|

|

|

|

|||||

|

|

|

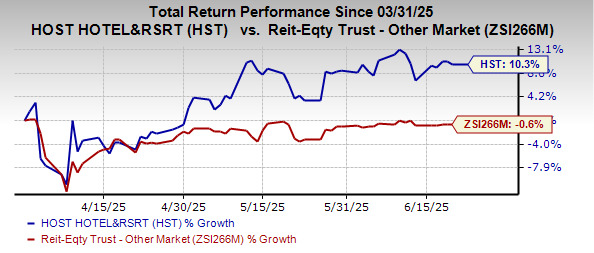

Shares of Host Hotels & Resorts Inc. HST have gained 10.3% in the quarter-to-date period against the industry’s decline of 0.6%.

The Bethesda, MD-based lodging real estate investment trust (REIT) owns a portfolio of luxury and upper-upscale hotels in the top U.S. markets and the Sunbelt region. The recovery in demand for the company’s well-located properties in markets with strong demand drivers has benefited the company lately.

Let us decipher the possible factors behind the surge in the stock price.

This Zacks Rank #3 (Hold) company has a strong Sunbelt exposure and presence in the top 21 U.S. markets. Its properties are advantageously located in central business districts of major cities, thus driving demand. The improvement in group travel demand and business transient demand has aided occupancy and revenue per available room growth over the past few quarters. In 2025, the company expects comparable hotel RevPAR growth between 0.5% and 2.5%.

Host Hotels undertakes strategic capital allocations to improve its portfolio quality and strengthen its position in the United States, where it has a greater scale and competitive advantage. In the first quarter of 2025, the company incurred $146 million in capital expenditure. For 2025, management expects total capital expenditures to be within $580-$670 million.

The company disposes of non-strategic assets with lower growth potential or properties with significant capital expenditure requirements through its capital-recycling program. It has redeployed the proceeds to acquire or invest in premium properties in markets expected to recover faster. Per the company’s May 2025 Investor Presentation, from 2021 through the end of the fourth quarter of 2024, total dispositions amounted to $1.5 billion, which is 17.5 times the EBITDA multiple. Its acquisitions during this period amounted to $3.3 billion, which is 13.3 times the EBITDA multiple. Such efforts highlight its prudent capital-management practices, preserve balance sheet strength and pave the way to capitalize on long-term growth opportunities.

Host Hotels has a healthy balance sheet and has been undertaking steps to fortify its balance sheet. As of March 31, 2025, the company had $2.2 billion in total available liquidity. Moreover, it is the only company with an investment-grade rating among the lodging REITs, having ratings of Baa3/Positive from Moody’s, BBB-/Stable from S&P Global and BBB/Stable from Fitch. This renders access to the debt market at favorable costs. Therefore, Host Hotels has ample financial flexibility for deploying capital for long-term growth opportunities while carrying out redevelopment initiatives.

Solid dividend payouts are a massive enticement for REIT investors, and Host Hotels has remained committed to that. HST has increased its dividend eight times in the last five years and has a 40% payout ratio. Such efforts boost investors’ confidence in the stock. Check out Host Hotels & Resorts’ dividend history here.

With the above-mentioned factors, we believe the rising trend in the stock is expected to continue in the near term.

On the macroeconomic front, recent heightened uncertainty surrounding trade policy and government spending is expected to weigh on the company’s growth through the remainder of 2025. Historically, economic uncertainty has hindered business investment, which is strongly correlated to business transient and group demand.

Moreover, challenges in the supply chain have led to project delays across the United States, and a restrictive lending environment has made it difficult to obtain construction financing for future projects.

Some better-ranked stocks from the broader REIT sector are VICI Properties VICI and Medical Properties Trust MPW, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for VICI’s 2025 FFO per share has moved one cent northward to $2.35 over the past week.

The Zacks Consensus Estimate for MPW’s 2025 FFO per share has moved one cent northward to 57 cents over the past month.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-01 | |

| Feb-28 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite