|

|

|

|

|||||

|

|

|

AbbVie ABBV stock has risen 8.0% in six months, adding more than $24 billion to its market value.

AbbVie has successfully navigated the loss of exclusivity (“LOE”) of its blockbuster drug, Humira, by launching two other successful new immunology medicines, Skyrizi and Rinvoq, which are performing extremely well, bolstered by approvals in new indications and are expected to support top-line growth in the next few years. AbbVie has several early/mid-stage candidates that have the potential to drive long-term growth.

AbbVie, however, faces its share of headwinds, like Humira biosimilar erosion, increasing competitive pressure on Imbruvica and slowing sales of its aesthetics franchise.

Let’s understand the company’s strengths and weaknesses to better analyze how to play ABBV stock amid the market value growth.

AbbVie lost patent protection for Humira in the United States in January 2023 and in the EU in 2018. Humira's sales are declining due to the LOE and biosimilar erosion. However, with approvals for many new indications, sales of Skyrizi and Rinvoq have successfully replaced Humira, which once generated more than 50% of its total revenues.

Skyrizi and Rinvoq generated combined sales of $5.1 billion in the first quarter of 2025, reflecting growth of more than 65%. The drugs are seeing strong performance across all approved indications, especially in the popular inflammatory bowel disease (IBD) space, which includes two conditions — ulcerative colitis (UC) and Crohn’s disease (CD). Importantly, Skyrizi and Rinvoq have demonstrated compelling head-to-head data against several novel therapies in clinical studies, which have given them a competitive advantage.

AbbVie expects combined sales of Skyrizi and Rinvoq to be around $24.7 billion in 2025 and more than $31 billion by 2027. Strong immunology market growth, market share gains and momentum from new indications, such as the recent launch of Skyrizi in UC, as well as the potential for five new indications for Rinvoq over the next few years, are expected to drive these drugs’ growth.

AbbVie has several early/mid-stage pipeline candidates with blockbuster potential. The company expects several regulatory submissions, approvals and key data readouts in the next 12 months.

ABBV has an exciting and diverse pipeline of promising new therapies in blood cancers and solid tumors, like ABBV-383, a BCMA CD3 bispecific (relapsed/refractory multiple myeloma) and Temab-A (metastatic colorectal cancer). Emrelis (previously Teliso-V), a promising antibody drug conjugate or ADC, was approved in the United States for previously treated non-squamous non-small cell lung cancer with high c-Met expression in May 2025. In other areas, some key pipeline drugs are lutikizumab for immunology indications and tavapadon for early Parkinson's disease. AbbVie expects to file a new drug application for tavapadon this year.

The company has been on an acquisition spree in the past couple of years, which is strengthening its pipeline. It has signed several M&A deals in the immunology space, its core area, while also inking some early-stage deals in oncology and neuroscience. It has signed more than 20 early-stage deals since the beginning of 2024, including promising technologies and innovative mechanisms that can elevate the standard of care in immunology, oncology and neuroscience. In early 2025, AbbVie bought rights to develop GUB014295 (ABBV-295), a long-acting amylin analog for the treatment of obesity, from Denmark’s Gubra. The deal marked AbbVie’s entry into the obesity space, dominated by Eli Lilly LLY and Novo Nordisk NVO. AbbVie plans to invest further in obesity.

Sales of AbbVie’s blockbuster drug Humira are declining due to biosimilar erosion. Humira volume is rapidly eroding compared to other novel mechanisms (including Skyrizi and Rinvoq). Humira sales declined by almost 50% in the first quarter of 2025, primarily due to faster erosion of its share as a result of biosimilar competition, as well as further molecule compression in the United States.

AbbVie is witnessing declining sales of Juvederm fillers in the United States and China due to challenging market conditions. The slowing growth of the U.S. facial injectables market and persistent economic headwinds, which are affecting consumer spending in China, are hurting AbbVie’s aesthetics portfolio sales, which declined 10.2% in the first quarter of 2025.

AbbVie’s stock has gained 7.1% so far this year against a decrease of 0.7% for the industry. The stock has also outperformed the industry and the S&P 500 index, as seen in the chart below.

From a valuation standpoint, AbbVie is not very cheap. Going by the price/earnings ratio, the company’s shares currently trade at 14.21 forward earnings, just slightly lower than 14.87 for the industry. The stock is cheaper than some other large drugmakers like Eli Lilly and Novo Nordisk, but is priced much higher than most other large drugmakers. The stock is also trading above its five-year mean of 12.44.

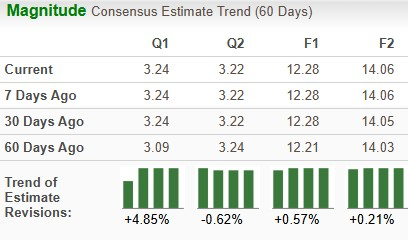

The Zacks Consensus Estimate for 2025 earnings has risen from $12.21 per share to $12.28, while that for 2026 has increased from $14.03 to $14.06 per share over the past 30 days.

Though AbbVie faces its share of near-term headwinds, the company has faced its biggest challenge — Humira’s patent cliff — quite well and looks well-positioned for continued strong growth in the years ahead. AbbVie expects to return to robust revenue growth in 2025, which is just the second year following the U.S. Humira LOE, driven by its ex-Humira platform. AbbVie’s ex-Humira drugs rose delivered robust sales growth of more than 21% (on a reported basis) in the first quarter of 2025.

Boosted by its new product launches, AbbVie expects to return to robust mid-single-digit revenue growth in 2025 with a high single-digit CAGR through 2029, as it has no significant LOE event for the rest of this decade. A substantial portion of this growth is expected to be driven by the robust performance of Skyrizi and Rinvoq.

Rising estimates for AbbVie, its solid pipeline and the prospect of growth in 2025 sales and profits are good enough reasons to stay invested in this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 31 min | |

| 44 min | |

| 45 min | |

| 51 min | |

| 54 min | |

| 57 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours |

AbbVie announces $380m investment in North Chicago API facilities

ABBV

Pharmaceutical Business Review

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite