|

|

|

|

|||||

|

|

|

Online vehicle auction company Copart (NASDAQ:CPRT) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 7.5% year on year to $1.21 billion. Its GAAP profit of $0.42 per share was in line with analysts’ consensus estimates.

Is now the time to buy Copart? Find out by accessing our full research report, it’s free.

Starting as a single salvage yard in California in 1982, Copart (NASDAQ:CPRT) operates an online auction platform that connects sellers of damaged and salvage vehicles with buyers ranging from dismantlers and rebuilders to used car dealers and exporters.

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $4.59 billion in revenue over the past 12 months, Copart is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

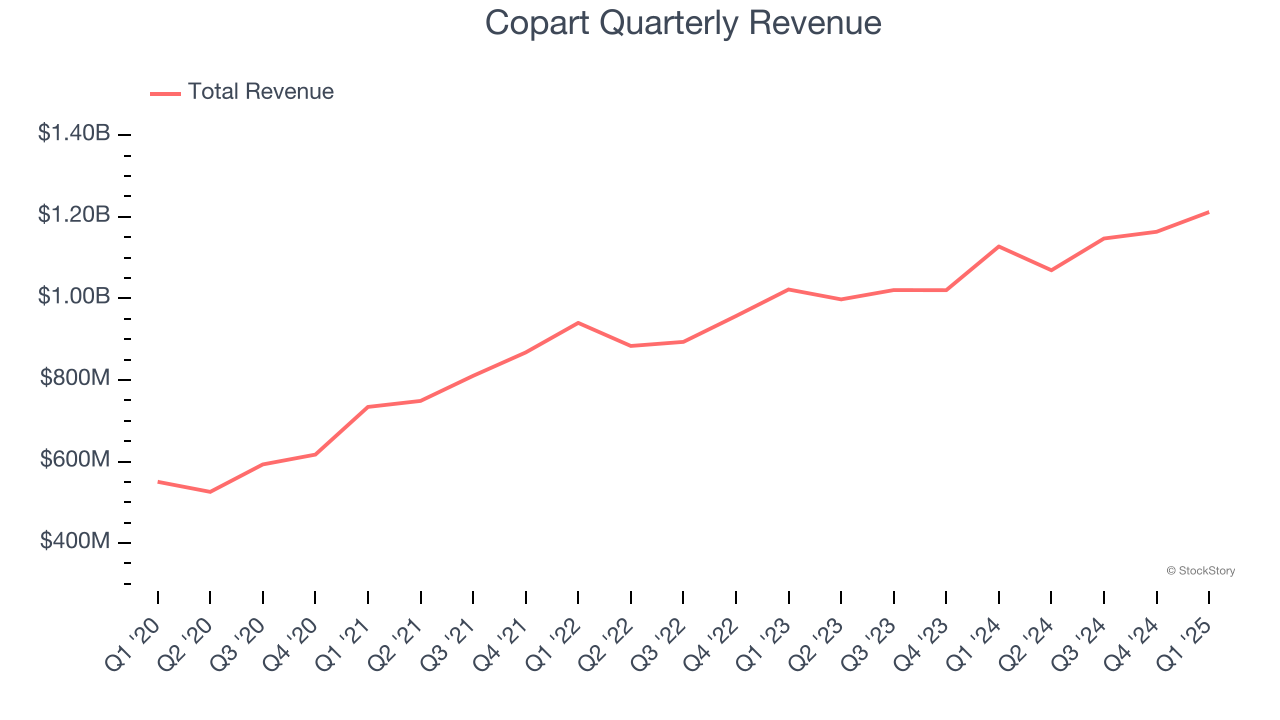

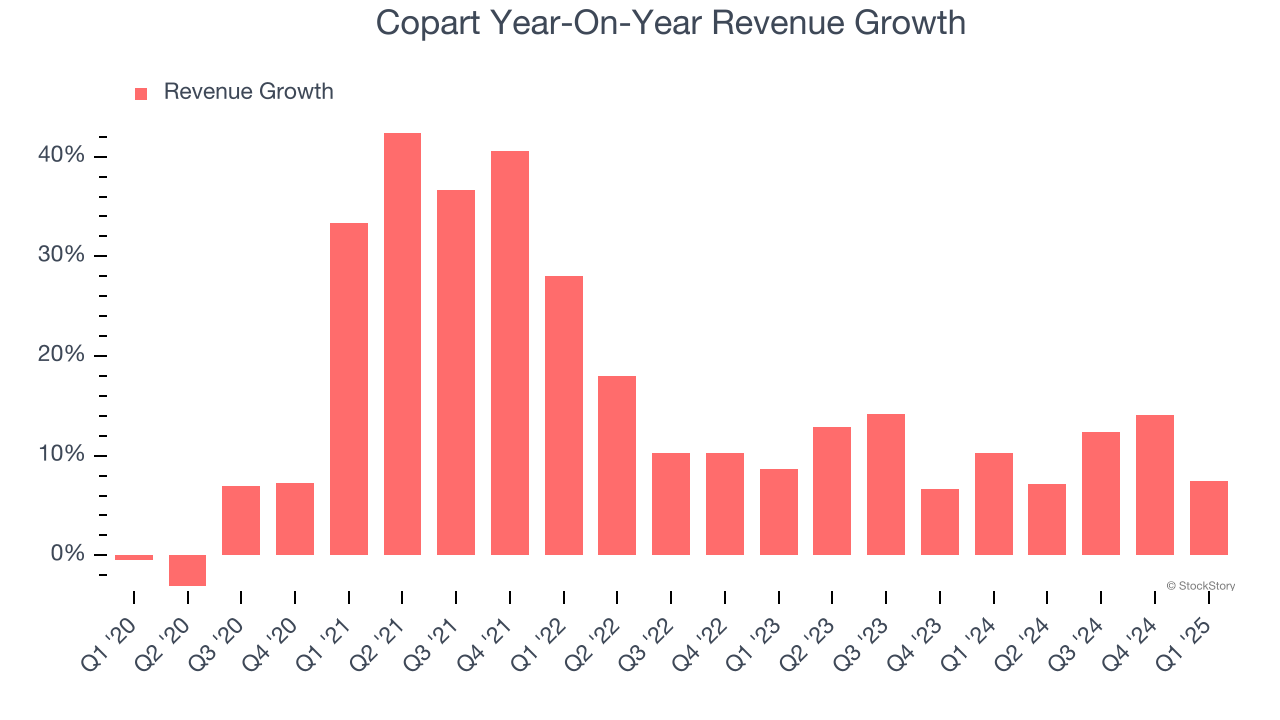

As you can see below, Copart’s 15.6% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Copart’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Copart’s annualized revenue growth of 10.6% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Service. Over the last two years, Copart’s Service revenue (processing and selling cars) averaged 12.9% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Copart’s revenue grew by 7.5% year on year to $1.21 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.4% over the next 12 months, similar to its two-year rate. This projection is admirable and indicates the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

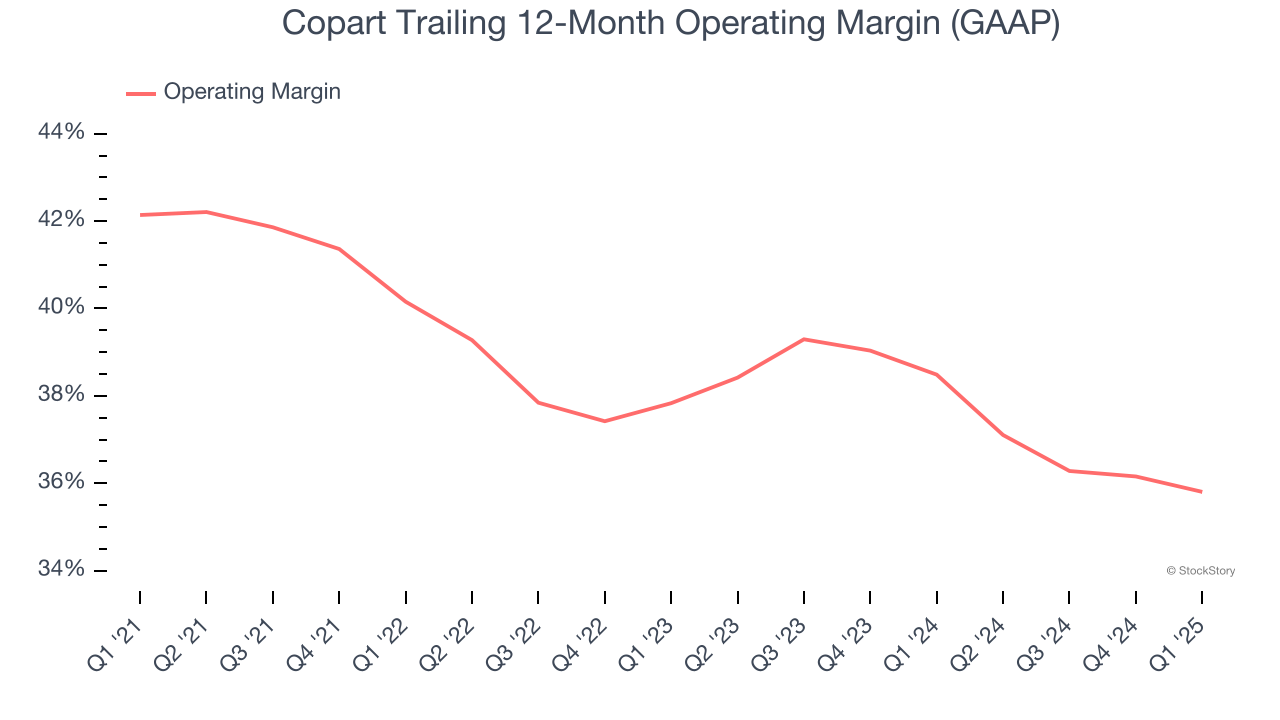

Copart has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 38.5%.

Analyzing the trend in its profitability, Copart’s operating margin decreased by 6.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Copart generated an operating profit margin of 37.3%, down 1.5 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

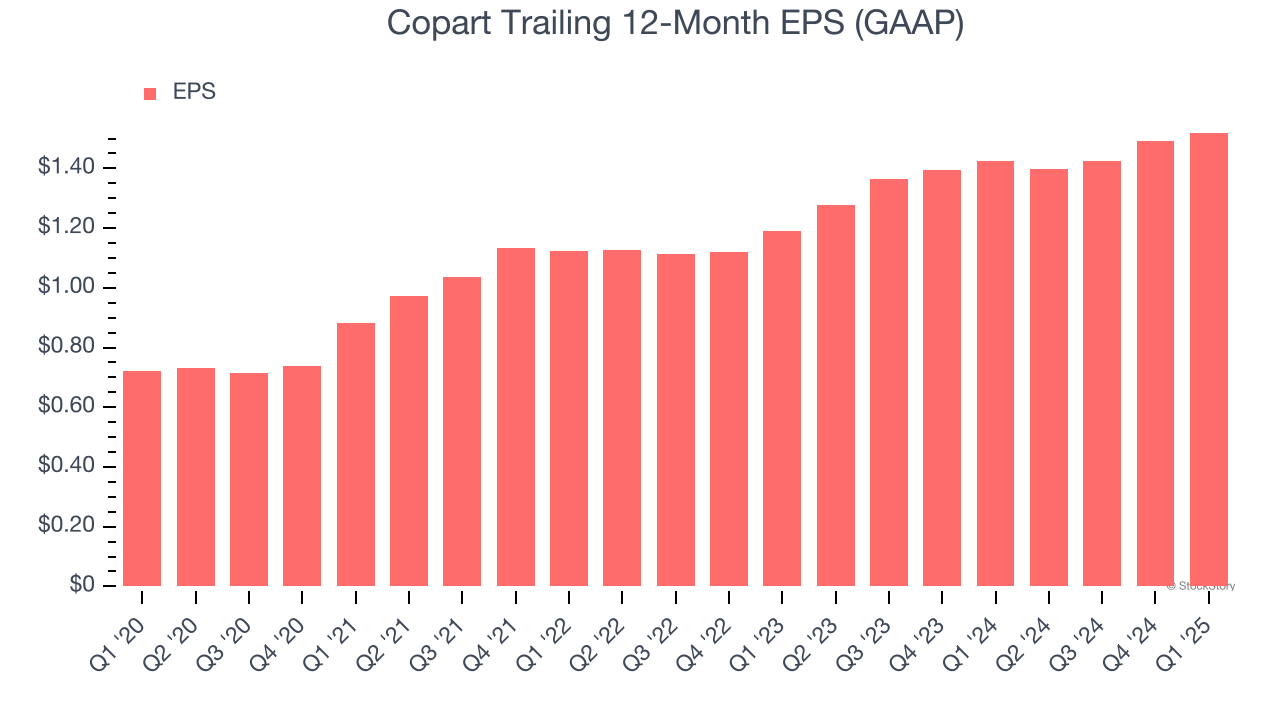

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Copart’s astounding 16.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Copart reported EPS at $0.42, up from $0.39 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Copart’s full-year EPS of $1.52 to grow 12.9%.

We struggled to find many positives in these results. Overall, this was a weaker quarter. The stock traded down 3.8% to $58.33 immediately following the results.

Copart didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Oct-29 | |

| Oct-27 | |

| Oct-27 | |

| Oct-23 | |

| Oct-22 | |

| Oct-21 | |

| Oct-17 | |

| Oct-16 | |

| Oct-15 | |

| Oct-12 | |

| Oct-09 | |

| Oct-03 | |

| Oct-02 | |

| Oct-01 | |

| Oct-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite