|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Polaris has gotten torched over the last six months - since November 2024, its stock price has dropped 43.2% to $38.32 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Polaris, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons why there are better opportunities than PII and a stock we'd rather own.

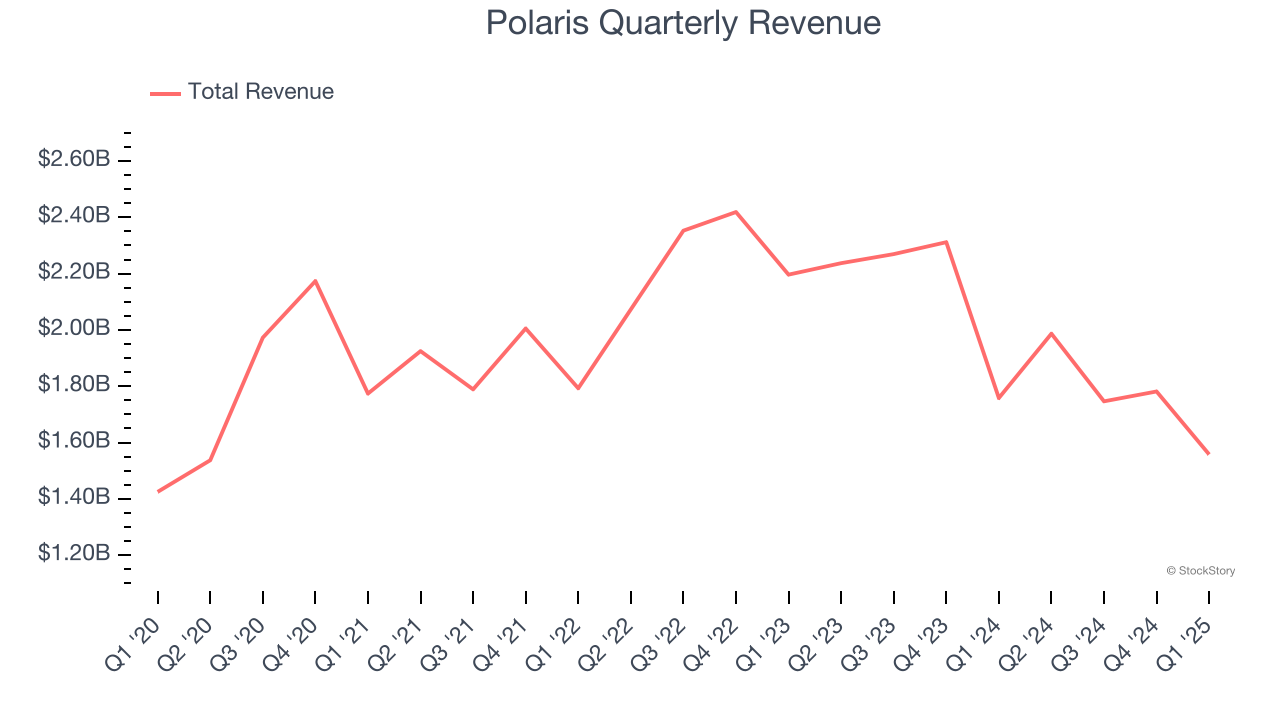

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Polaris struggled to consistently increase demand as its $7.07 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and signals it’s a low quality business.

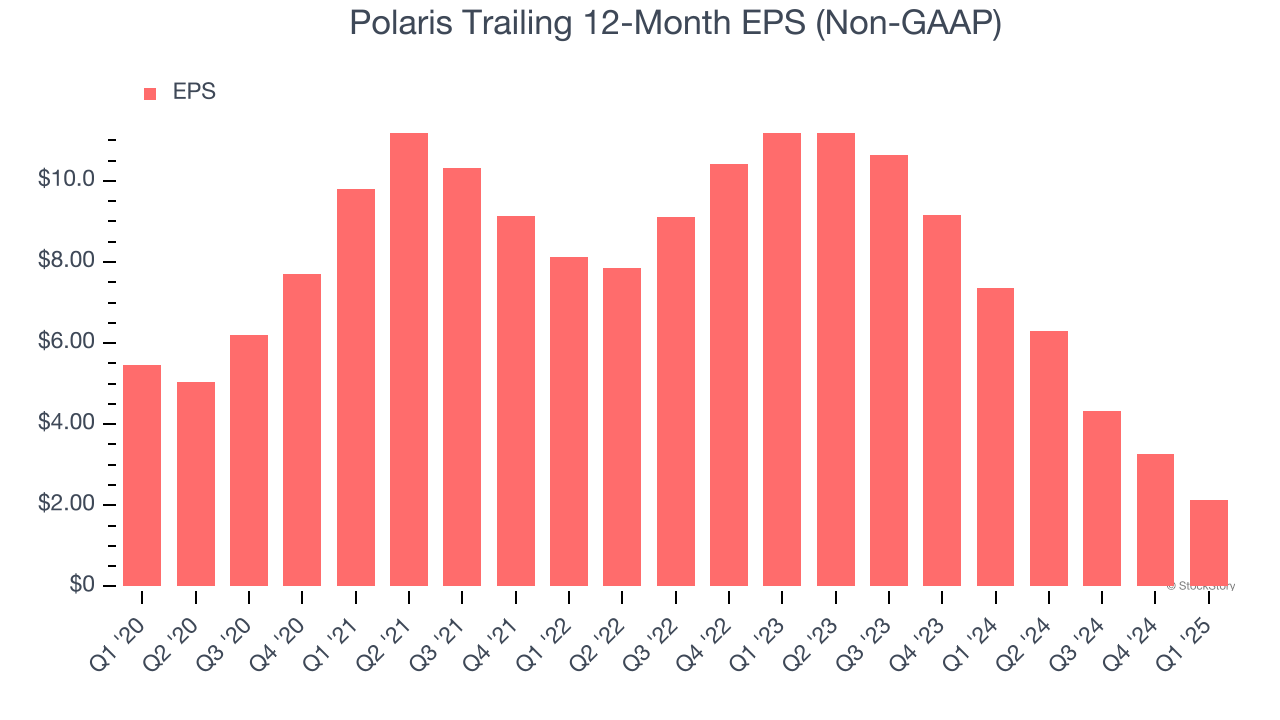

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Polaris, its EPS declined by 17.2% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

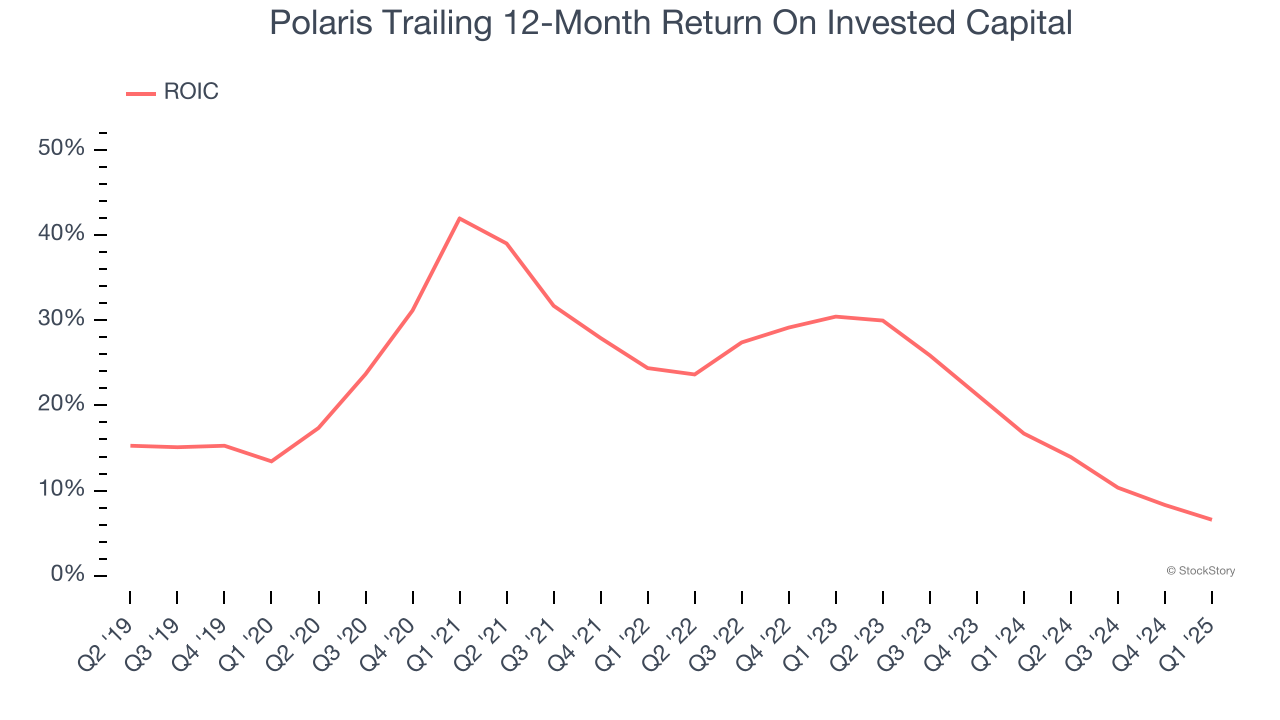

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Polaris’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

We cheer for all companies serving everyday consumers, but in the case of Polaris, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 25.3× forward P/E (or $38.32 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Feb-18 | |

| Feb-11 | |

| Feb-05 | |

| Feb-04 | |

| Feb-03 | |

| Feb-03 | |

| Feb-02 | |

| Jan-30 | |

| Jan-30 | |

| Jan-29 | |

| Jan-29 | |

| Jan-29 | |

| Jan-28 | |

| Jan-27 | |

| Jan-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite