|

|

|

|

|||||

|

|

|

The Nasdaq is in a new bull market. But recently soaring technology stocks are likely due for a cooldown and a pullback following the massive rally off the April lows.

Despite the rally, plenty of strong technology stocks are trading miles below their peaks for various reasons.

Investors might want to buy some of these best-in-class, beaten-down tech stocks before everyone else on Wall Street starts searching for deals again.

Data infrastructure semiconductor solution standout Marvell Technology Group Ltd. MRVL has tanked 50% from its January peaks heading into its Q1 FY26 earnings release on Thursday, May 29.

The chip stock plummeted due to a disappointing revenue forecast for its soon-to-be-reported quarter, analyst downgrades, AI hyperscaler capex spending concerns, tariff-driven fears, and broader semiconductor sector weakness.

Marvell Technology’s selloff was also due since its valuation levels desperately needed a reset after it traded as high as 83X forward earnings last year. MRVL’s downturn, mixed with its still-strong EPS outlook, has it trading at a 30% discount to its 10-year median and 7% below its industry (and nearly in line with Tech) at 27X forward 12-month earnings.

Marvell Technology is a fabless semiconductor giant that designs high-performance, application-specific integrated circuits (ASICs), system-on-chip (SoC) solutions, connectivity and storage chips, and more.

MRVL’s offerings play critical roles across AI data centers, enterprise networking, cloud computing, 5G telecommunications, automotive, and consumer electronics. Its data center end market revenue soared 78% in Q4 as the artificial intelligence spending boom continues.

The tech company is projected to grow its revenue by 44% this year and 18% next year to climb from $5.77 billion in FY25 (2024) to $9.78 billion in FY27 (2026). Meanwhile, it is projected to grow its adjusted earnings by 75% and 27%, respectively.

Marvell Technology’s earnings estimates for this year and next have climbed over the past year and remained largely unchanged after its Q4 FY25 release in early March.

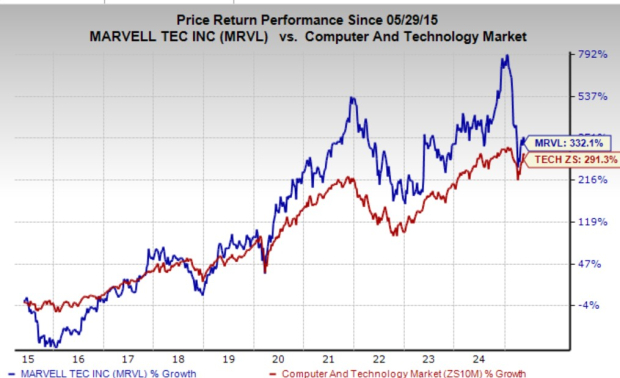

MRVL shares have jumped 330% in the past 10 years to top the Tech sector’s 290%. Yet the chip stock is down 50% from its records even as Tech trades just 5% under its peaks. It is holding ground near its critical 200-week moving average while trading at some of its lowest RSI levels of the past decade.

Wall Street is still bullish on the stock despite its fall, with 25 of the 31 brokerage recommendations Zacks has at “Strong Buys,” and it has a strong balance sheet.

It might be time to buy into weakness on Marvell Technology stock, trading 60% below its average Zacks price target.

Veeva Systems VEEV is a cloud-based software company focused on the pharmaceutical and life sciences industries, boasting clients like Merck, Bayer, and beyond.

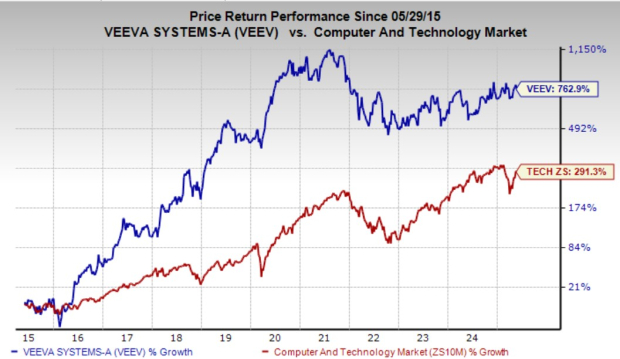

The company averaged roughly 25% revenue growth over the last decade, and its stock has surged 760% to more than double the Tech sector.

Yet, the medical-focused tech company trades 30% below its 2021 peaks heading into its Q1 fiscal 2026 release on Wednesday, May 28. Veeva has chopped around the last several years, as Wall Street worries about its slowing growth and valuation.

VEEV helps clients improve and streamline critical business functions, with software and services for research and development, regulatory processes and compliance, safety, clinical trials, marketing, and beyond. Veeva’s technology enables its clients to bring “products to market faster and more efficiently” while maintaining compliance.

The firm has invested heavily in artificial intelligence, and it announced Veeva AI at the end of April. Its new AI system “provides a fast and efficient way to introduce application-specific AI Agents based on large language models (LLMs) into existing Veeva applications and enable end users with AI Shortcuts.”

Veeva grew its fiscal 2025 (last year) revenue by 16%, driven by a 20% increase in subscription services, helping boost its adjusted earnings by 37%. Its FY26 and FY27 EPS estimates have improved slightly since its last report and it has topped our estimate for five years running.

VEEV is projected to grow its revenue by 11% this year and 12% next, while boosting its adjusted earnings by 11% both years.

The stock has climbed 11% in 2025 to outpace the Tech sector’s 3% drop. Yet, VEEV trades roughly 30% below its 2021 records and 12% below its average Zacks price target. The solid YTD performance helped it climb above its long-term 50- and 200-week moving averages.

Veeva’s valuation has held the stock back, with it trading at 43.5X forward 12-month earnings vs. Tech’s 25.2X. Yet, Veeva’s current levels represent 40% value vs. its 10-year median and 70% value compared to its highs.

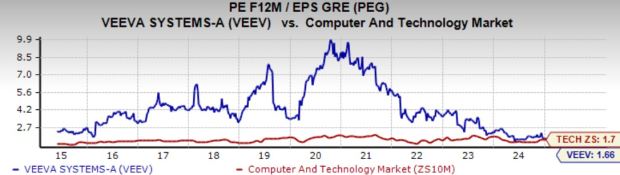

Its strong earnings growth outlook has it trading directly in line with Tech at a 1.7 price/earnings-to-growth ratio, even though Veeva has doubled Tech over the past 10 years. VEEV also trades at an 80% discount to its highs and 55% vs. its median.

Taking a chance on Veeva makes even more sense when investors consider that it has $5.1 billion in cash and equivalents and short term investments next to zero debt and $1.5 billion in total liabilities. This gives the medical software company the ability to pursue more organic growth opportunities and acquisitions.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 3 hours | |

| 4 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite