|

|

|

|

|||||

|

|

|

Credo Technology Group Holding Ltd CRDO reported fourth-quarter fiscal 2025 adjusted earnings per share (EPS) of 35 cents, which surpassed the Zacks Consensus Estimate by 29.6%. The bottom line compared favorably with 7 cents posted in the prior-year quarter.

The company’s revenues surged 179.7% year over year to $170 million. The increase in sales was primarily driven by strong growth in its product business. The top line also surpassed the Zacks Consensus Estimate by 6.27%.

CRDO achieved record financial performance for fiscal 2025, with revenues rising 126% year over year to $436.8 million. The top-line growth was driven by strong demand for its innovative, and energy-efficient high-performance connectivity solutions. Demand continues to accelerate, particularly among hyperscaler customers supporting advanced AI services. For fiscal 2025, the company reported adjusted EPS of 70 cents compared with 9 cents in fiscal 2024.

In response to the better-than-anticipated results, shares jumped approximately 15% in the pre-market trading session today.

(See the Zacks Earnings Calendar to stay ahead of market-making news.)

Credo Technology Group Holding Ltd. price-consensus-eps-surprise-chart | Credo Technology Group Holding Ltd. Quote

Product Sales: The company’s product business surged 303.3% year over year to $164.5 million during the quarter.

Product engineering services: The company’s product engineering services fell 60% year over year to $1.3 million.

IP license: The company’s IP license sales were down 75% year over year to $4.2 million.

In the fourth quarter, each of the company’s top three customers contributed more than 10% to revenues. Credo Technology expects three to four customers to exceed 10% of revenues in the upcoming quarters and fiscal year, driven by increasing volumes from existing hyperscalers and the expected ramp-up of two new hyperscale customers in the second half of fiscal 2026.

Non-GAAP gross profit came to $114.5 million in the fourth quarter compared with $40.2 million in the same period last year.

Non-GAAP gross margin expanded 130 basis points (bps) to 67.4% during the quarter under review. The figure also exceeded the top end of the company’s guidance and increased 355 bps sequentially.

Total non-GAAP operating expenses increased 58.9% year over year to $52 million.

Research and development expenses surged 76.7% year over year to $47.6 million.

Selling, general and administrative expenses increased 58.4% year over year to $32 million.

As of May 3, 2025, CRDO had $431.3 million of cash and cash equivalents and short-term investments compared with $410 million as of April 27, 2024.

The company generated a fourth-quarter fiscal 2025 cash flow from operating activities of $57.8 million, up $53.6 million sequentially, driven by strong cash collections from the product ramp. Capital expenditure totaled $3.7 million, mainly for production equipment, resulting in a free cash flow of $54.2 million, up $54.6 million from the third quarter.

For the first quarter of fiscal 2026, the company expects revenues between $185 million and $195 million, up 12% at the midpoint. Non-GAAP gross margin is projected at 64–66%, with operating expenses between $54 million and $56 million and a diluted share count of approximately 188 million. These estimates assume the current tariff regime.

For fiscal 2026, Credo Technology anticipates revenues to surpass $800 million, implying more than 85% year-over-year growth. Non-GAAP operating expenses are expected to grow at less than half the revenue growth rate, driving non-GAAP net margin to nearly 40%. Strong AI-driven demand and solid execution supported its fiscal 2025 performance and continue to fuel momentum.

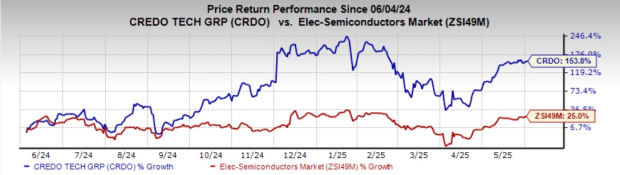

CRDO currently has a Zacks Rank #3 (Hold). Shares of the company have soared 153.8% in the past year compared with the Zacks Electronics-Semiconductors industry's growth of 25%. You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Cadence Design Systems CDNS reported first-quarter 2025 non-GAAP earnings per share (EPS) of $1.57, which beat the Zacks Consensus Estimate by 5.4%. The bottom line increased 34.2% year over year, exceeding management’s guided range of $1.46-$1.52. Revenues of $1.242 billion topped the Zacks Consensus Estimate by 0.3% and increased 23% year over year. CDNS’s top line was driven by broad-based demand for its solutions amid robust design activity.

In the past year, shares of CDNS have inched up 1.9%.

SAP SAP reported first-quarter 2025 non-IFRS EPS of €1.44 ($1.51), which increased 79% from the year-ago quarter. The Zacks Consensus Estimate was pegged at $1.39. Driven by momentum in the cloud business, SAP reported total revenues on a non-IFRS basis of €9.01 billion ($9.48 billion), which increased 12.1% year over year (up 11% at constant currency or cc). The Zacks Consensus estimate was pegged at $9.78 billion.

In the past year, shares of SAP have soared 65.4%.

Simulations Plus, Inc. SLP second-quarter fiscal 2025 adjusted earnings of 31 cents per share, which fell 3% year over year. However, the figure surpassed the Zacks Consensus Estimate of 25 cents per share. Quarterly revenues jumped 23% year over year to $22.4 million, driven by increasing momentum across its software and services business segments. The growing uptake of its flagship solutions, including GastroPlus, MonolixSuite and ADMET Predictor, fueled the top-line expansion.

In the past six months, shares of SLP have decreased 15.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 16 hours | |

| Apr-27 | |

| Apr-27 | |

| Apr-27 | |

| Apr-27 | |

| Apr-27 | |

| Apr-27 | |

| Apr-24 | |

| Apr-24 | |

| Apr-24 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite