|

|

|

|

|||||

|

|

|

Pembina Pipeline Corporation PBA, headquartered in Calgary, Alberta, is a major force in North America's energy infrastructure sector. The company manages an extensive system of pipelines, gas processing facilities and storage terminals that support the full spectrum of hydrocarbon logistics. Its operations span key oil and gas producing regions, enabling the movement of substantial volumes of energy products across the continent.

PBA holds listings on both the Toronto and New York stock exchanges, reinforcing its position as a significant entity in the oil and gas midstream space. With its wide-ranging infrastructure capabilities, particularly in transporting and processing hydrocarbons, the company remains a focal point for energy investors.

Given its critical function in the industry, market watchers are closely monitoring PBA stock. But what factors are driving its performance? What risks could hinder its progress? Let us explore the dynamics influencing PBA’s trajectory, highlighting both the potential catalysts for growth and the key vulnerabilities it faces.

Strong Financial Performance and Dividend Growth: Pembina reported a robust first-quarter 2025 with adjusted EBITDA of C$1.2 billion, a 12% increase year over year and earnings of C$502 million, up 15%. The company raised its quarterly dividend by 3% to 71 Canadian cents per share, reflecting confidence in its cash flow stability. This dividend growth underlines Pembina’s commitment to returning capital to shareholders, supported by its highly contracted, fee-based business model. The company is trending toward the midpoint of its 2025 EBITDA guidance range of C$4.2-C$4.5 billion, indicating resilience despite macroeconomic volatility.

Strategic Contracting and Volume Commitments: Pembina secured significant long-term, take-or-pay agreements with a leading Montney producer, covering transportation, fractionation and marketing services. These contracts enhance utilization across its Peace Pipeline, Pouce Coupé systems and Redwater Complex, including the under-construction RFS IV. Such agreements provide revenue visibility and mitigate volume risk, reinforcing Pembina’s low-risk business model. The company’s ability to lock in volumes amid market uncertainty highlights its competitive positioning in the Western Canadian Sedimentary Basin (“WCSB”).

Growth Projects and Capital Efficiency: Pembina is advancing a C$4+ billion portfolio of growth projects, including the Taylor-to-Gordondale expansion, Cedar LNG and RFS IV. These projects are designed to capitalize on rising WCSB volumes and diversify end-market exposure. Management emphasized a track record of delivering projects on time and on budget, with superior capital efficiency compared with peers. The Cedar LNG remarketing process is progressing well, with definitive agreements in negotiation, signaling strong demand for Canada’s LNG exports.

Diversification and Reduced U.S. Tariff Exposure: Pembina is actively diversifying its NGL marketing beyond U.S. markets, leveraging West Coast export capacity to access premium global markets. The company noted that its products are CUSMA-compliant, avoiding current U.S. tariffs. Recent contracts include tariff-sharing provisions, further mitigating risks. This strategy enhances long-term resilience, particularly as global demand for Canadian energy grows.

Strong Balance Sheet and Financial Flexibility: Pembina’s proportionally consolidated debt-to-EBITDA ratio was 3.4x, well below its target range (3.5x-4.0x), supporting a BBB credit rating. The company generated meaningful free cash flow in the first quarter, allocated to debt reduction and shareholder returns. This financial strength positions Pembina to pursue opportunistic acquisitions or share buybacks if market conditions favor offensive moves.

Exposure to Commodity Price Volatility in Marketing Segment: While Pembina’s marketing business outperformed in the first quarter, management cautioned that lower commodity prices due to global economic uncertainty could offset gains later in 2025. The segment’s EBITDA guidance of C$550 million for 2025 remains unchanged, highlighting sensitivity to NGL margins and crude oil prices. This volatility introduces earnings risk, despite hedging (50% of frac spreads).

Regulatory and Toll Uncertainty for Alliance Pipeline: The CER review process for Alliance Pipeline tolls remains unresolved, with Pembina acknowledging potential lower future tolls. While negotiations aim for a balanced outcome, any material reduction in tolls could pressure EBITDA. The U.S. Federal Energy Regulatory Commission review in December 2025 adds another layer of uncertainty.

Delays in Dow’s Path2Zero Project: Dow Chemicals Canada’s decision to delay its ethylene cracker project (key to Pembina’s ethane supply agreement) introduces execution risk. While Pembina has not spent material capital yet, the timeline for its de-ethanizer project (RFS III) may now extend, potentially delaying associated cash flows. The long-term demand for ethane infrastructure could weaken if Dow further postpones its plans.

Macro Risks, Tariffs and Global Demand: Although Pembina is diversifying away from U.S. markets, prolonged trade tensions or new tariffs could disrupt NGL exports. A slowdown in demand for LNG in Asia or propane might also impact Cedar LNG and West Coast export economics. These external factors lie outside Pembina’s control.

Capital Intensity of Growth Projects: Pembina’s C$4+ billion project pipeline requires significant capital expenditures, which could strain free cash flow if execution challenges arise. While the company has a strong track record, cost overruns or delays (e.g., Cedar LNG) could impact returns. Investors may prefer more immediate cash-generating investments.

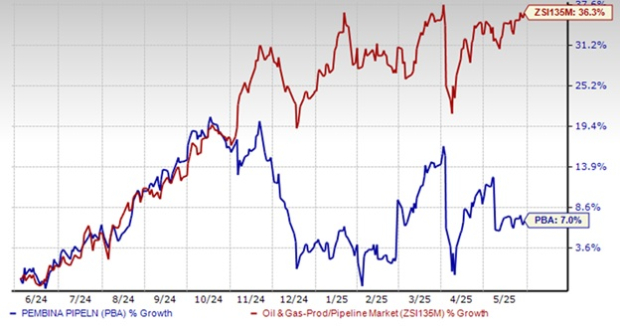

Recent Stock Performance Concerns: PBA's share price has declined 7%, while its Production and Pipelines sub-industry has gained 36.3%. This relative underperformance may reflect investor concerns and could weigh on PBA’s valuation in the near term.

Pembina Pipeline shows strong fundamentals, with first-quarter 2025 earnings up 15%, a 3% dividend increase and progress on major growth projects like Cedar LNG, supported by long-term contracts and a resilient, fee-based model. The company maintains a strong balance sheet and financial flexibility, positioning it well for future opportunities.

However, it also faces risks, including exposure to commodity price volatility in its marketing segment and regulatory uncertainty related to the Alliance Pipeline. Delays in partner projects like Dow’s ethylene cracker and the capital-intensive nature of its growth plans could impact timelines and returns. Given the balance of growth potential and risks, investors should wait for a more favorable opportunity to add this stock to their portfolios.

Currently, PBA has a Zacks Rank #3 (Hold).

Investors interested in the energy sector might look at some better-ranked stocks like Subsea 7 SUBCY, which sports a Zacks Rank #1 (Strong Buy), Paramount Resources Ltd. PRMRF and RPC, Inc. RES, each holding a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Subsea 7 is valued at $5.14 billion. The company is a global leader in delivering offshore projects and services for the energy industry, specializing in subsea engineering, construction and installation. Headquartered in Luxembourg, Subsea 7 supports both the oil & gas and renewable energy sectors with integrated solutions, including subsea infrastructure, heavy lifting and life-of-field services.

Paramount Resources is valued at $1.99 billion. It is a Calgary-based energy company engaged in the exploration and development of conventional and unconventional petroleum and natural gas reserves across Canada. Paramount Resources’ key assets include significant holdings in the Duvernay, Montney, Muskwa and Besa River formations located in Alberta and northeast British Columbia.

RPC is valued at $979.31 million. The company provides a wide range of oilfield services and equipment to support the exploration, production and maintenance of oil and gas wells globally. RPC operates through Technical Services—offering pressure pumping, cementing, and well control—and Support Services, which rents tools and provides pipe handling and inspection.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-16 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jun-23 | |

| Jun-01 | |

| May-26 | |

| May-25 | |

| May-07 | |

| May-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite