|

|

|

|

|||||

|

|

|

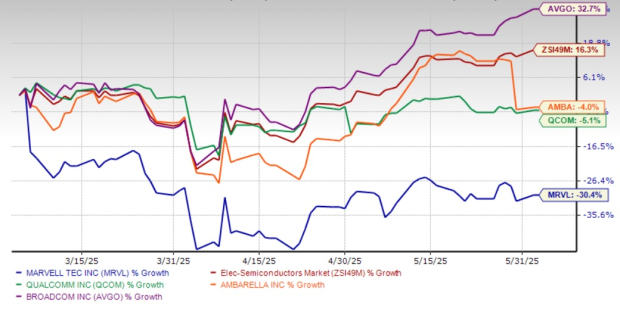

Marvell Technology’s MRVL shares have plunged 30.4% in the past three months, underperforming the Zacks Electronics - Semiconductors industry and its peers, including Broadcom AVGO, Qualcomm QCOM and Ambarella AMBA. While Broadcom shares have returned 32.7%, shares of Qualcomm and Ambarella have lost 5.1% and 4%, respectively, in the same time frame.

This steep decline in the share price of this semiconductor leader raises the question: Should investors hold on or exit the stock to minimize losses?

Fears of rising trade tensions and slowing economic growth have put pressure on the entire technology sector, prompting widespread sell-offs in tech stocks.

The U.S. government’s recent stance toward China has also been a matter of concern for Marvell Technology, as the company generates significant revenues (about 43% of its fiscal 2025 total revenues) from the Chinese market.

Additionally, as Marvell Technology owns research and development facilities in China and outsources there, the growing geopolitical tension, fear of fresh sanctions and persistent tariff threats have added to investors’ skepticism.

Weakness in MRVL’s consumer end market due to volatility in gaming demand and lumpy order patterns in industrial business has added to investor concerns. Furthermore, Marvell Technology’s custom AI silicon, including XPUs, which are driving its revenue growth, is lowering MRVL’s gross margins due to higher costs associated with manufacturing these chips. However, not everything is gloom and doom for MRVL stock.

Marvell Technology is gaining from hyperscalers’ increasing reliance on custom silicon for AI workloads. The data center segment, which is also Marvell Technology’s largest segment, is benefiting from solid momentum in electro-optics products, custom AI silicon and next-generation switch divisions.

As AI workloads gain momentum, data centers are expected to require improved networking and interconnect solutions. Marvell Technology can seize this opportunity and capitalize on this shift with its advanced optical interconnects, including 800G PAM, 400ZR DCI, and its industry-first 1.6T PAM digital signal processor.

Additionally, the transition from copper to optical connectivity in AI infrastructure represents a massive growth opportunity for Marvell Technology’s Co-Packaged Optics technology. Additionally, as Marvell Technology’s enterprise networking and carrier infrastructure segments are now returning to normalcy on the back of demand recovery.

With all these factors at play, the Zacks Consensus Estimate for Marvell Technology’s 2026 revenues is pegged at $8.2 billion, indicating year-over-year growth of 42%. The consensus mark for earnings is pegged at $2.75 per share, suggesting a whopping 75.2% year-over-year increase.

Marvell Technology beat the Zacks Consensus Estimate in each of the trailing four quarters, with an average surprise of 3.6%.

Marvell Technology, Inc. price-consensus-eps-surprise-chart | Marvell Technology, Inc. Quote

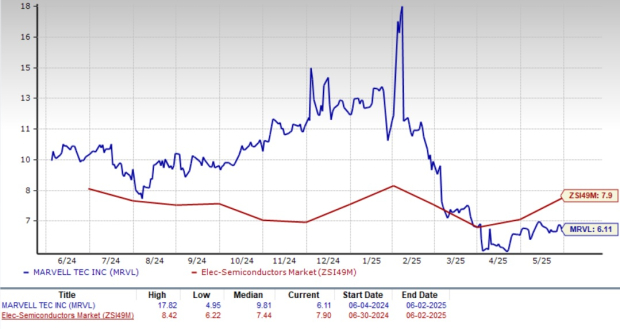

The price drop in stock price has brought Marvell Technology to a forward 12-month price-to-sales (P/S) multiple of 6.11x, significantly below its one-year median of 9.82x as well as the Zacks Electronics – Semiconductors industry’s average of 7.90x. This valuation discount makes Marvell Technology an appealing buy for investors looking for exposure to AI and high-performance computing at a more reasonable price.

MRVL stock is also trading at a discounted valuation than its peers like Broadcom and Ambarella’s forward 12-month P/S ratios of 17.13x and 6.11x, while Qualcomm trades at 3.67x, which is at a lower valuation than Marvell Technology at present.

Marvell Technology is facing several headwinds, including U.S.-China tension and the United States’ new tax policies, raising costs for MRVL. Shrunken margins and the entry of big players in the automotive market will further challenge Marvell Technology’s growth.

However, the company has strong long-term fundamentals supported by its strong foothold in the data center and high-speed networking market. Marvell Technology’s investment in AI has endowed it with long-term potential. Considering all these factors, we suggest retaining MRVL stock at present.

Marvell Technology carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 10 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite