|

|

|

|

|||||

|

|

|

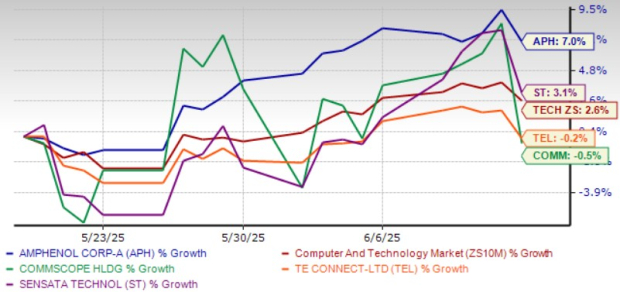

Amphenol APH shares have risen 7% over the past month, outperforming the Zacks Computer & Technology sector’s appreciation of 2.5%. The outperformance can be attributed to Amphenol’s diversified business model that lowers the volatility of individual end markets and geographies. APH’s wide array of interconnect and sensor products boosts long-term prospects.

APH has outperformed its closest peers, including CommScope COMM, TE Connectivity TEL and Sensata Technologies Holding ST, in the past month. While shares of Sensata Technologies Holding have returned 3.1%, CommScope and TE Connectivity have dropped 0.5% and 0.2%, respectively.

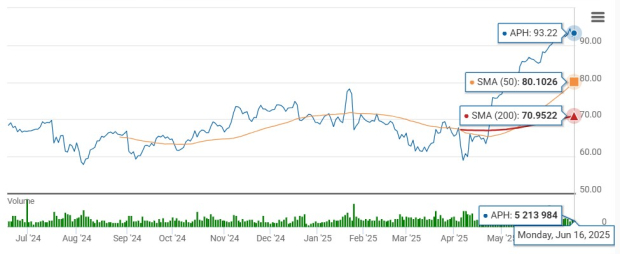

The stock is currently trading above the 50-day and the 200-day moving averages, indicating a bullish trend.

So, is APH stock a buy right now? Let’s analyze.

Amphenol’s long-term prospects benefit from strong spending by countries around next-generation defense technologies. The company expects second-quarter 2025 sales to increase in the high-single-digit range sequentially. Strong demand for jetliners and next-gen aircraft is bullish for the commercial aerospace segment.

Amphenol plans to expand its high-technology interconnect antenna and sensor offerings, both organically and through complementary acquisitions in the industrial domain. Industrial sales accounted for 20% of first-quarter 2025 net sales, and grew 20% in U.S. dollars and 6% organically. Sequentially, net sales increased 1%. Amphenol expects second-quarter 2025 sales to be roughly at this level.

Communications (comprising broadband and mobile networks markets) accounted for 10% of net sales in the first quarter of 2025, and net sales surged 107%, driven by the addition of the Andrew business. Amphenol expects sales to increase in the high-teens range sequentially, driven by the full quarter addition of Andrew.

The company’s solutions are critical for both high-speed power and fiber optic interconnect solutions. The growing use of AI and machine learning is driving these technologies, benefiting APH’s long-term prospects in the IT datacom end market. As demand grows for high-bandwidth, low-latency solutions across AI, cloud and enterprise environments, Amphenol expects the datacom vertical to remain a key catalyst to overall growth within its Communications Solutions segment.

Acquisitions have helped APH strengthen its product offerings and expand its customer base. The buyouts contributed 8% to 2024 revenues.

In May 2024, it completed the acquisition of CIT, which expanded Amphenol’s footprint across defense, commercial air and industrial end markets. The Lutze acquisition strengthens APH’s broad offering of high-technology interconnect products for industrial markets and expands the range of value-added interconnect products.

The acquisition of CommScope’s Andrew business expands Amphenol’s footprint in the areas of base station antennas and related interconnect solutions, as well as distributed antenna systems. The Andrew acquisition is expected to add roughly 9 cents to earnings in 2025. The acquisition of LifeSync, a leading provider of interconnect products for medical applications with annual sales of approximately $100 million, is noteworthy for APH’s prospects.

Amphenol offered positive second-quarter 2025 guidance. Earnings are now expected between 64 cents and 66 cents per share, indicating year-over-year growth between 45% and 50%. Sales are anticipated between $4.90 billion and $5 billion, suggesting year-over-year growth of 36-39%.

The Zacks Consensus Estimate for second-quarter 2025 earnings is pegged at 66 cents per share, up 20% over the past 60 days and indicating 53.49% growth over the year-ago quarter’s reported figure. The consensus mark for 2025 earnings is pegged at $2.68 per share, up 15% over the past 60 days and indicating 41.8% growth year over year.

Amphenol Corporation price-consensus-chart | Amphenol Corporation Quote

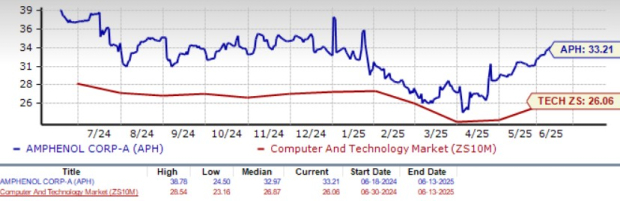

Amphenol shares are overvalued, as suggested by a Value Score of D. APH stock is trading at a significant premium with a forward 12-month Price/Earnings (P/E) of 33.21X compared with the sector’s 26.06X.

Amphenol shares are trading at a premium compared with CommScope, TE Connectivity and Sensata Technologies Holding, shares of which are trading at 5.74X, 18.49X and 8.19X, respectively.

Amphenol benefits from a diversified business model. APH’s strong portfolio of solutions, including high-technology interconnect products, is a key catalyst. These factors justify APH’s premium valuation.

Amphenol stock currently has a Zacks Rank #1 (Strong Buy) and a Growth Score of B, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 22 min | |

| Feb-27 |

Nvidia Collaborator And AI Data Center Play Holds Support Amid Market Sell-Off

TEL

Investor's Business Daily

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite