|

|

|

|

|||||

|

|

|

NVIDIA Corporation NVDA and Arm Holdings Plc ARM are two major semiconductor designers helping power the growth of artificial intelligence (AI). NVIDIA leads the GPU market and has become closely linked with AI training and inference. Arm Holdings is gaining importance with its AI-optimized CPU architectures, which are increasingly used in cloud and edge applications.

For investors looking to benefit from AI’s expansion, it’s important to compare these two companies and see which offers a stronger investment case today. Here’s a closer look at their strengths, risks, valuations and where they stand against each other.

NVIDIA is at the center of AI computing, with its products widely used across data centers, gaming and autonomous vehicles. The company continues to see strong demand from cloud providers, enterprises and startups building AI systems. In the first quarter of fiscal 2026, NVIDIA’s data center revenues rose 73% year over year to $39.1 billion, showing the strength of this part of its business.

Its newer Hopper 200 and Blackwell GPU platforms are being adopted quickly as customers work to grow their AI infrastructure. Much of this demand comes from large cloud providers that depend on NVIDIA GPUs for their AI workloads. The Blackwell architecture promises significantly higher performance, and upcoming versions like Blackwell Ultra and Vera Rubin are expected to strengthen NVIDIA’s position further as AI demand keeps growing.

However, the company faces near-term challenges from export restrictions. New U.S. rules stopped NVIDIA from selling its H20 chips to China, leading to lost sales of $2.5 billion in the first quarter. NVIDIA expects to lose another $8 billion in H20 sales during the second quarter. Despite the projected revenue loss from the Chinese market, the company is still on track for major growth, forecasting $45 billion in revenues (+/-2%) for the second quarter, representing 50% year-over-year growth.

Arm Holdings has long played a key role in the semiconductor industry, with its low-power chip designs widely used in smartphones and tablets. Big names like Apple, Qualcomm and Samsung continue to rely on ARM’s architecture.

Arm Holdings is positioned to benefit from the growing use of AI and the Internet of Things (IoT). Its energy-efficient chips are used in smart devices, autonomous systems and cloud infrastructure. As demand for scalable and power-saving solutions increases, ARM’s focus on AI-ready designs could support its future growth.

A key part of Arm Holdings’ model is its licensing and royalty setup, which brings in steady revenues without heavy capital spending. Its partnerships across industries help it maintain relevance in areas like automotive, data centers and consumer devices.

However, Arm Holdings faces challenges from global trade issues and tariffs. About 10-20% of its royalty revenues come from U.S. shipments, and higher tariffs could slow demand. Its exposure to China adds another risk, as local firms turn to RISC-V, an open-source chip technology backed by the Chinese government. This could weaken Arm Holdings’ share of the Chinese market over time.

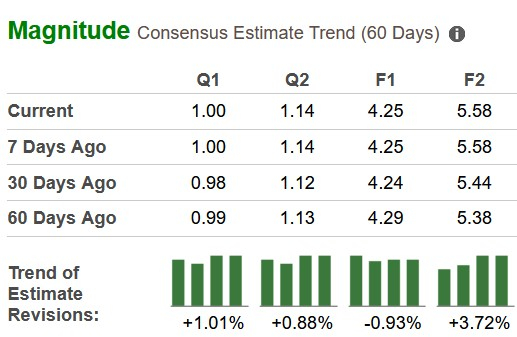

The Zacks Consensus Estimate projects NVIDIA’s earnings per share (EPS) to rise 42.1% in fiscal 2026 and 31.3% in fiscal 2027. Over the past 30 days, earnings estimates have been revised upward, showing strong confidence.

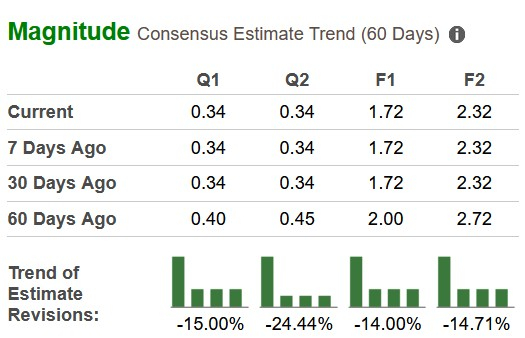

For Arm Holdings, EPS is expected to grow 5.5% in fiscal 2026 and 34.8% in 2027. However, the EPS estimate trend for ARM has been moving down over the last 60 days, reflecting less certainty about the near-term performance.

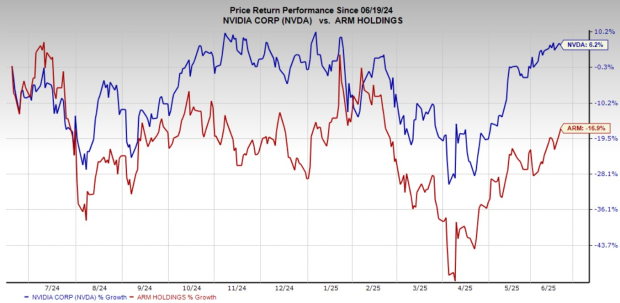

Both stocks have seen ups and downs over the past year due to macro uncertainty and geopolitical tension. NVIDIA shares have risen 6.2% over the past year, while Arm Holdings has declined 16.9%.

On the valuation front, NVIDIA trades at a more reasonable level. Its price-to-sales (P/S) multiple is 16.26X, far below Arm Holdings’ 31.2X. This suggests that NVIDIA offers better value relative to its growth potential.

Both NVIDIA and Arm Holdings are important to the AI chip market, but NVIDIA’s scale, technology leadership and ability to manage challenges give it the advantage right now. Arm’s growth story is solid, but concerns about tariffs, China exposure and a high valuation make NVIDIA the stronger choice for investors looking for more balanced risk and return in AI.

NVIDIA carries a Zacks Rank #3 (Hold), making it a clear winner over Arm Holdings, which has a Zacks Rank #4 (Sell) at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite