|

|

|

|

|||||

|

|

|

We continue to see headlines dominated by the beloved AI trade, with many companies in the space seeing big-time share gains thanks to the overwhelming positivity.

The theme is undoubtedly here to stay for years, with many believing we haven’t even entered the early innings yet.

And at the forefront has been NVIDIA NVDA, which has seen unprecedented growth over recent years thanks to the frenzy. But a lingering question remains following the stock’s immense run over the last several years – is the stock too expensive to buy now?

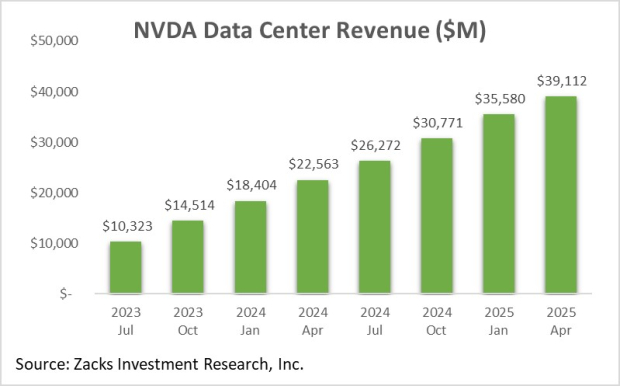

As mentioned above, unrelenting demand for its Data Center products has provided NVIDIA with unprecedented growth over recent years. The AI poster child continued to fire on all cylinders throughout its latest release, with Data Center sales of $39.1 billion up a staggering 73% from the $22.5 billion print in the same period last year.

Below is a chart illustrating NVIDIA’s Data Center sales on a quarterly basis.

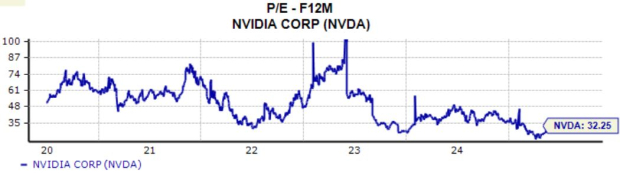

The stock clearly reflects one of the strongest straightforward AI plays out there, with the valuation picture also not rich. Shares currently trade at a 30.1X forward 12-month earnings multiple, a fraction of the 106.3X five-year highs and well beneath the 50.0X five-year median.

The current PEG ratio works out to a fair 1.1X, again well beneath five-year highs and the five-year median. Keep in mind that shares traded well above current valuation levels in 2020 and 2021, a time when the AI theme had yet to emerge fully and when the company was primarily known for its gaming GPUs.

NVIDIA’s recent deal with the Kingdom of Saudi Arabia (KSA) is further proof that everybody wants their hands on its GPUs. More specifically, HUMAIN, a subsidiary of Saudi Arabia’s Public Investment Fund focused on AI, announced in May a major investment to build AI factories in KSA with a projected capacity of up to 500 megawatts powered by several hundred thousand of NVIDIA’s most advanced GPUs over the next five years.

Further adding to the snowballing of deals NVDA has enjoyed, the company also recently unveiled a partnership with Novo Nordisk NVO to create customized AI models and agents that Novo Nordisk can utilize for early research and clinical development, as well as to apply advanced simulation and physical AI technologies.

Bottom Line

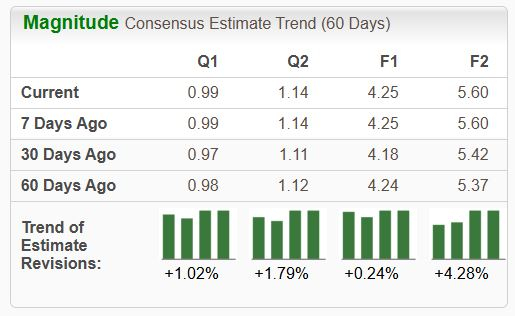

With NVIDIA’s massive run over recent years, many have felt that the stock has become too expensive. But the reality is that that shares aren’t rich at all concerning the valuation picture, with current multiples comparing favorably to historical levels. Red-hot growth has kept the valuation picture in check, with current consensus expectations alluding to 42% EPS growth in its current fiscal year on 51% higher sales.

The lofty growth expectations fully reflect the immense demand in the space, with the trend set to continue for years as more continue to get their hands on NVIDIA’s GPUs. In addition, the company’s EPS outlook remains positive across the board, with analysts continuing to positively revise their expectations over recent months.

NVIDIA NVDA remains the go-to stock for AI exposure given its sheer size and unmatched execution, with the latter being a significant reason behind its remarkable story. While many wait to buy a potential dip, the reality remains that it’d take a massively negative development to slow the stock down.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 30 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 8 hours | |

| 11 hours | |

| 11 hours | |

| Apr-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite