|

|

|

|

|||||

|

|

|

Insulet Corporation’s PODD rapid commercial expansion of its Omnipod platform is poised to help it grow in the upcoming quarters. The rising adoption of Omnipod 5 also presents a promising growth opportunity. Meanwhile, adverse macroeconomic impacts and fierce competition raise concerns for Omnipod’s operations.

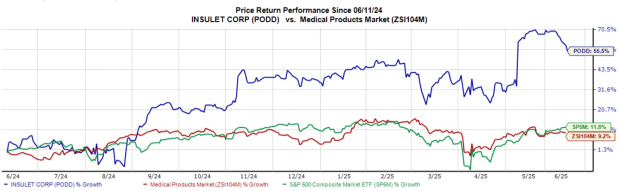

In the past year, this Zacks Rank #3 (Hold) stock has risen 55.5%, outperforming the industry’s 9.2% growth and S&P 500 composite’s gain of 11.8%.

The developer, manufacturer and distributor of insulin delivery systems has a market capitalization of $21.51 billion. PODD’s earnings surpassed estimates in three of the trailing four quarters and missed in one, delivering an average surprise of 12.21%.

Let’s delve deeper.

Omnipod 5, a New Focus: Insulet’s game-changing Omnipod 5 stands out as the only FDA-cleared, fully disposable pod-based AID system. Consistent with expectations, Omnipod 5 maintained strong momentum in new customer starts in the United States and grew both sequentially and year over year in the first quarter.

Approximately 85% of new starts came from people previously using MDI, Insulet’s target market, while competitive conversions remained strong. Notably, Type 2 users represented over 30% of U.S. new customer starts in the first quarter. The Type 2 indication has significantly expanded Insulet’s total addressable market by making Omnipod 5 commercially available to more than 5.5 million people in the United States.

Focus on Market Expansion: Insulet is expanding its global presence in a targeted and strategic manner. The company is now transitioning from Omnipod GO to Omnipod 5 as its primary offering for people with type 2 diabetes on basal-only insulin.

Omnipod 5 continues to drive strong adoption across all market segments. Following successful launches in France and the Netherlands last year, the product was introduced in five additional countries, namely Italy, Denmark, Finland, Norway and Sweden, in January 2025. It was also launched in Australia in March 2025.

Insulet plans to expand internationally with additional sensor options, including further rollouts of Omnipod 5 integrated with FreeStyle Libre 2 Plus and the upcoming integration with Dexcom G7 in the following quarters of 2025. Insulet anticipates further international launches of Omnipod 5 in 2025. The company expects to expand into Belgium and Switzerland with Abbott’s FreeStyle Libre 2 Plus and Dexcom G6 and G7 integrations, and into Canada with Dexcom G6 and G7 compatibility. Omnipod 5 will also become available in five more markets — Israel, Saudi Arabia, the United Arab Emirates, Qatar and Kuwait.

Economic Uncertainty Hampers Growth: The ongoing worldwide macroeconomic and geopolitical uncertainty may reduce demand for Insulet’s products, intensify competition, exert pressure on prices, dent supply and lengthen the sales cycle. In addition, Insulet continues to experience challenges stemming from the global supply-chain disruption. The reinstatement of China tariffs is expected to result in higher product costs during the remainder of 2025. In the first quarter of 2025, selling, general & administrative expenses rose 30.5% year over year.

Tough Competitive Pressure: Insulet operates in a highly competitive environment, dominated by firms ranging from large multinational corporations with significant resources to start-ups. PODD also competes with companies offering products and supplies for MDI therapy, which is currently the most prevalent method of insulin delivery. In addition, the competitive and regulatory conditions in the markets where the company operates limit Insulet’s ability to switch to strategies like price increases.

The Zacks Consensus Estimate for 2025 earnings per share (EPS) has moved south 1.4% to $4.34 in the past 30 days.

The Zacks Consensus Estimate for 2025 revenues is pegged at $2.52 billion, suggesting a 21.8% rise from the year-ago reported number.

Some better-ranked stocks in the broader medical space are Phibro Animal Health PAHC, Prestige Consumer Healthcare PBH and Inspire Medical Systems INSP.

Phibro Animal Health has an estimated long-term earnings growth rate of 26.2% compared with the industry’s 15.9%. Its earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 30.6%. Its shares have rallied 26.3% compared with the industry’s 10% growth in the past year.

PAHC flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Prestige Consumer Healthcare, currently carrying a Zacks Rank #2 (Buy), has an earnings yield of 5.4% compared with the industry’s 0.6%. Shares of the company have rallied 30.3% compared with the industry’s 10% growth. PBH’s earnings surpassed estimates in three of the trailing four quarters and matched on one occasion, the average surprise being 2.8%.

Inspire Medical Systems, carrying a Zacks Rank #2 at present, has an estimated long-term earnings growth rate of 28.9% compared with the industry’s 25.2%. Shares of the company have lost 9.5% against the industry’s 19.6% growth. INSP’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 356.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-20 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-06 | |

| Jul-01 | |

| Jun-30 | |

| Jun-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite