|

|

|

|

|||||

|

|

|

Under Armour, Inc. UAA reported a gross margin of 46.7% for the fourth quarter of fiscal 2025, representing a year-over-year increase of 170 basis points. This improvement was primarily driven by lower product and freight costs, which contributed 150 basis points, along with a reduction in discounting and promotional activity within the direct-to-consumer (DTC) channel, adding 80 basis points.

Additional benefits came from improved royalty terms and favorable impacts from foreign currency and product mix, which together contributed 20 basis points. These gains were partially offset by a 90-basis-point decline due to unfavorable regional and channel mix.

For fiscal 2025, the gross margin was 47.9%, up 180 basis points from the previous year. Key drivers were reduced supply-chain costs (both freight and product-related) and a strategic reduction in discounting, especially online. This margin expansion surpassed the company’s original outlook and was a significant positive in a year of declining revenue.

The margin improvements reflect a strategic shift. Under Armour is deliberately focusing on "higher quality revenue" and regaining pricing power, which means selling at full price instead of relying on markdowns. This is central to the company’s brand elevation strategy. It is reducing promotions, especially in DTC channels, and is investing in better storytelling and marketing to justify its full price positioning.

In the first quarter of fiscal 2026, the company anticipates year-over-year gross margin expansion of 40-60 basis points, driven by favorable product mix, continued supply-chain cost efficiencies, and currency benefits.

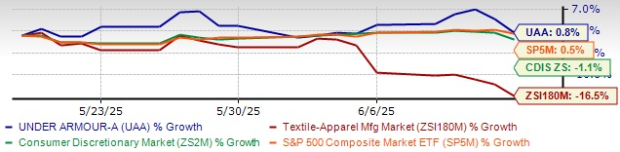

UAA Stock's Past-Month Performance

Under Armour’s ongoing restructuring program is playing a pivotal role in improving operating efficiency and supporting long-term margin expansion. In fiscal 2025, the company recorded $89 million in transformation and restructuring charges. Despite the upfront costs, the initiatives yielded $35 million in actual savings in the year, with expectations to reach a $75-million annualized cost-saving run-rate by the end of fiscal 2026.

These savings are primarily driven by reductions in consulting fees, travel expenses and third-party services, as well as operational streamlining measures, including the closure of the Rialto distribution center.

Selling, general and administrative (SG&A) expenses are projected to decline 40% from that reported in the prior-year quarter, which included a $274-million litigation settlement. When excluding the one-time impacts of last year’s settlement and anticipated transformation costs associated with the fiscal 2025 Restructuring Plan, adjusted SG&A is expected to exhibit slight leverage.

This improvement in cost management reflects disciplined spending and enhanced productivity across the organization. The combination of restructuring-driven savings and tighter cost control positions Under Armour to support gross margin gains and improve overall profitability.

Shares of this Zacks Rank #3 (Hold) company have gained 0.8% in the past month against the Zacks Textile – Apparel industry’s sharp 16.5% decline. The company’s ongoing strategic initiative and operational efficiencies have enabled it to outperform the broader Consumer Discretionary sector and the S&P 500 index’s decline of 1.1% and growth of 0.5%, respectively, during the same period.

Some better-ranked stocks are Stitch Fix SFIX, Canada Goose GOOS, and Allbirds Inc. BIRD.

Stitch Fix delivers customized shipments of apparel, shoes and accessories for women, men and kids. It carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

The Zacks Consensus Estimate for Stitch Fix’s current fiscal year’s earnings implies growth of 69.7% from the year-ago actuals. SFIX delivered a trailing four-quarter average earnings surprise of 51.4%.

Canada Goose is a global outerwear brand. GOOS is a designer, manufacturer, distributor and retailer of premium outerwear for men, women and children. It carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Canada Goose’s current fiscal year’s earnings and sales indicates growth of 10% and 2.9%, respectively, from the year-ago actuals. Canada Goose delivered a trailing four-quarter average earnings surprise of 57.2%.

Allbirds is a lifestyle brand that uses naturally derived materials to make footwear and apparel products. It carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for BIRD’s current financial-year earnings implies growth of 16.1% from the year-ago actual. The company delivered a trailing four-quarter average earnings surprise of 21.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 hours | |

| 18 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite