|

|

|

|

|||||

|

|

|

Mondelez International MDLZ entered 2025 facing one of the most formidable headwinds in its global supply chain: record cocoa inflation. While first-quarter 2025 organic revenues rose 3.1%, driven largely by strong pricing in its chocolate portfolio, the gains were not enough to shield gross profit from compression. The company’s gross profit declined significantly as cocoa prices soared to unprecedented highs, adding pressure on margins even amid robust retail execution.

Management emphasized a multipronged mitigation strategy built around pricing, revenue growth management and strategic pack architecture. Mondelez successfully implemented pricing across key markets with minimal disruption, indicating strong retailer alignment. Elasticity impacts, while present, were in line with expectations and suggest consumer loyalty to core brands like Oreo and Cadbury remains intact, especially where entry-level price points were preserved.

However, the first quarter numbers raise key questions about Mondelez’s ability to sustain profitability under prolonged commodity inflation. Volume mix declined 3.5% due to elasticity from chocolate pricing and planned pack downsizing. Notably, operating income in developed markets, particularly North America, was hurt by both cocoa cost pressure and soft consumer demand. In Europe, pricing landed well, but operating income erosion still occurred despite strong share gains.

Management noted that while some commodity inputs were procured favorably, the benefit was not enough to offset the cocoa’s impact. Even with strong cost controls and productivity gains, adjusted earnings per share dropped by double digits, underscoring the bottom-line strain.

Looking ahead, Mondelez is well-positioned to manage cocoa volatility. Strong pricing, effective cost controls and resilient brands support its margin strategy. As cocoa markets begin stabilizing, the company stands to benefit from improved leverage while reinvesting in long-term growth. Its disciplined execution underscores confidence in navigating near-term pressures and sustaining momentum in its core chocolate business.

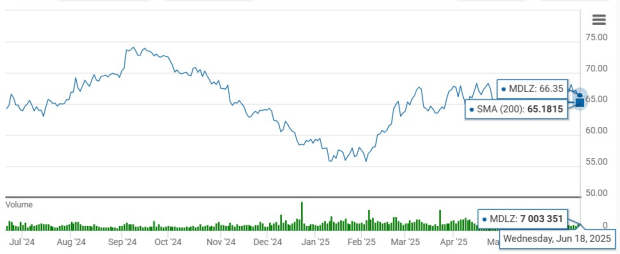

Shares of this Zacks Rank #2 (Buy) company have rallied 13.4% in the past six months against the industry’s 4% decline. MDLZ outperformed the broader Consumer Staples sector and the S&P 500 index’s growth of 5.9% and 1.1%, respectively, during the same period.

Closing yesterday’s trading session at $66.35, the MDLZ stock is trading 12.8% below its 52-week high of $76.06 attained on Sept. 10, 2024. Technical indicators show the company’s strong performance. The stock is trading above its 200-day SMA (simple moving average) of $65.18, highlighting a continued uptrend. This technical strength, along with sustained momentum, indicates positive market sentiment and investors’ confidence in MDLZ’s financial health and growth prospects.

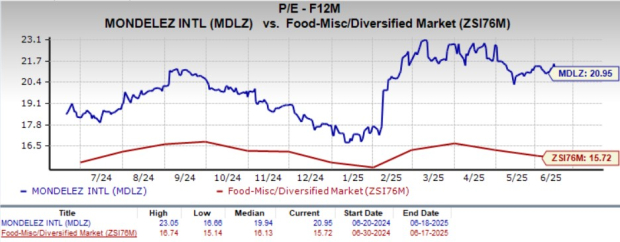

Mondelez currently trades at a forward 12-month P/E ratio of 20.95 compared with the industry average of 15.72 and the sector average of 17.49. This valuation places the stock at a premium relative to peers, reflecting broader market expectations around its business stability and ability to navigate current cost and demand dynamics.

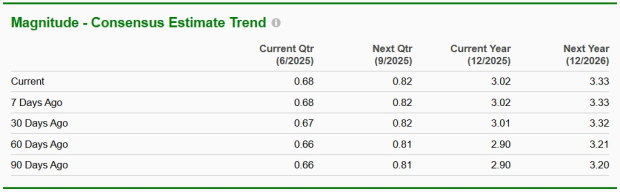

The positive sentiment surrounding MDLZ is reflected in the upward revisions in the Zacks Consensus Estimate for earnings. In the past 30 days, the consensus estimate has moved up by a cent to $3.02 per share for the current fiscal year and to $3.33 for the next fiscal year. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

The Zacks Consensus Estimate for the current and next fiscal year’s sales is pegged at $38.4 billion and $40.1 billion, implying year-over-year growth of 5.3% and 4.5%, respectively.

Nomad Foods NOMD, which manufactures frozen foods, sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

NOMD delivered a trailing four-quarter earnings surprise of 3.2%, on average. The Zacks Consensus Estimate for Nomad Foods’ current financial-year sales and earnings implies growth of 4.6% and 7.3%, respectively, from the year-ago number.

Oatly Group AB OTLY, an oatmilk company, provides a range of plant-based dairy products made from oats. It presently has a Zacks Rank of 2. OTLY delivered a trailing four-quarter earnings surprise of 25.1%, on average.

The consensus estimate for Oatly Group’s current fiscal-year sales and earnings implies growth of 2.3% and 63.8%, respectively, from the year-ago figures.

BRF S.A. BRFS raises, produces and slaughters poultry and pork for the processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank #2. BRFS delivered a trailing four-quarter earnings surprise of 5.4%, on average.

The Zacks Consensus Estimate for BRF's current fiscal-year earnings implies growth of 11.1% from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-16 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jul-09 | |

| Jul-06 | |

| Jul-01 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite