|

|

|

|

|||||

|

|

|

I like to keep things simple—I look for stocks that have strong price momentum, top Zacks Ranks, reasonable valuations and high growth forecasts. Momentum indicates that the market recognizes a winner, the Zacks rank reflects improving analyst expectations, a reasonable valuation limits downside risk and growth is what ultimately drives stock returns. When a stock checks all these boxes, and flies under the radar, that’s even better.

Olo (OLO), Palomar Holdings (PLMR) and Exelixis (EXEL) all fit this profile and represent a diverse range of industries. Below, I will lay out why investors may consider investing in one, or all of these non-consensus stocks.

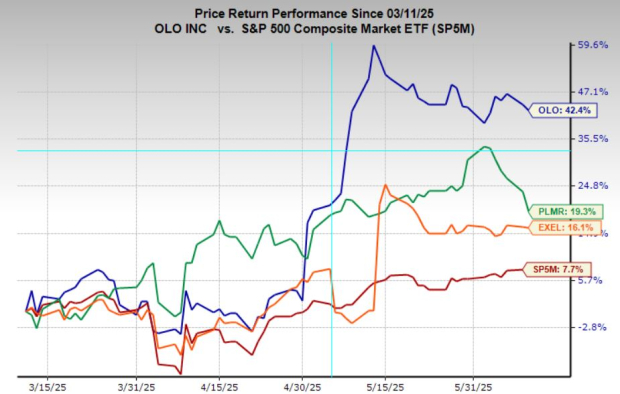

Olo is a software-as-a-service (SaaS) provider that helps restaurants streamline digital ordering, delivery, and customer engagement. The company serves some of the most recognizable brands in the foodservice industry, offering an end-to-end platform that integrates seamlessly with restaurants’ operations. After years of unprofitable growth, Olo is now emerging as a turnaround story, making it one of my favorite setups: a stock that was beaten down but is now showing a rapid inflection of profitability.

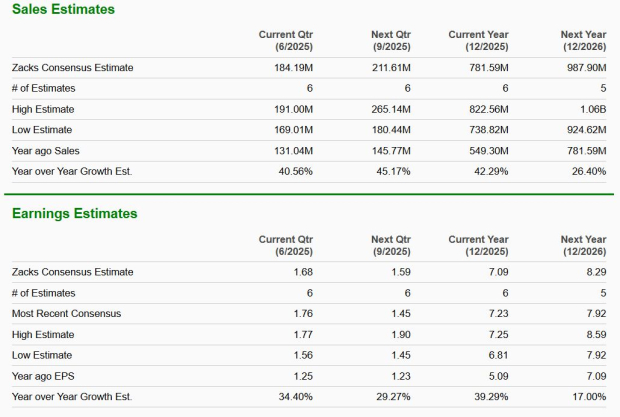

Currently holding a Zacks Rank #2 (Buy), Olo is benefitting from a wave of upward earnings revisions. Revenue is expected to climb 19.1% this year and 17.6% next year, while earnings are forecast to rise 41% this year and another 18.3% next year. With a forward earnings multiple of 23.6x, Olo is trading at a reasonable valuation for a business with expanding margins, impressive growth and strong business economics.

On the technical front, the stock looks poised for a breakout. After a strong rally in May, OLO has been consolidating in a tight bull flag pattern as it digestion some gains. A clean breakout above the $8.95 resistance level could trigger another leg higher, supported by strong momentum. For investors looking for a high-growth turnaround story with both technical and fundamental appeal, Olo is worth watching closely.

Palomar Holdings is a specialty insurer focused on underwriting property and casualty risks, particularly in underserved or complex markets like earthquake, hurricane, and specialty commercial insurance.

Over the past few years, I’ve grown increasingly attracted the insurance sector. The combination of pricing power, recurring revenue, and an exceptional business model has made insurers some of the most consistent performers in the market. Palomar is a standout in that already strong group, and despite strong stock gains, its valuation remains reasonable.

Currently holding a Zacks Rank #1 (Strong Buy), Palomar is seeing sharp upward earnings estimate revisions. The company is expected to grow EPS by 39.9% this year and another 17% in 2025. Sales are also surging, with revenue forecast to rise 42.3% this year and 26.4% next year. Yet, PLMR trades at just 18.8x forward earnings, offering a compelling valuation relative to its growth forecasts.

After gaining over 180% in the last 18 months, Palomar’s stock is currently in the midst of what appears to be a healthy pullback. Given the company’s strong fundamentals, upward earnings momentum, and continued top-line acceleration, this dip looks more like a buying opportunity than a reason for concern. Investors looking for growth at a reasonable price in a defensive sector should keep a close eye on PLMR.

Exelixis is a biotechnology company focused on developing and commercializing cancer treatments, including its flagship therapy Cabometyx, which is approved for multiple tumor types. The company has built a robust oncology pipeline and continues to reinvest in innovation while maintaining profitability—a rare combination in the biotech space.

Exelixis currently holds a Zacks Rank #2 (Buy), driven by rising earnings estimates. Over the past month, FY25 EPS estimates have been raised by 13%, while FY26 estimates are up 7.1%, reflecting increasing confidence in the company’s growth outlook. Analysts expect earnings to grow at a healthy 21.2% annually over the next three to five years. Despite this impressive growth profile, EXEL trades at just 16.5x forward earnings, giving it a very attractive PEG ratio of 0.78, and an appealing setup for GARP (Growth at a Reasonable Price) investors.

On the technical side, the stock is showing signs of building momentum. After trending snapping higher last month, EXEL is coiling into a bullish continuation pattern. A breakout above the $43.70 level would mark a technical breakout and could trigger a wave of momentum buying, especially given the supportive fundamental backdrop. With both growth and valuation on its side, Exelixis presents a rare opportunity in biotech: a profitable company with strong upside potential and limited valuation risk.

Each of these underfollowed stocks, Exelixis, Olo, and Palomar Holdings, offers a compelling mix of strong fundamentals, favorable earnings revisions, and attractive valuations. They also bring the added benefit of price momentum, signaling growing institutional interest. While they operate in very different industries, they share the same core traits: improving outlooks, reasonable prices, and room to run. For investors seeking high-potential, non-consensus opportunities, these names deserve a closer look.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-30 | |

| Mar-06 | |

| Mar-05 | |

| Mar-02 | |

| Mar-02 | |

| Mar-02 | |

| Feb-26 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-20 | |

| Feb-18 | |

| Feb-18 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite