|

|

|

|

|||||

|

|

|

General Motors GM and Toyota Motor TM are two of the biggest names in the global auto industry and fierce rivals in the U.S. market. GM often leads the pack as the top-selling automaker in the country, while Toyota usually comes in a close second. In 2024, GM sold over 2.7 million vehicles in the United States, up 4% year over year. Toyota wasn’t far behind, delivering 2.33 million units, a 3.7% increase from 2023.

Globally, Toyota holds a clear edge. The Japanese automaker sold 10.8 million vehicles worldwide last year, compared to GM’s 6 million. Toyota’s scale and steady performance are reflected in its market value—around $255 billion—while GM trades at just under $50 billion.

Year to date, shares of Toyota have declined 1.7%, compared with GM’s decline of 8%. The auto sector has lost 10% over the same timeframe.

Let’s take a closer look at their fundamentals, growth catalysts and looming risks to determine which automaker is a better choice for investors now.

General Motors is holding its ground but cracks are starting to show. The automaker managed to beat earnings expectations once again in the last reported quarter—a sign of resilience—but the near-term outlook is getting cloudier.

Tariff pressure under Trump’s presidency forced GM to revise its full-year outlook. The company now expects adjusted EBIT of $10 billion to $12.5 billion, down sharply from its earlier range of $13.7 billion to $15.7 billion. Net income projections were cut as well. GM suspended its share buyback program after having $4.3 billion in repurchase capacity left at the end of the first quarter of 2025. That move has rattled some investors, raising questions about how well GM is positioned to absorb the tariff blow.

The company is also vulnerable to supply chain disruptions. GM expects a $2 billion impact from South Korean operations alone, where vehicles like the Chevrolet Trailblazer and Buick Encore GX are built—models that made up nearly 18% of its first-quarter sales. Its reliance on manufacturing in Mexico and Canada adds another layer of uncertainty.

Even as GM pushes forward on its electric vehicle ambitions, the payoff remains uncertain. The company was the second-largest EV seller in the United States last quarter, and Chevrolet is now the fastest-growing EV brand. It also managed to make its EV lineup "variable profit positive" by the end of 2024, which means it now covers basic production costs. Still, that’s a long way from achieving healthy margins, and progress will take time.

Heavy investment in EVs, battery tech, and software continues to eat into GM’s free cash flow. The company has lowered its adjusted automotive free cash flow forecast to $7.5-$10 billion, down from $11-$13 billion. While GM does have a strong cash position—$20.7 billion at the end of the first quarter of 2025—its financial flexibility could tighten if global risks escalate further.

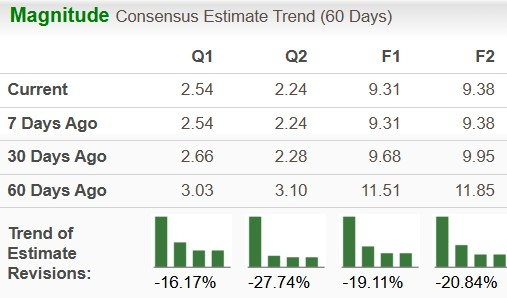

GM’s long-term vision remains intact, but the road ahead is looking bumpy. The Zacks Consensus Estimate for GM’s 2025 sales and earnings implies a year-over-year decline of 5.3% and 12%, respectively.

EPS estimates for GM have been revised downward over the past 60 days.

Toyota continues to show why it’s considered one of the most dependable players in the global auto space. The company topped earnings expectations in its last reported quarter and expects to grow both sales volumes and revenues in fiscal 2026 (ending on March 31, 2026). However, profits may come under pressure as new challenges emerge.

Toyota forecasts a 21% drop in operating income for fiscal 2026. That’s largely due to rising material costs, a stronger yen and the impact of Trump’s tariffs. Higher vehicle prices could hurt consumer sentiment and weigh on demand, especially in key markets like the United States.

On the bright side, Toyota expects to sell 9.8 million vehicles in fiscal 2026, up from 9.36 million in fiscal 2025. Including Lexus, total sales are projected to reach 10.4 million units. Electrified vehicles—including hybrids and plug-ins—are a major driver, with expected sales rising to 5.18 million units, up from 4.75 million last year. That momentum is reflected in revenue forecasts, with sales projected to rise slightly to ¥48.5 trillion in fiscal 2026.

Toyota’s hybrid-first strategy is clearly resonating with buyers. RAV4, America’s top-selling SUV, is now available only as a hybrid or plug-in hybrid model starting in 2026. By ditching the gas-only version, Toyota is doubling down on efficient, accessible electrification—something that stands out as BEV adoption is expensive. Beyond hybrids, Toyota is also making big moves in hydrogen. It’s focused on expanding commercial vehicle use and scaling hydrogen infrastructure to cut costs over time.

Meanwhile, Toyota is keeping investors happy. It raised its annual dividend to 90 yen per share in fiscal 2025 and expects to increase it to 95 yen in fiscal 2026. With consistent dividend growth and a measured approach to electrification, Toyota remains a steady and strategic player in an uncertain auto landscape.

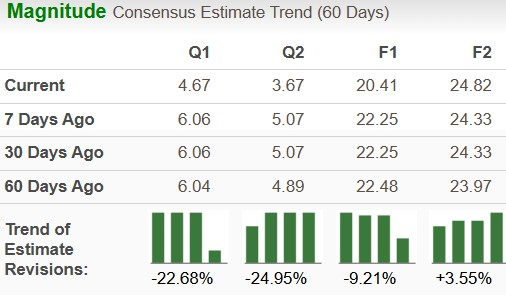

The Zacks Consensus Estimate for TM’s sales in fiscal 2026 implies 6% growth year over year. The consensus mark for EPS, however, implies a decline of 13.5% year over year. While fiscal 2026 estimates for TM have moved down over the past 60 days, fiscal 2027 estimates have moved up.

Our Take: TM Over GM

Both General Motors and Toyota are navigating a tough macro environment with tariffs and rising costs squeezing profitability. GM is making steady progress in EVs and holds a strong position in the U.S. market, but near-term challenges and reduced financial forecasts have clouded its outlook.

Toyota, meanwhile, continues to flex its global scale, hybrid dominance, and disciplined strategy—even as profit growth stalls. Its steady top-line momentum, growing electrified sales, and dividend growth are appealing. While GM has potential, Toyota’s fundamentals and strategy look stronger now.

Toyota currently carries a Zacks Rank #3 (Hold), while GM carries a Zacks Rank of 5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Steel and Aluminum Stocks Fall, Automakers Gain After Reports of Tariff Pullback

TM GM

The Wall Street Journal

|

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite