|

|

|

|

|||||

|

|

|

Abercrombie & Fitch Co. ANF is scheduled to report first-quarter fiscal 2025 results on May 28, before the opening bell. The Zacks Consensus Estimate for ANF’s fiscal first-quarter revenues is pegged at $1.06 billion, suggesting 3.7% growth from that reported in the year-ago quarter.

For fiscal first-quarter earnings, the consensus mark is pegged at $1.36 per share, implying a 36.5% decline from the $2.14 reported in the year-ago quarter. The consensus estimate for earnings has moved down 4.2% in the past seven days. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

In the last reported quarter, Abercrombie's earnings beat the consensus estimate by 2.6%. Moreover, ANF has delivered an earnings surprise of 14%, on average, in the trailing four quarters.

Our proven model does not conclusively predict an earnings beat for Abercrombie this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Abercrombie currently has an Earnings ESP of -6.28% and a Zacks Rank of 4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Although Abercombie has been witnessing top-line growth, the sales momentum has been showing a decelerating trend. The sales slowdown from the prior periods mainly reflects that the company is transitioning out of its high-growth phase in fiscal 2023. Abercrombie’s first-quarter and fiscal 2025 guidance also pointed toward continued moderation in sales in the quarters ahead. For the first quarter of fiscal 2025, the company projects sales growth of 4-6%, significantly trailing the 22% jump posted in the same period last year.

The company’s performance in the to-be-reported quarter is expected to reflect pressures from elevated operating costs and higher freight costs, which are expected to weigh on margins. The company’s outlook for the first half of fiscal 2025 suggests continued margin pressure from high freight expenses and more normalized inventory sell-through. However, margins are projected to improve in the second half of fiscal 2025, driven by easing freight costs compared with the prior-year period.

For the first quarter of fiscal 2025, the operating margin is expected to be 8-9%, suggesting a sharp decline from the 12.7% registered a year ago. The earnings per share (EPS) guidance also reflects a challenging near-term outlook. The company expects first-quarter fiscal 2025 EPS of $1.25-$1.45, indicating a significant decline from the $2.14 reported in the same quarter last year.

Our model estimates a year-over-year increase of 9% in adjusted operating expenses for the fiscal first quarter, with a 26.4% decline in adjusted operating income. The adjusted operating margin is estimated to be 8.9%, a 380-bps decline from the year-ago quarter.

American Eagle Outfitters, Inc. price-eps-surprise | American Eagle Outfitters, Inc. Quote

Apart from these, the company is highly skeptical about the impacts of the incremental tariffs, which are expected to hurt its quarterly performance. As for the current tariffs, the company’s outlook includes the effects of the recently imposed U.S. tariffs on China, Canada and Mexico. It expects effects of $5 million from these tariffs in fiscal 2025. The outlook, however, excludes the impacts of other incremental tariffs that may be imposed as retaliatory tariffs.

Despite slowing sales growth rates, the company has been benefiting from solid brand performances, driven by its focus on high-quality, trend-forward assortments that appeal to both new and loyal customers. Management’s commitment to product innovation and quality has been a key factor in sustaining its success.

While our model predicts first-quarter fiscal 2025 total revenues to increase 5.3% year over year, we expect sales for the Hollister and Abercrombie brands to grow 9.9% and 1.7%, respectively.

Abercrombie has increased store traffic by leveraging favorable fashion trends and store optimization. Its store modernization efforts have created inviting spaces that enhance the shopping experience, while e-commerce enhancements, such as personalized recommendations and seamless navigation, support a frictionless omnichannel journey. Gains from these actions are expected to get reflected in its first-quarter fiscal 2025 results.

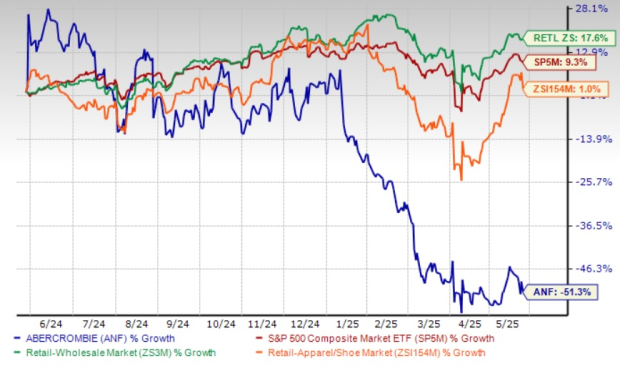

Abercrombie’s shares have exhibited a decline in the past year, underperforming its industry peers and the Zacks Retail-Wholesale sector. In the past year, the New Albany, OH-based company’s shares have declined 51.3% against the industry and the sector’s growth of 1% and 17.6%, respectively. The company has also lagged the S&P 500’s rally of 9.3%.

Although Abercrombie’s stock has declined, it has outperformed arch-rival American Eagle AEO, which has been struggling with a 53.8% decline in the same period. However, ANF has underperformed other competitors like Urban Outfitters URBN and The Gap Inc. GAP, which have rallied 73.2% and 35.7%, respectively, in the past year.

At the current price of $73.17, ANF trades 62.9% below its 52-week high of $196.99. It trades 11.9% above its 52-week low mark of $65.40.

From the valuation standpoint, ANF trades at a forward 12-month P/E multiple of 6.79X, lower than the industry average of 17.68X and the S&P 500’s average of 21.36X. Abercrombie’s valuation appears attractive at this level.

Abercrombie has demonstrated impressive momentum in recent years, underpinned by its strategic rebranding and focus on premium casual wear for men, women and children. The company's renewed emphasis on denim and targeted appeal to millennial consumers has reinvigorated the Abercrombie brand, driving notable improvements in brand perception and sales growth. ANF has also enhanced its competitive position by leveraging digital transformation and optimizing its store footprint. These initiatives have enabled the company to better align with evolving consumer preferences, fueling top-line growth and improved profitability.

However, despite these operational successes, the company faces mounting cost pressures. Elevated operating expenses and rising freight costs are expected to weigh on margins in the near term. In addition, ANF has been vulnerable to macroeconomic uncertainties and potential disruptions from tariff-related policies, which can further impact its cost structure and sourcing strategies.

While Abercrombie continues to benefit from strong brand equity, product innovation, and an improved omnichannel experience, its near-term outlook remains clouded by a deceleration in sales momentum and rising cost pressures. The company is clearly transitioning out of its high-growth phase, and fiscal 2025 is shaping up to be a period of moderation rather than acceleration.

With elevated freight and operating costs weighing on margins and earnings, along with tariff-related risks adding further uncertainty, investor sentiment may remain cautious heading into the upcoming earnings release. Long-term brand resilience and strategic execution offer some support, but the near-term picture suggests a more measured performance ahead.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-15 | |

| Apr-15 | |

| Apr-15 | |

| Apr-15 | |

| Apr-15 | |

| Apr-14 | |

| Apr-14 | |

| Apr-14 | |

| Apr-14 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-08 | |

| Apr-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite