|

|

|

|

|||||

|

|

|

Alibaba’s BABA e-commerce business continues to be the company’s biggest strength. Its main platforms, Taobao and Tmall, help drive strong customer management revenues, which grew 12% year over year in the fourth quarter of fiscal 2025, driven by the improvement of take rates. Better tools and shopping incentives have improved user activity and order frequency, helping the company recover its core business despite a tough macro environment.

Alibaba sees e-commerce as key to future growth, both in China and globally. With stronger monetization tools and better AI-driven search and recommendations, the company plans to grow consumption quality rather than just volume. Its global platforms, like AliExpress and Lazada, are also expected to benefit from rising cross-border demand.

Alibaba is combining Ele.me, its food delivery platform, and Fliggy, its travel services platform, with its core e-commerce business, realigning resources around its main revenue engine and building a stronger delivery network. In April, the company also launched a new rapid delivery feature on Taobao, which the company called a strategic upgrade, as it helps it evolve from an e-commerce platform into a broader consumer-focused platform.

In the fiscal fourth quarter, Taobao and Tmall Group earned RMB 93.2 billion ($12.9 billion) in revenues, up 4% year over year, and made up 47% of total company revenues. International commerce, including AliExpress and Lazada, earned RMB 27.4 billion ($3.8 billion), up 45% year over year, with AliExpress alone growing 22%. Together, domestic and global e-commerce remain Alibaba’s strongest growth drivers.

As Alibaba sharpens its focus on e-commerce, it faces growing competition from domestic rivals JD.com JD and PDD Holdings Inc. Sponsored ADR PDD, both of which are rapidly expanding in China’s digital retail market.

JD.com is driving growth through strong category execution and ecosystem integration. Its RMB 200 billion “export to domestic” program and food delivery momentum are boosting engagement. In the first quarter of 2025, JD Retail revenues grew 16.3% year over year.

PDD Holdings continues to scale its group buying model while expanding merchant support. In the first quarter of 2025, online marketing services revenues rose 15% year over year, driven by PDD Holdings’ enhanced tools to improve reach and performance.

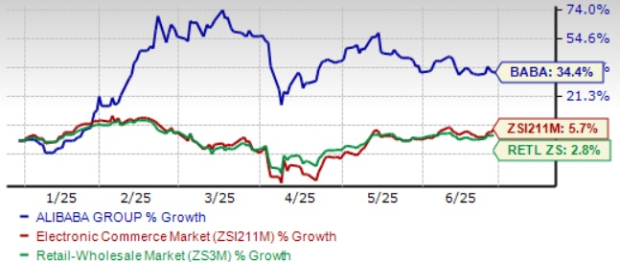

BABA shares have gained 34.4% in the year-to-date (YTD) period, outperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 5.7% and 2.8%, respectively.

From a valuation standpoint, BABA stock is currently trading at a forward 12-month Price/Earnings ratio of 10.39X compared with the industry’s 24.70X. BABA has a Value Score of B.

The Zacks Consensus Estimate for first-quarter fiscal 2026 earnings is pegged at $2.48 per share, which has remained steady over the past 30 days, indicating 9.73% year-over-year growth.

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

The consensus mark for fiscal 2026 earnings is pegged at $10.47 per share, which has remained steady over the past 30 days. The estimate indicates 16.2% year-over-year growth.

Alibaba currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite