|

|

|

|

|||||

|

|

|

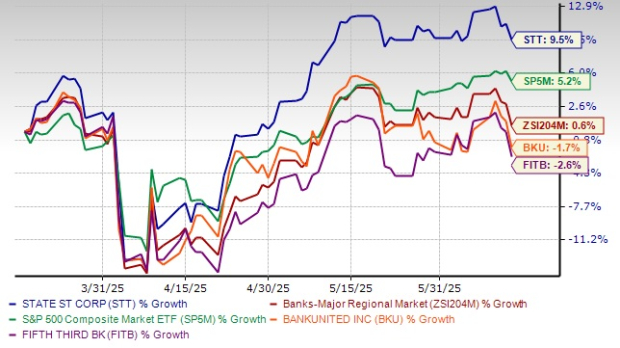

State Street Corporation STT shares have gained 9.5% in the past three months, outperforming the industry’s mere 0.6% growth and the S&P 500 Index’s 5.2% rise. Moreover, STT’s price performance has been better than that of its peers, BankUnited, Inc. BKU and Fifth Third Bancorp FITB. The BKU stock has lost 1.7%, whereas shares of FITB have declined 2.6% in the same time frame.

Does the State Street stock have more upside left despite showing recent strength in share price? Let us try to find out.

Acquisitions & Restructuring Efforts: State Street has been expanding its scale by undertaking acquisitions, business expansion and restructuring efforts. In May 2025, it collaborated with smallcase to cater to investors in India seeking global exposure. In April, the company partnered with Ethic Inc. to offer customized investment solutions to institutional and financial intermediary clients.

In February, it announced a deal to acquire global custody and related businesses outside of Japan from Mizuho Financial Group, Inc. Moreover, in November 2024, State Street Global Advisors joined forces with Bridgewater Associates to boost its core alternative investment strategies, while, in September, STT partnered with Apollo Global to enhance investors' accessibility to private markets.

Also, as part of its global business consolidation efforts, State Street has announced the restructuring of the nearly 20-year-old European component of the International Financial Data Services LP joint venture (JV) arrangement in Luxembourg and Ireland, consolidated its India-based operations and assumed the full ownership of its two JVs. These, along with past buyouts and expansion initiatives, are expected to continue to result in revenue and cost benefits, and help the company expand its footprint globally.

Fee Income Strength: Growth in State Street’s fee income has been impressive. While the company’s total fee revenues declined in 2022 and 2023, the metric saw a four-year (2020-2024) compound annual growth rate (CAGR) of 1.7%. This was mainly driven by higher client activity and significant market volatility.

Servicing assets yet to be installed were $3.5 trillion in 2021, $3.6 trillion in 2022, $2.3 trillion in 2023, and $3 trillion in 2024 across client segments and regions. As of March 31, 2025, servicing assets yet to be installed were $3.06 trillion. Also, assets under custody and administration (AUC/A) and assets under management (AUM) recorded a four-year (ended 2024) CAGR of 4.7% and 8%, respectively.

State Street remains well-positioned for fundamental business activities, given its global exposure and a broad array of innovative products and services (including the launch of State Street Digital and State Street Alpha). The company’s business servicing wins and its inorganic growth strategy are expected to continue to aid fee revenues.

Relatively Higher Interest Rates: In a relatively high-interest rate backdrop, State Street has been witnessing an increase in its net interest income (NII). NII recorded a four-year (ended 2024) CAGR of 7.4%. Given the company’s investment portfolio repositioning efforts, its NII is expected to improve in the quarters ahead.

Impressive Capital Distributions: Following the clearance of the 2024 stress test, State Street increased its quarterly dividend by 10% to 76 cents per share. This was the fourth consecutive annual hike in dividend payout by 10%. In January 2024, the company was authorized to repurchase shares worth up to $5 billion (with no expiration date). As of March 31, 2025, almost $3.6 million worth of authorization remained available.

STT plans to return approximately 80% of earnings to its shareholders this year, with a step-up in repurchase activity in the second quarter of 2025. Driven by a strong capital position and earnings strength, the company is expected to sustain improved capital distributions in the future, enhancing shareholder value.

Elevated Expense Base: Despite a marginal decline in expenses in 2022 and 2024, STT’s total non-interest expenses witnessed a four-year (ended 2024) CAGR of 2.3%. Last year, the company was successful in managing expenses through high-cost location workforce reduction, business consolidation and restructuring initiatives. These efforts resulted in almost $550 million in gross cost savings.

However, expenses are likely to remain elevated owing to higher information systems and communications expenses. Also, inflationary pressure and the company’s strategic buyouts and investments in franchises will put pressure on expenses.

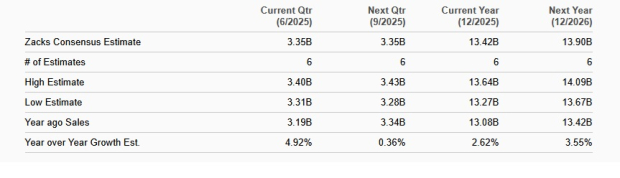

Fee Income Concentration: State Street’s largest revenue source is fee income, which constituted 78.3% of total revenues in the first quarter of 2025. Though fee income majorly supported the company’s top line in 2024, significant volatility in the capital markets is worrisome, putting a strain on the metric’s future trajectory.

Also, concentration risk arising from higher dependence on fee-based revenues can significantly alter the company’s financial position if there is any change in individual investment preferences, regulatory amendments or a slowdown in capital markets activities.

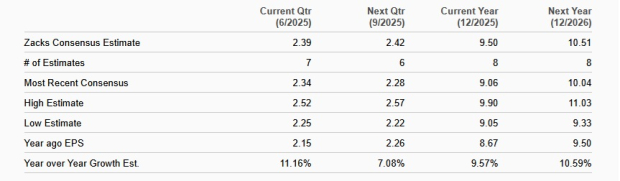

Solid business servicing wins, a global footprint, and strategic buyouts and alliances will likely continue to aid STT’s fee income growth. Rising AUM balance will drive its top line and higher interest rates will likely support NII growth.

However, elevated costs due to continuous investments in franchises and inflationary pressure will hurt State Street's bottom line. The company's high dependence on fee income sources is another major concern.

Hence, investors should not rush to buy the STT stock now; instead, they should keep this Zacks Rank #3 (Hold) stock on their radars and wait for an attractive entry point. Those who already own State Street stock in their portfolio can hold on to it because it is less likely to disappoint over the long term, given its strong fundamentals.

You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 10 hours | |

| Feb-25 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite