consensus estimate of $50.2 million.

Under Armour reported gross profit of $550.8 million, down 8.1% year over year. The company’s gross margin expanded 170 basis points to 46.7% from the prior-year period. This was driven by supply-chain improvements such as lower product and freight costs, decreased direct-to-consumer discounting and favorable effects from product mix and foreign exchange. These gains were partially offset by an unfavorable channel and regional mix.

Adjusted selling, general and administrative expenses increased 7% year over year to $586.4 million, excluding approximately $16 million in transformation costs associated with the fiscal 2025 Restructuring Program and around $5 million in litigation settlement expenses. Adjusted operating loss was $35.6 million in the quarter under review.

UAA ended the quarter with cash and cash equivalents of $501.4 million, long-term debt (net of current maturities) of $595.1 million and total stockholders' equity of $1.89 billion.

In the fiscal fourth quarter, Under Armour repurchased $25 million worth of its class C common stock, retiring 4.1 million shares. As of March 31, 2024, 12.8 million shares were repurchased for $90 million as part of a three-year, $500-million program approved by the company in May 2024.

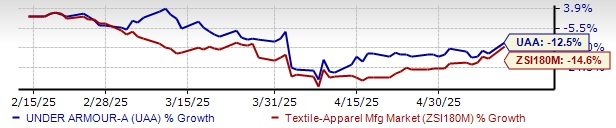

UAA Stock Past Three-Month Performance

Looking ahead to fiscal 2026, Under Armour remains focused and agile, supported by its shift to a category-led operating model to navigate a challenging macroeconomic and trade environment. Due to ongoing uncertainty, the company provided guidance only for the first quarter.

For the first quarter of fiscal 2026, Under Armour expects revenues to decline four-five percent compared with the same period in fiscal 2025. This projection includes a four-five percent drop in North America, high single-digit growth in the EMEA region and a mid-teen percentage decrease in Asia-Pacific.

The gross margin is expected to expand 40-60 basis points year over year, supported by a more favorable product mix, lower product and freight costs, and positive foreign exchange effects. These gains are anticipated to be partially offset by a less favorable channel and regional mix, as well as the impact of tariffs.

Selling, general and administrative expenses are projected to decline approximately 40 percent compared with the prior-year quarter, which included a $274 million litigation settlement. Excluding last year’s settlement and expected transformation costs from the fiscal 2025 Restructuring Plan, adjusted SG&A is expected to show slight leverage.

Operating income is forecasted to be in the range of $5-$15 million, with adjusted operating income, excluding restructuring and transformation expenses, expected between $20 million and $30 million. Loss per share is projected to be between break-even and two cents, while adjusted earnings per share are expected to be between one cent and three cents.

This Zacks Rank #3 (Hold) stock has lost 12.5% in the past three months compared with the industry’s decline of 14.6%.

Some better-ranked stocks are G-III Apparel Group, Ltd. GIII, Stitch Fix SFIX and Canada Goose GOOS.

G-III Apparel is a manufacturer, designer and distributor of apparel and accessories. It has a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for G-III Apparel’s fiscal 2025 earnings and revenues indicates a decline of 4.5% and 1.2%, respectively, from the fiscal 2024 reported levels. GIII delivered a trailing four-quarter average earnings surprise of 117.8%.

Stitch Fix delivers customized shipments of apparel, shoes and accessories for women, men and kids. It currently has a Zacks Rank of 2.

The Zacks Consensus Estimate for SFIX’s fiscal 2025 earnings implies growth of 64.7% from the year-ago actual. SFIX delivered a trailing four-quarter average earnings surprise of 48.9%.

Canada Goose is a global outerwear brand. GOOS is a designer, manufacturer, distributor and retailer of premium outerwear for men, women and children. It carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for Canada Goose’s current fiscal year’s earnings and revenues implies a decline of 1.4% and 4.9%, respectively, from the year-ago actuals. Canada Goose delivered a trailing four-quarter average earnings surprise of 71.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite