|

|

|

|

|||||

|

|

|

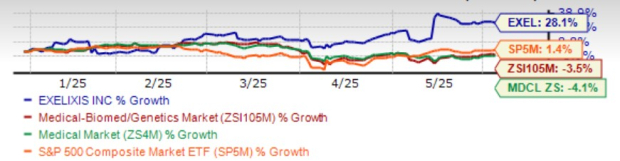

Exelixis EXEL has performed well this year. Shares of the biotech company have gained 28.1% year to date against the industry’s decline of 3.5%. The stock has outperformed the sector and the S&P 500 Index in this timeframe.

The company's upbeat performance can be attributed to its strong quarterly results, raised guidance, label expansion of Cabometyx (cabozantinib) and efforts to increase shareholders' returns.

In March, the FDA expanded Cabometyx's label for patients with previously treated advanced neuroendocrine tumors (NET).

Let’s delve deeper and analyze the company’s strengths and weaknesses to make an informed decision on the stock.

Exelixis’ lead drug Cabometyx maintains its status as the leading tyrosine kinase inhibitor (TKI) for the treatment of renal cell carcinoma (RCC) in both the frontline immuno-oncology (IO) +TKI market and the second-line monotherapy segment.

Cabometyx is also approved for use in combination with Bristol Myers’ BMY Opdivo in the first-line setting in RCC. Demand has been strong for this combination, boosting sales.

BMY’s Opdivo is one of the leading IO drugs, and has been approved for various oncology indications.

Cabometyx is also approved for the treatment of hepatocellular carcinoma.

Given the strong momentum of Cabometyx in the first quarter, EXEL raised its annual guidance for net product revenues and total revenues by $100 million.

The recent label expansion of cabozantinib for adult and pediatric patients 12 years of age and older with previously treated, unresectable, locally advanced or metastatic, well-differentiated pancreatic NET (pNET) and those with previously treated advanced extra-pancreatic NET should further fuel sales.

Cabometyx is now the first and only systemic treatment that is FDA approved for previously treated NET regardless of primary tumor site, grade, somatostatin receptor expression and functional status.

The pipeline progress has been impressive as well, as Exelixis looks to expand its oncology portfolio beyond Cabometyx.

The company is now focused on developing zanzalintinib, a next-generation oral TKI. Results from an expansion cohort of the phase Ib/II STELLAR-001 study evaluating zanzalintinib alone or in combination with Tecentriq (atezolizumab) in patients with previously treated metastatic colorectal cancer (CRC) were encouraging.

Results showed that all efficacy parameters, including objective response rate, PFS and overall survival, favored the combination of zanzalintinib plus Tecentriq versus zanzalintinib monotherapy in the overall population as well as in a subgroup of patients without liver metastases.

The data support zanzalintinib’s ongoing pivotal development in metastatic CRC.

Meanwhile, Exelixis collaborated with pharma giant Merck MRK to evaluate zanzalintinib in combination with its blockbuster anti-PD-1 therapy Keytruda (pembrolizumab) in a late-stage study for treating patients with head and neck squamous cell carcinoma (HNSCC).

Per the terms of the agreement, Merck is supplying Keytruda for the ongoing, Exelixis-sponsored phase III STELLAR-305 study in previously untreated PD-L1-positive recurrent or metastatic HNSCC.

In April, Exelixis presented preclinical data from four pipeline candidates. Data on XL309, XB628 and XB371 were encouraging. Exelixis is on track to submit an investigational new drug application (IND) application for XB371 to the FDA in 2025.

The successful development of additional drugs should broaden its portfolio and reduce its dependence on its lead drug, Cabometyx.

Exelixis is also making efforts to increase shareholder value through repurchases. In August 2024, the board authorized a stock repurchase program to acquire up to $500 million of the company’s common stock before Dec. 31, 2025. In February 2025, another share buyback program for an additional $500 was authorized.

Under these programs, as of March 31, 2025, Exelixis repurchased $494.5 million of the company’s common stock.

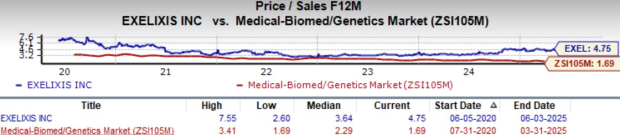

From a valuation standpoint, EXEL is expensive. Going by the price/sales ratio, its shares currently trade at 4.75x forward sales, higher than its mean of 3.64x and the biotech industry’s 1.69x.

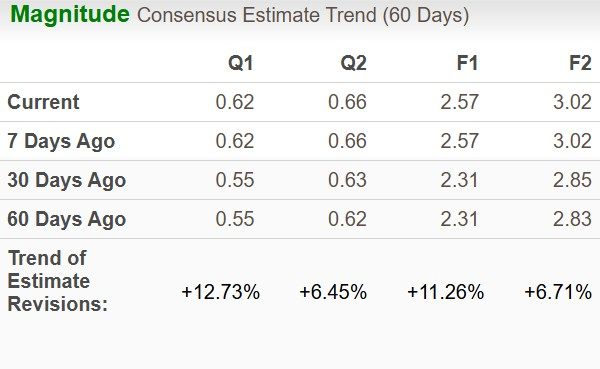

The bottom-line estimate for 2025 has risen from $2.31 to $2.57, while that for 2026 has increased to $3.02 from $2.85 over the past 30 days.

Large biotech companies are generally considered safe havens for investors interested in this sector. Exelixis' lead drug, Cabometyx, maintains momentum for the company. The label expansion of Cabometyx should boost its growth. The company’s efforts to expand its portfolio are encouraging as well. The successful development of additional drugs should broaden its portfolio and reduce its dependence on its lead drug.

The company’s efforts to increase shareholder value are impressive and should boost returns.

EXEL is a good stock to buy now, considering its good fundamentals and growth prospects. We recommend the stock to investors as we believe there is more room for growth.

EXEL currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite