|

|

|

|

|||||

|

|

|

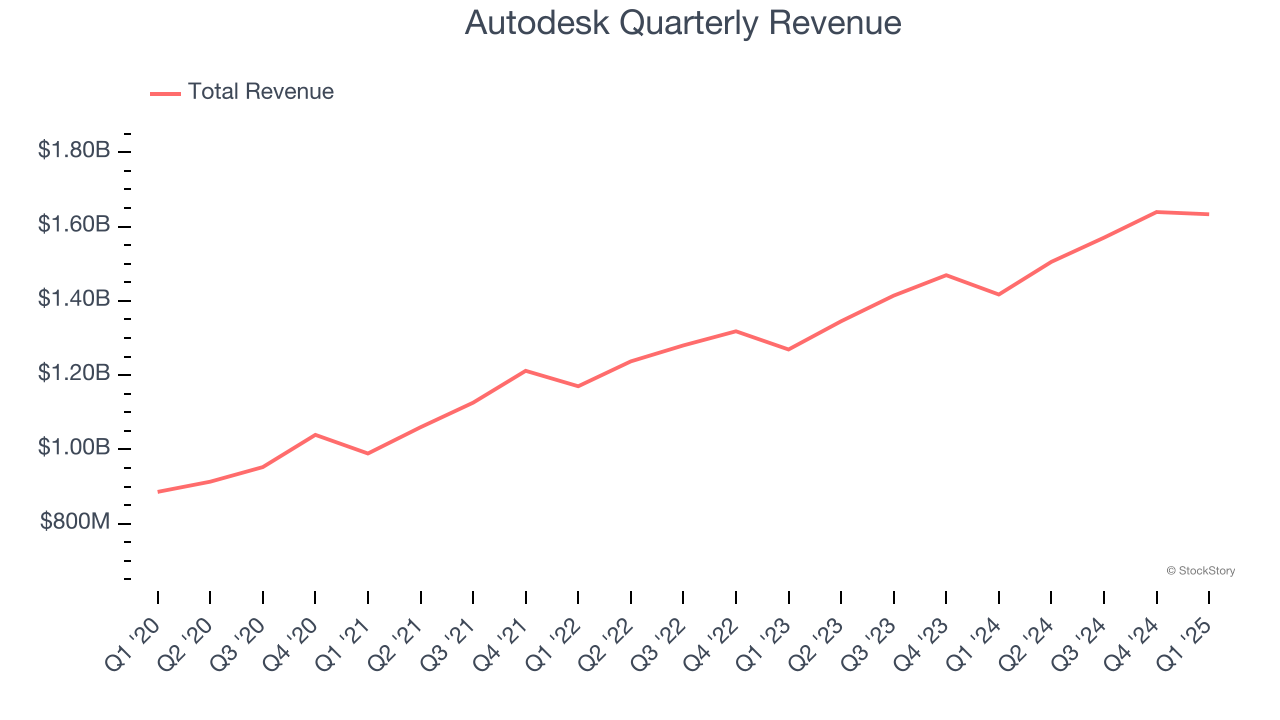

Design software company Autodesk (NASDAQ:ADSK) announced better-than-expected revenue in Q1 CY2025, with sales up 15.2% year on year to $1.63 billion. Guidance for next quarter’s revenue was better than expected at $1.73 billion at the midpoint, 1.6% above analysts’ estimates. Its non-GAAP profit of $2.29 per share was 6.7% above analysts’ consensus estimates.

Is now the time to buy Autodesk? Find out by accessing our full research report, it’s free.

"Against an uncertain geopolitical, macroeconomic, and policy backdrop, our strong performance in the first quarter of fiscal 26 set us up well for the year," said Andrew Anagnost, Autodesk president and CEO.

Founded in 1982 by John Walker and growing into one of the industry's behemoths, Autodesk (NASDAQ:ADSK) makes computer-aided design (CAD) software for engineering, construction, and architecture companies.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Autodesk grew its sales at a 11.6% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds. Luckily, there are other things to like about Autodesk.

This quarter, Autodesk reported year-on-year revenue growth of 15.2%, and its $1.63 billion of revenue exceeded Wall Street’s estimates by 1.7%. Company management is currently guiding for a 14.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12% over the next 12 months, similar to its three-year rate. This projection is above average for the sector and indicates its newer products and services will help maintain its historical top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

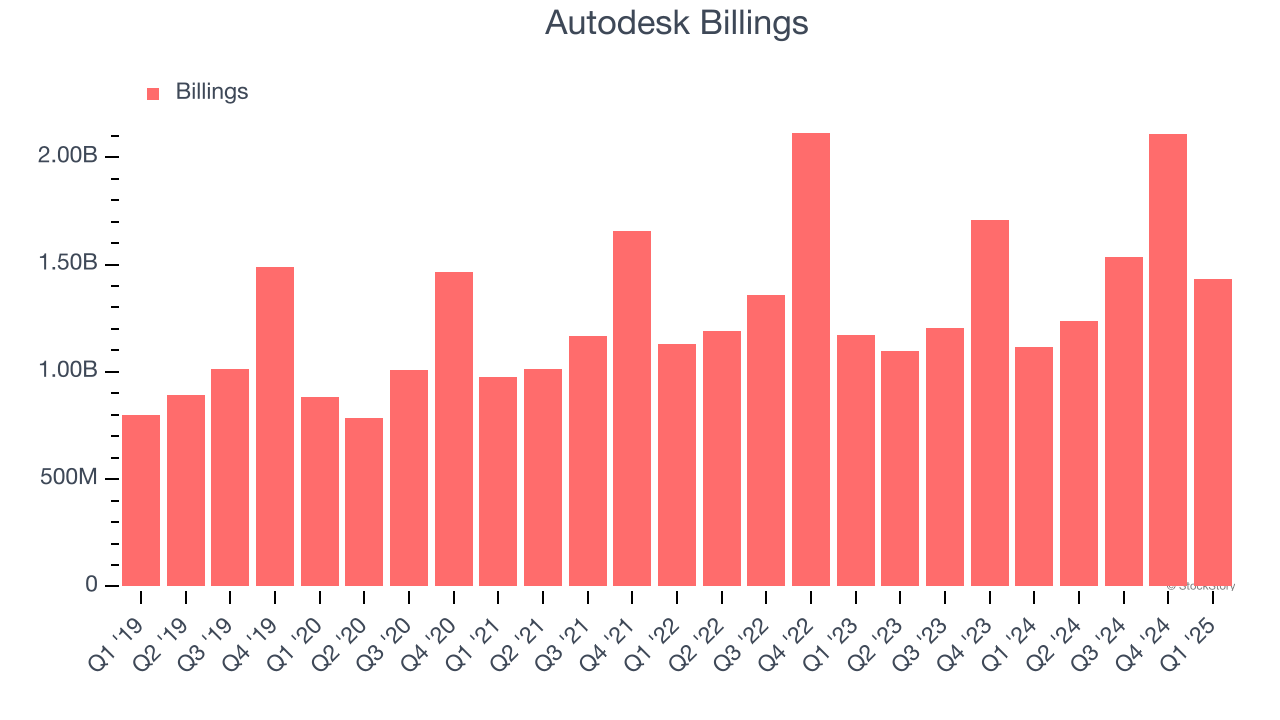

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Autodesk’s billings punched in at $1.43 billion in Q1, and over the last four quarters, its growth was impressive as it averaged 23.1% year-on-year increases. This alternate topline metric grew faster than total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Autodesk’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

It was great to see Autodesk raise its full-year revenue and EPS guidance. We were also glad its billings, revenue, and EPS outperformed Wall Street’s estimates. On the other hand, its EBITDA missed. Still, this print had some key positives. The stock traded up 4.1% to $307.02 immediately after reporting.

Sure, Autodesk had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| 2 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 11 hours | |

| 12 hours | |

| 13 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite