|

|

|

|

|||||

|

|

|

Zebra Technologies Corporation ZBRA failed to impress investors with its recent operational performance due to increasing cost of sales, high debt levels and forex woes.

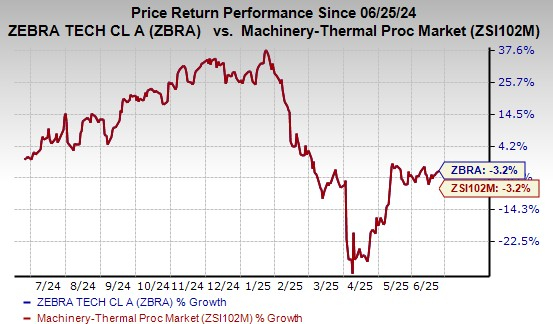

ZBRA currently carries a Zacks Rank #5 (Strong Sell). In the past year, the stock has lost 3.2%, in line with the industry.

Let’s discuss the factors that are likely to continue taking a toll on this company.

Rising Costs: ZBRA has been dealing with the adverse impacts of rising operating costs and expenses. During the first quarter of 2025, the company witnessed an 8.3% year-over-year increase in the cost of sales due to high raw material costs. Also, selling and marketing expenses increased 8.8% year over year. Escalating costs and expenses, if uncontrolled, may negatively impact profitability in the quarters ahead.

High Debt Level: High debt is a major roadblock for the company. ZBRA’s long-term debt in the last five years (2020-2024) witnessed a CAGR of 18.9%. At the end of the first quarter, the company’s long-term debt totaled $2.10 billion compared with $2.09 billion at 2024-end. Considering Zebra Technologies’ high debt level, its cash and cash equivalents of $879 million do not look impressive. Also, interest expenses in the first quarter were $23 million, up 35.3% year over year.

In the second quarter of 2024, ZBRA completed the offering of $500 million senior notes due June 1, 2032, in a private placement. The senior notes have a fixed interest rate of 6.5%, payable semi-annually. Although the current notes offering will help pay down a share of its term loan, we believe it will also add to Zebra Technologies’ existing debt balance.

Forex Woes: The company operates across diverse regions (North America, EMEA, the Asia-Pacific and Latin America), exposing it to certain political, environmental and geopolitical issues. The ongoing conflicts between Russia & Ukraine and Israel & Iran, and changes in China-Taiwan and U.S.-China relations may harm its business and operational results in the long run. Moreover, the company has considerable exposure to overseas markets. This brings social and environmental risks as well as forex woes. A stronger U.S. dollar might weigh on the company’s overseas business performance.

Some better-ranked companies are discussed below:

Life360, Inc. LIF currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

LIF delivered a trailing four-quarter average earnings surprise of 425%. In the past 60 days, the Zacks Consensus Estimate for Life360’s 2025 earnings has increased 20%.

Alarm.com Holdings, Inc. ALRM presently carries a Zacks Rank #2 (Buy). It has a trailing four-quarter average earnings surprise of 15.7%.

The Zacks Consensus Estimate for ALRM’s 2025 earnings has increased 0.9% in the past 60 days.

Broadwind, Inc. BWEN presently carries a Zacks Rank of 2. The company delivered a trailing four-quarter average earnings surprise of 61.1%.

In the past 60 days, the consensus estimate for BWEN’s 2025 earnings has increased 14.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-23 | |

| Jul-23 | |

| Jul-21 | |

| Jul-16 | |

| Jul-13 | |

| Jul-10 | |

| Jul-07 | |

| Jun-22 | |

| Jun-18 | |

| Jun-18 | |

| Jun-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite