|

|

|

|

|||||

|

|

|

Since December 2024, Telephone and Data Systems has been in a holding pattern, posting a small return of 0.9% while floating around $34.31.

Is now the time to buy Telephone and Data Systems, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

We're sitting this one out for now. Here are three reasons why you should be careful with TDS and a stock we'd rather own.

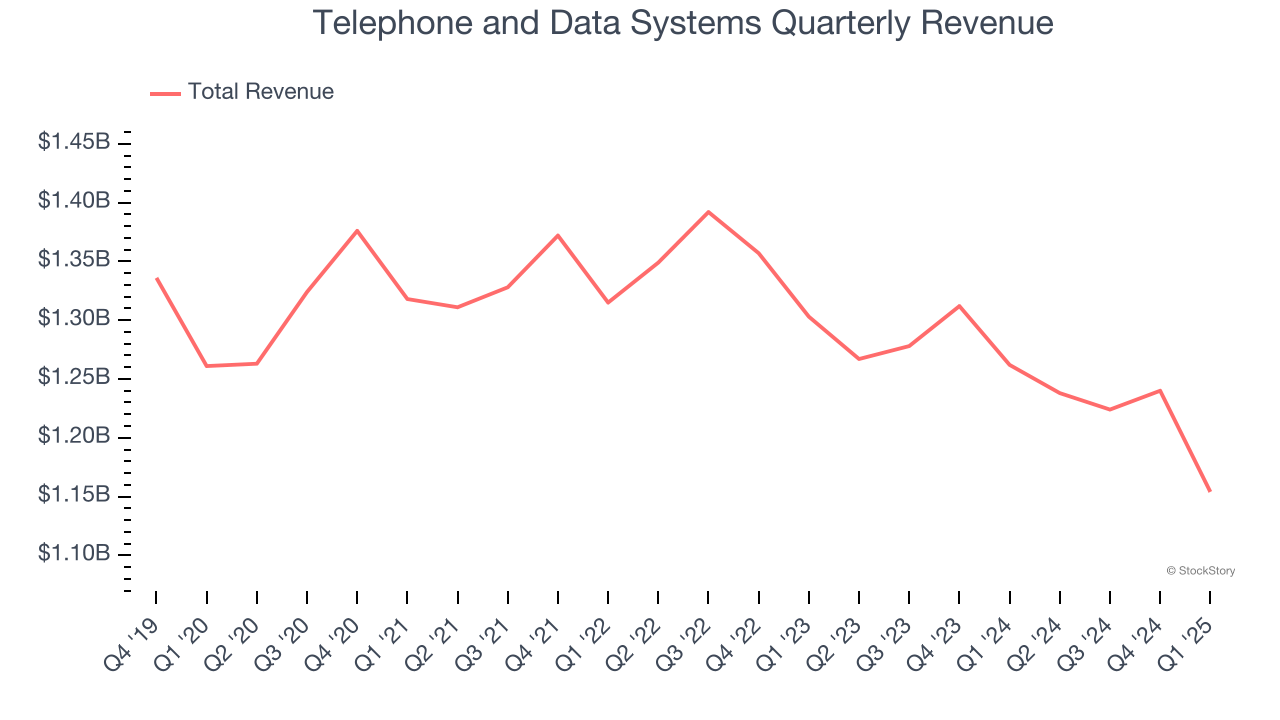

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Telephone and Data Systems’s demand was weak and its revenue declined by 1.6% per year. This was below our standards and is a sign of poor business quality.

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Telephone and Data Systems, its EPS declined by 24% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Telephone and Data Systems’s $5.10 billion of debt exceeds the $348 million of cash on its balance sheet. Furthermore, its 26× net-debt-to-EBITDA ratio (based on its EBITDA of $180 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Telephone and Data Systems could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Telephone and Data Systems can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Telephone and Data Systems falls short of our quality standards. That said, the stock currently trades at 3× forward EV-to-EBITDA (or $34.31 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-31 | |

| Jun-01 | |

| May-21 | |

| May-11 | |

| May-08 | |

| May-08 | |

| May-08 | |

| May-08 | |

| May-01 | |

| Apr-27 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite