|

|

|

|

|||||

|

|

|

CarMax has gotten torched over the last six months - since November 2024, its stock price has dropped 25.5% to $63.46 per share. This might have investors contemplating their next move.

Is there a buying opportunity in CarMax, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why KMX doesn't excite us and a stock we'd rather own.

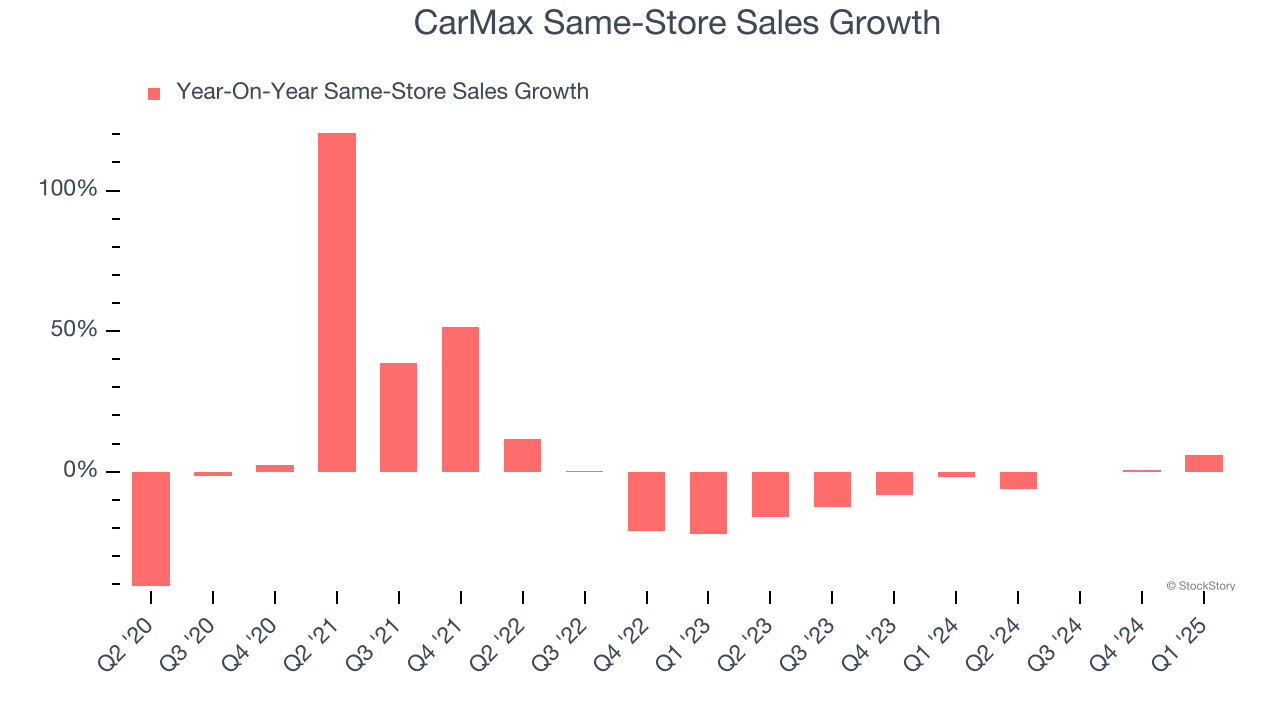

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

CarMax’s demand has been shrinking over the last two years as its same-store sales have averaged 4.9% annual declines.

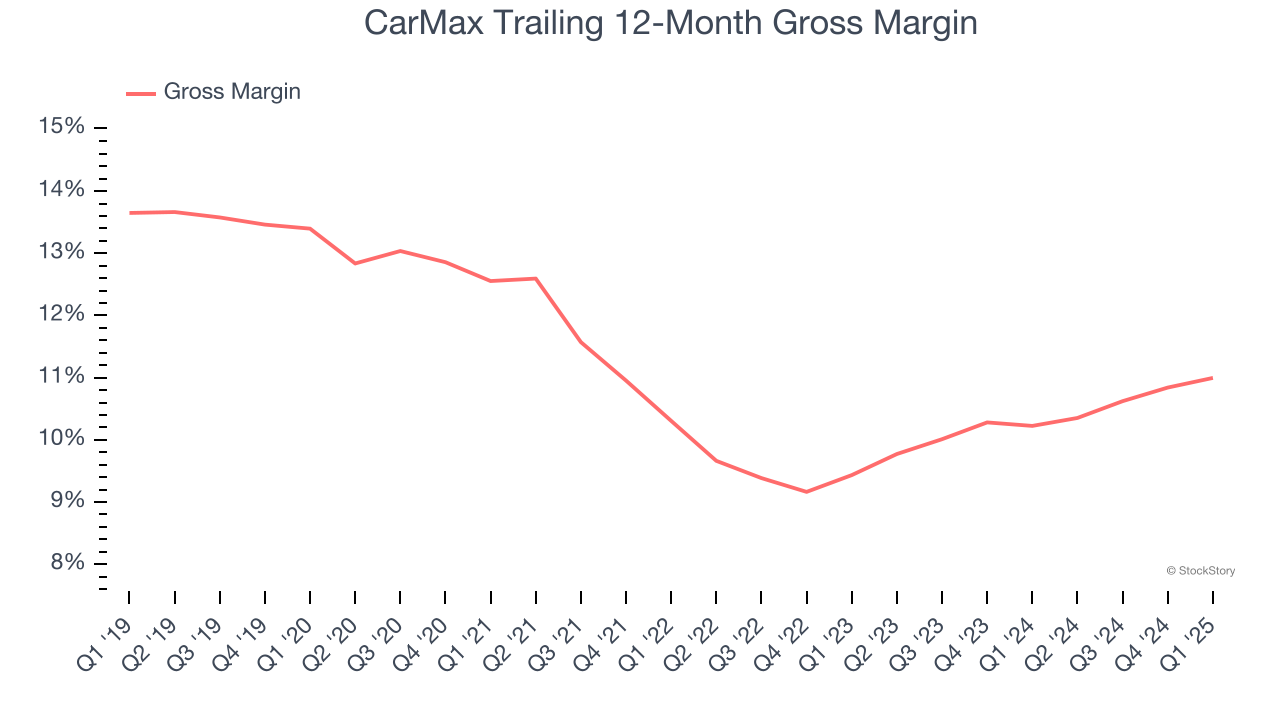

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

CarMax has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 10.6% gross margin over the last two years. Said differently, CarMax had to pay a chunky $89.39 to its suppliers for every $100 in revenue.

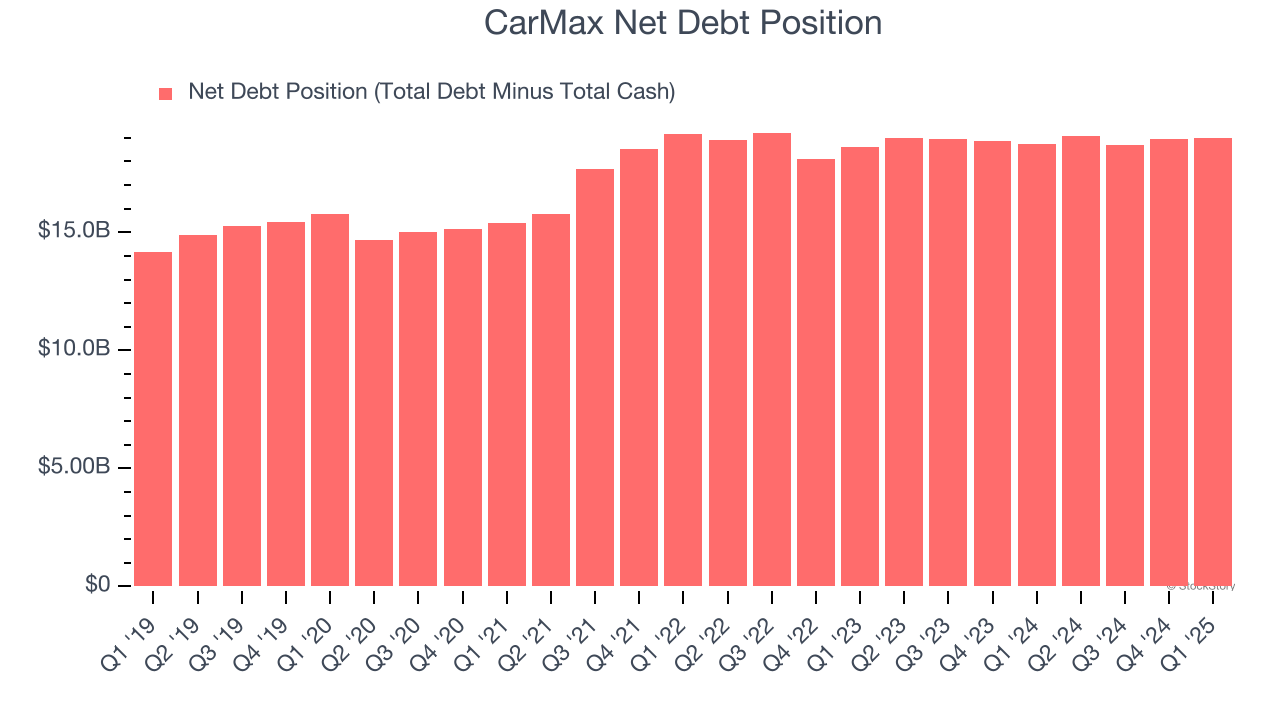

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

CarMax’s $19.22 billion of debt exceeds the $247 million of cash on its balance sheet. Furthermore, its 17× net-debt-to-EBITDA ratio (based on its EBITDA of $1.14 billion over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. CarMax could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope CarMax can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

CarMax isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 15.5× forward P/E (or $63.46 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward one of our top software and edge computing picks.

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Feb-18 | |

| Feb-14 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-08 | |

| Feb-04 | |

| Feb-04 | |

| Feb-03 | |

| Jan-30 | |

| Jan-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite