|

|

|

|

|||||

|

|

|

Tecnoglass currently trades at $84.90 and has been a dream stock for shareholders. It’s returned 2,188% since May 2020, blowing past the S&P 500’s 97.3% gain. The company has also beaten the index over the past six months as its stock price is up 7% thanks to its solid quarterly results.

Is now still a good time to buy TGLS? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

The first-ever Colombian company to trade on the NASDAQ, Tecnoglass (NYSE:TGLS) is a manufacturer of architectural glass, windows, and aluminum products.

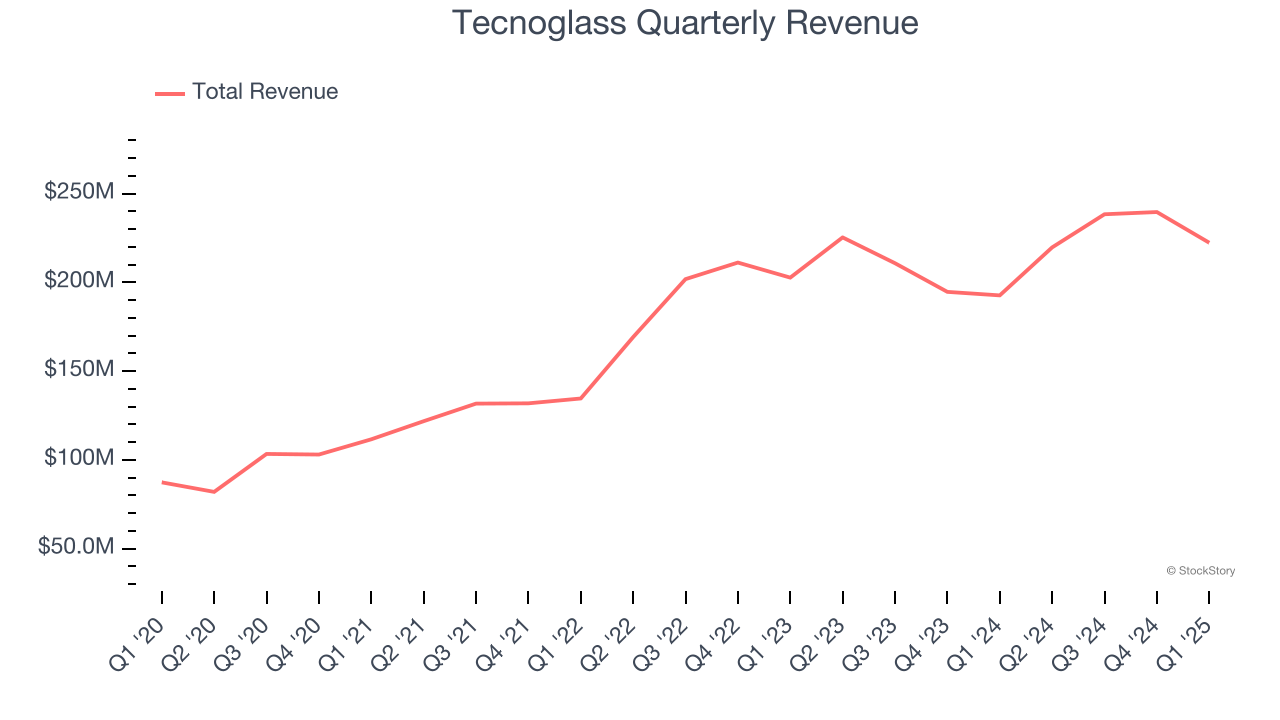

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Tecnoglass’s 17.5% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

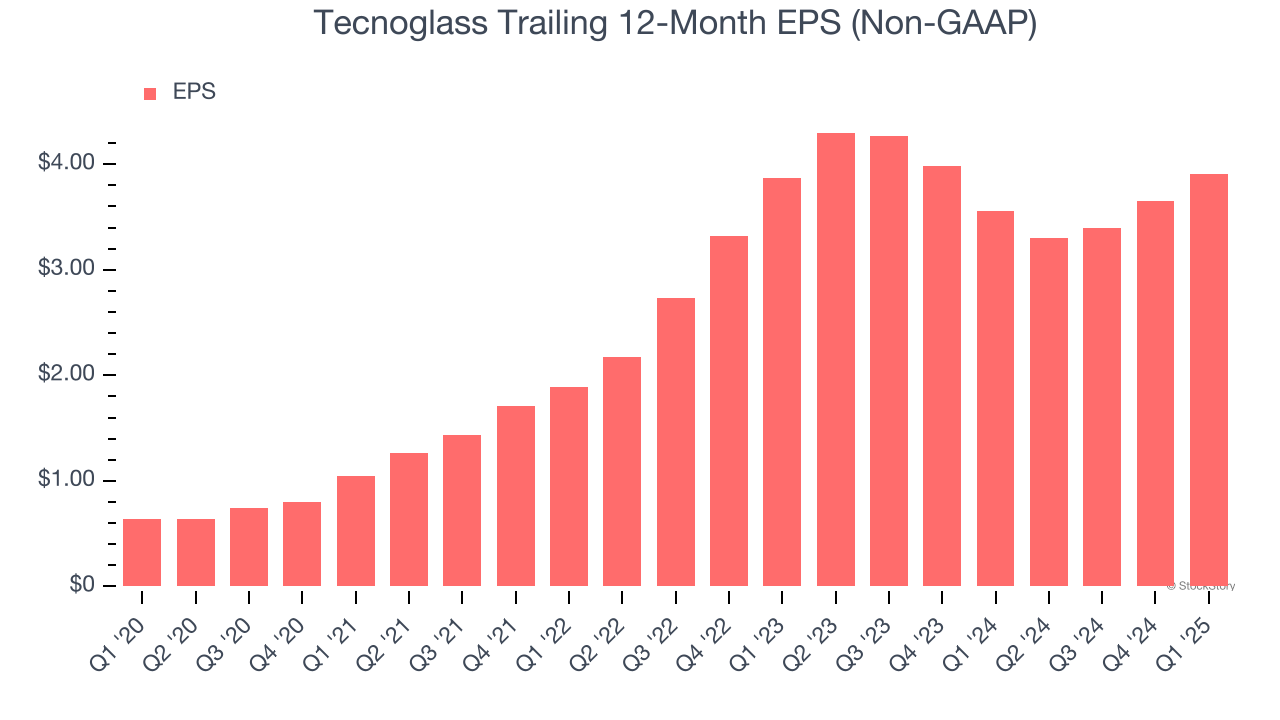

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Tecnoglass’s EPS grew at an astounding 43.6% compounded annual growth rate over the last five years, higher than its 17.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

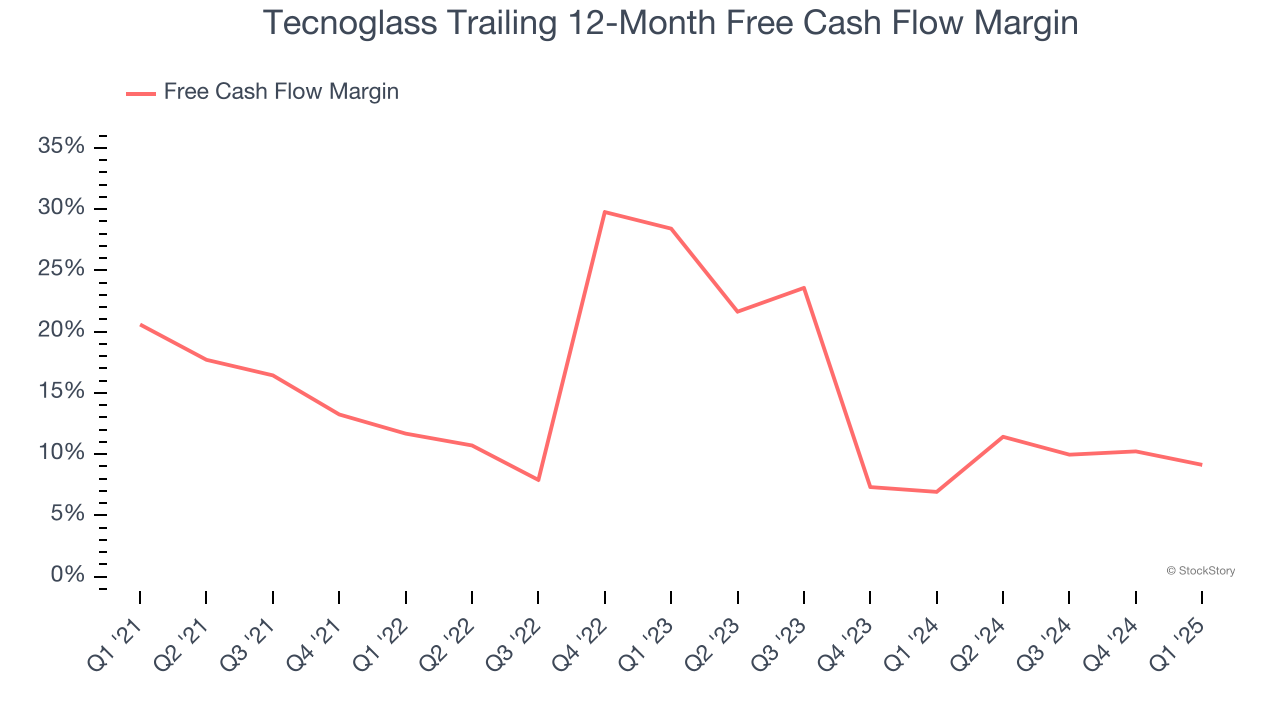

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Tecnoglass’s margin dropped by 11.5 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity. Tecnoglass’s free cash flow margin for the trailing 12 months was 9.1%.

Tecnoglass has huge potential even though it has some open questions, and with its shares beating the market recently, the stock trades at 20.4× forward P/E (or $84.90 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-21 | |

| Jun-10 | |

| May-19 | |

| May-07 | |

| Apr-21 | |

| Apr-09 | |

| Mar-18 | |

| Mar-02 | |

| Mar-02 | |

| Feb-28 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite