|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Since November 2024, AECOM has been in a holding pattern, posting a small return of 0.9% while floating around $109.77.

Is there a buying opportunity in AECOM, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're sitting this one out for now. Here are three reasons why you should be careful with ACM and a stock we'd rather own.

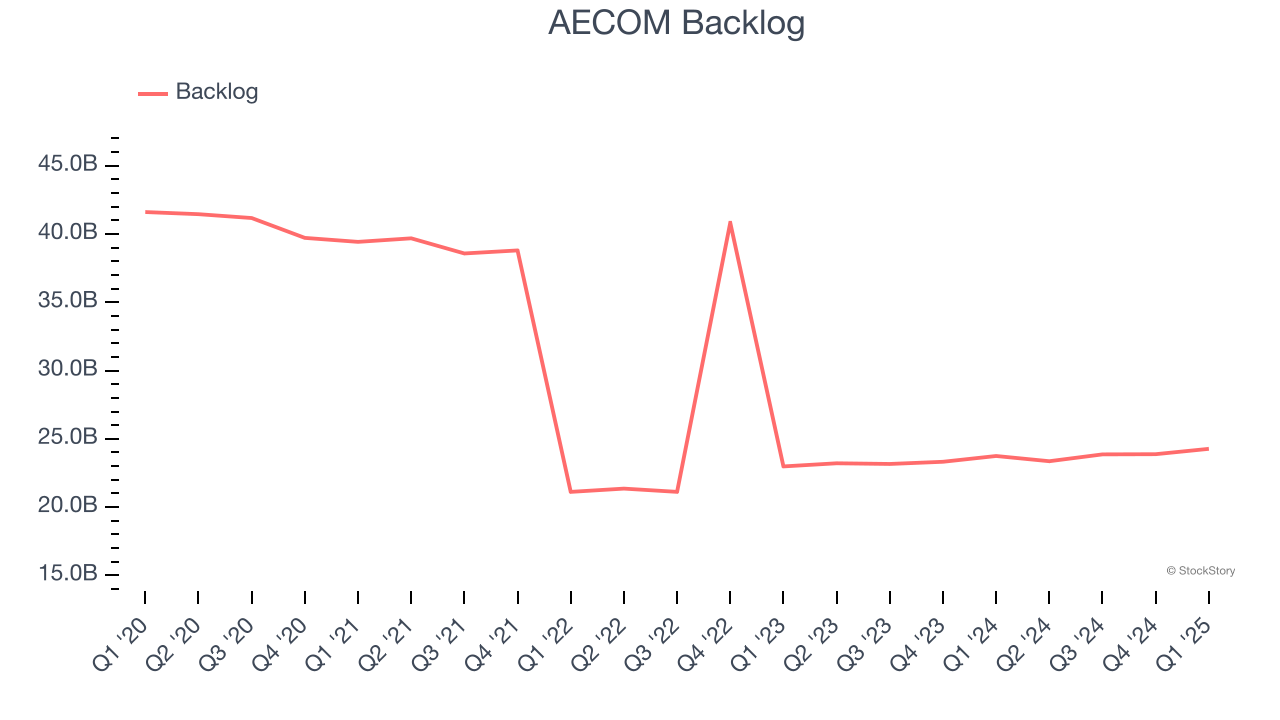

Investors interested in Engineering and Design Services companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into AECOM’s future revenue streams.

AECOM’s backlog came in at $24.27 billion in the latest quarter, and it averaged 1.6% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

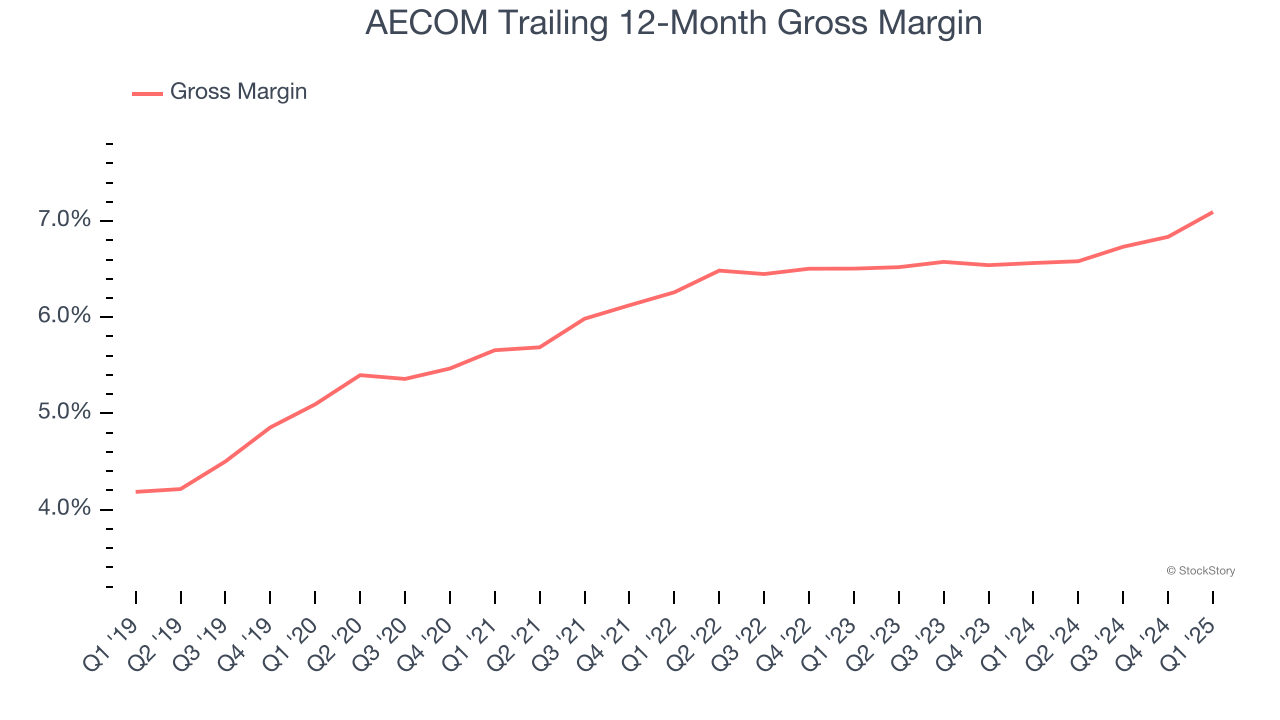

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

AECOM has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 6.4% gross margin over the last five years. Said differently, AECOM had to pay a chunky $93.55 to its suppliers for every $100 in revenue.

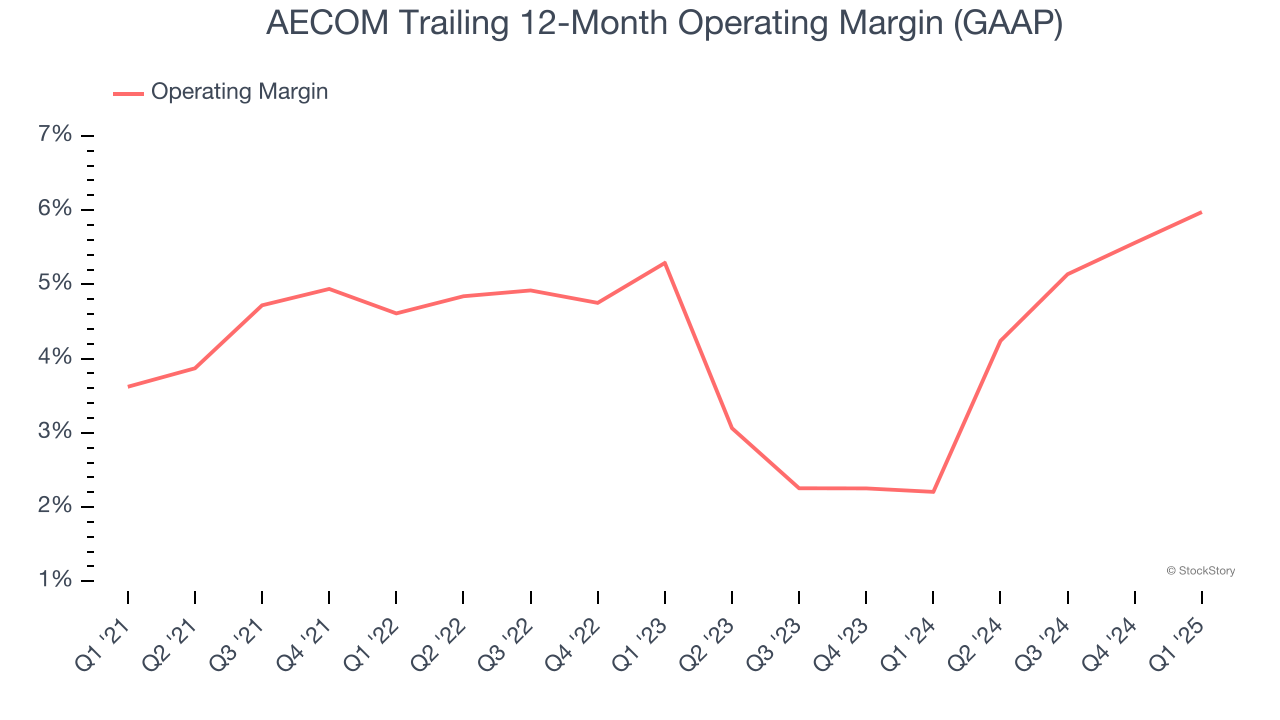

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

AECOM was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.3% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

AECOM isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 21.3× forward P/E (or $109.77 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| 3 hours | |

| Feb-19 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite