|

|

|

|

|||||

|

|

|

Five Below, Inc. FIVE has demonstrated strong upward momentum. FIVE ended Friday’s trading session at $106.52, above its 50 and 200-day simple moving averages (SMAs) of $76.33 and $87.10, respectively, highlighting a continued uptrend. This technical strength, combined with consistent momentum, reflects positive market sentiment and investor confidence in Five Below's financial stability and growth potential.

FIVE Trades Above 50 & 200-Day Moving Averages

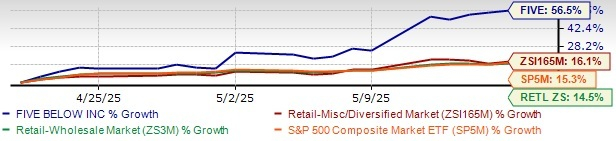

Shares of this specialty value-chain retailer are currently trading 24.8% below its 52-week high of $141.7 reached on June 3, 2024, making investors contemplate their next move. In the past month, FIVE stock has gained 56.5%, significantly outperforming the Zacks Retail-Miscellaneous industry’s 16.1% growth.

The company’s enhanced operational efficiency and growth initiatives have also helped it to outperform the broader Retail-Wholesale sector and the S&P 500 index’s growth of 14.5% and 15.3%, respectively, during the same period.

FIVE Stock Past-Month Performance

Five Below’s strong financial momentum, aggressive expansion and operational improvements position it well for sustained growth. The company’s scalable business model, combined with a disciplined approach to expansion and a sharp focus on customer experience, provides a solid foundation as it enters fiscal 2025 with optimism and strategic clarity.

Five Below delivered a strong financial performance in the fourth quarter of fiscal 2024 despite a tough retail climate. Total sales reached $1.39 billion, up 4% from the same period in 2023, driven by the addition of 22 net stores and the success of new and non-comparable locations. The company’s focus on a customer-centric strategy targeting kids and families, supported by enhanced marketing and trend-right product offerings, helped boost brand engagement and laid the groundwork for continued momentum into fiscal 2025.

FIVE’s aggressive store expansion strategy further underscores its growth potential. In fiscal 2024, the company opened a record 228 stores across 39 states, including its first in Wyoming, increasing the total store count by 14.7% to 1,771. For fiscal 2025, plans include 150 new store openings. The expansion is strategically focused on densifying current markets and entering new ones like the Pacific Northwest.

Five Below has raised its outlook for the first quarter of fiscal 2025, which ended on May 3, 2025, reflecting stronger-than-expected sales and earnings performance. The company now projects net sales of approximately $967 million, well above its previous guided range of $905-$925 million and a sharp increase from $811.9 million in first-quarter fiscal 2024.

Store openings for the quarter are expected to total 55, slightly higher than the earlier estimate of 50. Comparable sales are now forecasted to grow 6.7%, a notable improvement from the initial expectation of flat to 2% growth. Earnings per share are forecasted between 69 cents and 71 cents, up from the previously stated 44-55 cents. Adjusted earnings per share for the fiscal first quarter are expected to be 82-84 cents compared with the prior mentioned 50-61 cents. This compares with the 60 cents reported in the prior-year period.

The company is trading at a notable low price-to-sales (P/S) multiple, below the averages of the industry and the sector. With a forward 12-month P/S of 1.31, FIVE is priced lower than the industry and the sector’s average of 1.64 and 1.59, respectively. This undervaluation highlights its potential for investors seeking attractive entry points. The company’s Value Score of A further emphasizes its investment appeal.

FIVE Looks Attractive From a Valuation Standpoint

The positive sentiment surrounding Five Below is reflected in the upward revisions in the Zacks Consensus Estimate for earnings. In the past 30 days, the consensus estimate has moved up 14 cents to $4.58 per share for the current fiscal year and by 13 cents to $4.84 for the next fiscal year, indicating a year-over-year decline of 9.1% and growth of 5.6%, respectively. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

The Zacks Consensus Estimate for the current and next fiscal year’s sales is pegged at $4.34 billion and $4.75 billion, respectively, implying year-over-year growth of 12% and 9.5%.

Five Below continues to face elevated cost pressures, particularly in managing selling, general, and administrative (SG&A) expenses. In the fiscal fourth quarter, SG&A expenses rose 8.5% to $267 million, with the SG&A rate increasing roughly 80 basis points to 19.2% of net sales.

This increase was mainly caused by fixed cost deleverage due to negative comparable sales, higher store wages and increased investment in store hours. These trends highlight ongoing challenges in controlling operational expenses amid a competitive and demand-sensitive retail environment.

In addition to rising SG&A costs, Five Below is contending with margin pressures. The company’s adjusted gross margin declined 70 basis points year over year to 40.5% in the fiscal fourth quarter, mainly due to fixed cost deleverage and the timing of product costs.

Five Below offers strong long-term potential with robust sales growth, aggressive store expansion and an improved earnings outlook. The company’s focus on value-driven products for families helps maintain strong customer loyalty and the attractive valuation makes it appealing for investors. However, rising operating costs and margin pressures could affect short-term profits. Despite these challenges, the overall outlook remains positive for those holding the stock.

The company currently has a Zacks Rank #3 (Hold).

Some better-ranked stocks are Nordstrom Inc. JWN, Stitch Fix SFIX and Canada Goose GOOS.

Nordstrom is a leading fashion specialty retailer. It has a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Nordstrom’s fiscal 2025 earnings and revenues indicates growth of 1.8% and 2.2%, respectively, from fiscal 2024 reported levels. JWN delivered a negative trailing four-quarter average earnings surprise of 26.1%.

Stitch Fix delivers customized shipments of apparel, shoes and accessories for women, men and kids. It currently has a Zacks Rank of 2.

The Zacks Consensus Estimate for SFIX’s fiscal 2025 earnings implies growth of 64.7% from the year-ago actual. SFIX delivered a trailing four-quarter average earnings surprise of 48.9%.

Canada Goose is a global outerwear brand. GOOS is a designer, manufacturer, distributor and retailer of premium outerwear for men, women and children. It carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for Canada Goose’s current fiscal-year earnings and revenues implies a decline of 1.4% and 4.9%, respectively, from the year-ago actuals. Canada Goose delivered a trailing four-quarter average earnings surprise of 71.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite