|

|

|

|

|||||

|

|

|

onsemi’s stock price has taken a beating over the past six months, shedding 21% of its value and falling to $53.49 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in onsemi, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're cautious about onsemi. Here are three reasons why ON doesn't excite us and a stock we'd rather own.

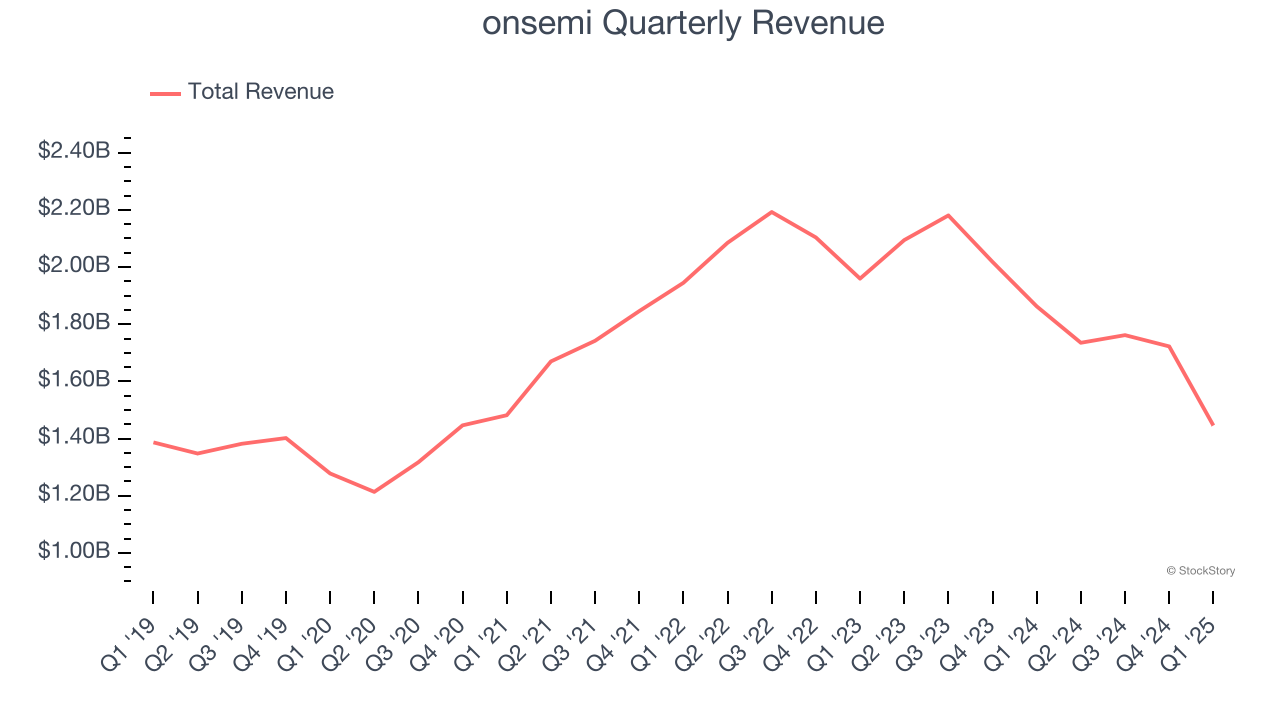

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, onsemi grew its sales at a sluggish 4.3% compounded annual growth rate. This was below our standard for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect onsemi’s revenue to drop by 10.2%, close to its 4.3% annualized growth for the past five years. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

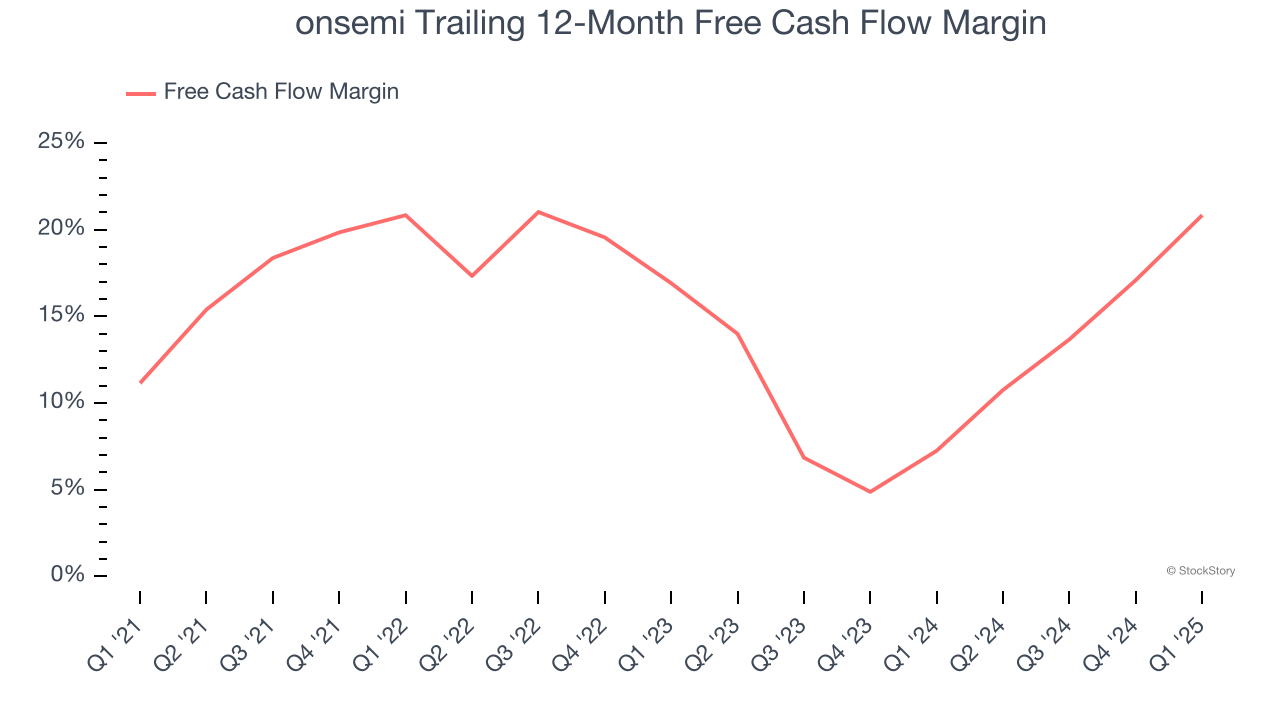

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

onsemi has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 13.4%, subpar for a semiconductor business. The divergence from its good operating margin stems from its capital-intensive business model, which requires onsemi to make large cash investments in working capital and capital expenditures.

onsemi isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 19.7× forward P/E (or $53.49 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| 6 hours | |

| Feb-16 | |

| Feb-16 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 |

Stock Market Today: Dow Closes At Another Record High; Nasdaq Breaks Win Streak (Live Coverage)

ON

Investor's Business Daily

|

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Stock Market Today: Dow Hits Record High; Chip Equipment Name Soars (Live Coverage)

ON

Investor's Business Daily

|

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite