|

|

|

|

|||||

|

|

|

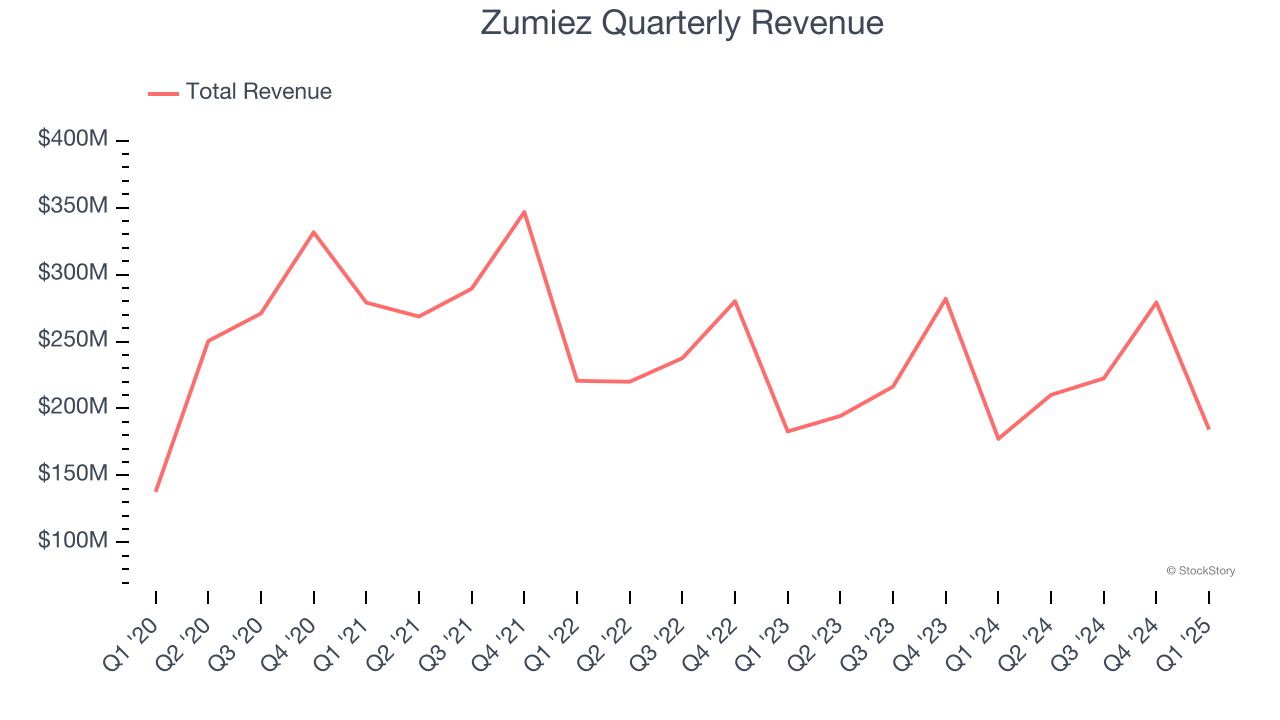

Clothing and footwear retailer Zumiez (NASDAQ:ZUMZ) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 3.9% year on year to $184.3 million. Guidance for next quarter’s revenue was better than expected at $210.5 million at the midpoint, 1.3% above analysts’ estimates. Its GAAP loss of $0.79 per share was 3% below analysts’ consensus estimates.

Is now the time to buy Zumiez? Find out by accessing our full research report, it’s free.

Rick Brooks, Chief Executive Officer of Zumiez Inc., stated, “Our North American business showed resilience during the first quarter despite increased macroeconomic uncertainty following the implementation of higher tariffs. Consumers continue to respond positively to our merchandise assortments and shopping experience evidenced by strong full price selling that drove sales growth above the Q4 run rate for North America. In response to the current global trade environment, we have further diversified our North America supply chain and expect a meaningful reduction in exposure to China by the end of this year. While the potential impact on consumer sentiment from ongoing trade negotiations is unknown, we are pleased with our current momentum in North America and confident in our ability to outperform the market over the remainder of the year. Internationally, our business was tougher in the first quarter with sales turning slightly negative. We remain focused on introducing new and unique products to drive demand while controlling costs to improve margins. Consolidated results, removing the previously mentioned unplanned legal charge, exceeded the high end our guidance for both Sales and loss per share while also showing meaningful improvement to the prior year.”

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ:ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $896.2 million in revenue over the past 12 months, Zumiez is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Zumiez’s revenue declined by 1.6% per year over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it closed stores.

This quarter, Zumiez reported modest year-on-year revenue growth of 3.9% but beat Wall Street’s estimates by 1.2%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products will catalyze better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

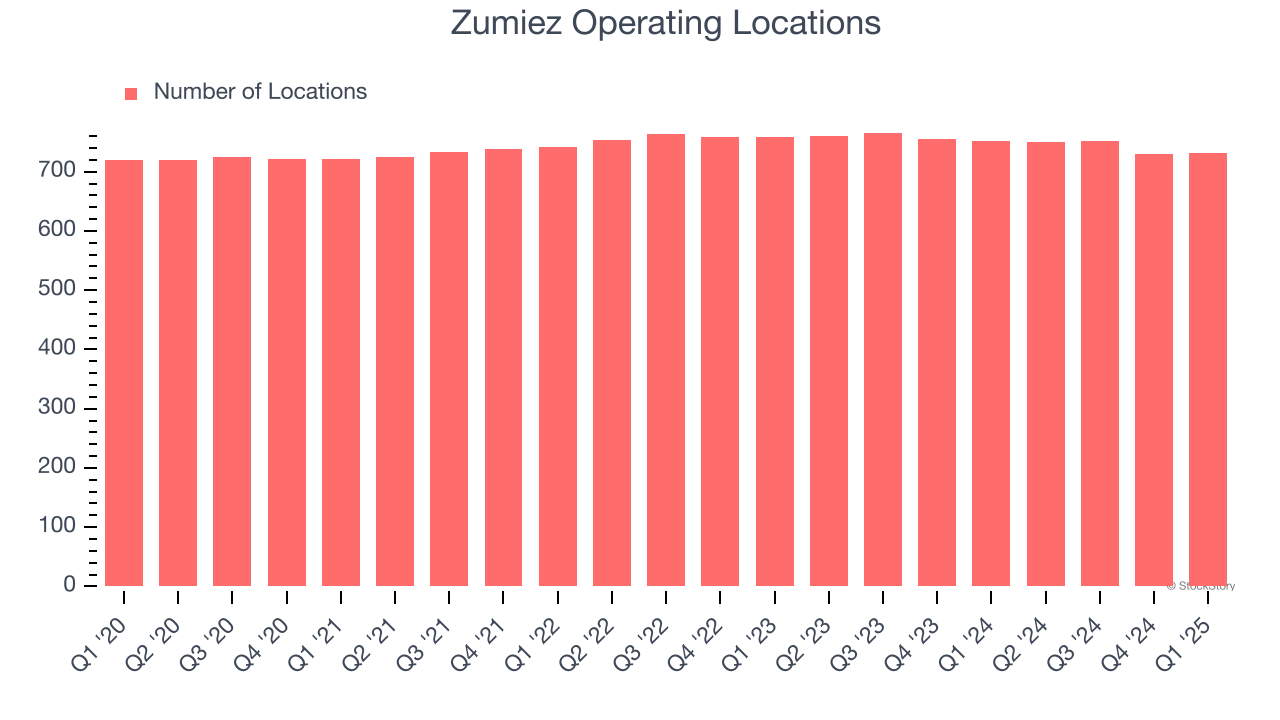

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Zumiez operated 731 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 1.1% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

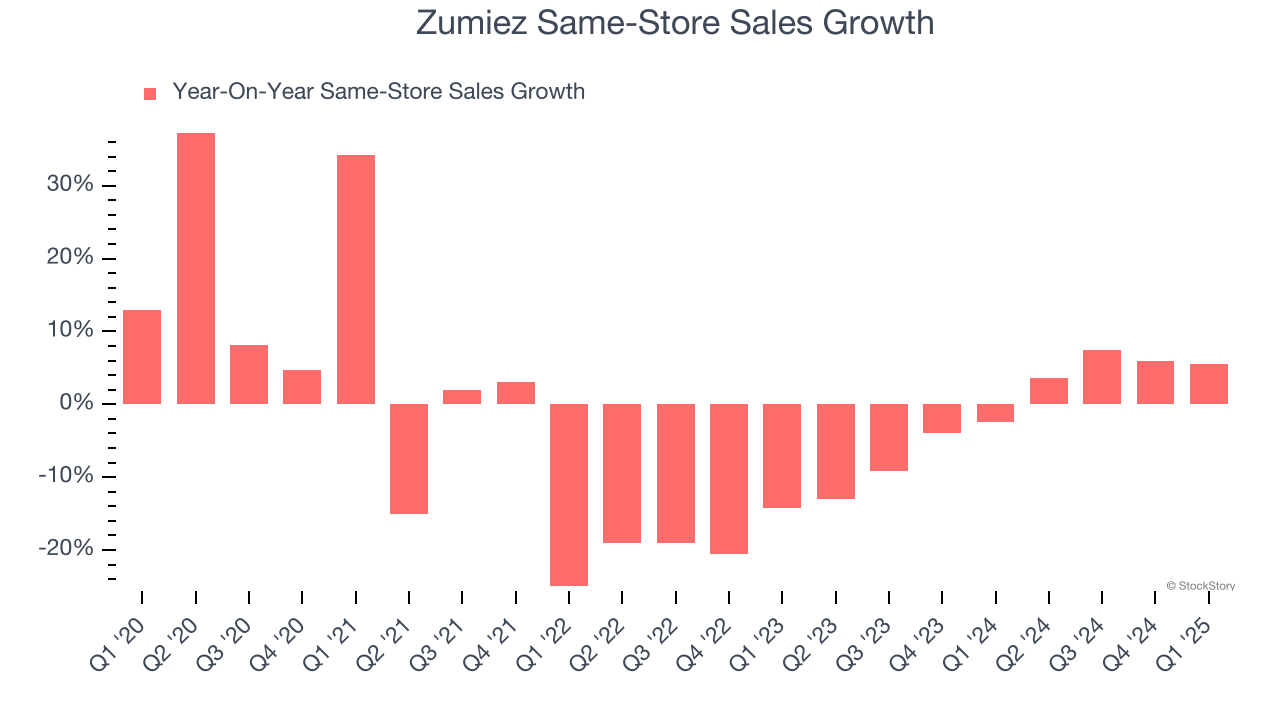

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Zumiez’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Zumiez is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Zumiez’s same-store sales rose 5.5% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

It was good to see Zumiez narrowly top analysts’ revenue expectations this quarter. We were also glad its revenue guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its EBITDA missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.2% to $12.45 immediately following the results.

Zumiez may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Jun-05 | |

| Jun-04 | |

| Jun-04 | |

| Jun-02 | |

| May-21 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-10 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite