|

|

|

|

|||||

|

|

|

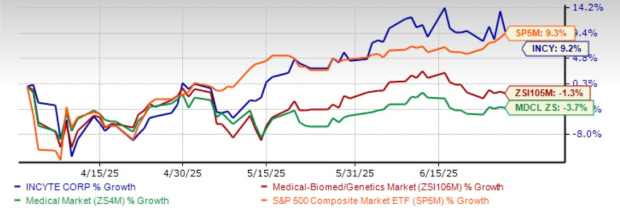

Incyte INCY has put up a good performance in the past three months. Shares of the company have gained 9.2% against the industry’s decline of 1.3%. The stock has also outperformed the sector in the said timeframe.

The outperformance can be attributed to positive pipeline and regulatory updates. Lead drug Jakafi (ruxolitinib) also maintains momentum.

Let us take a look at what’s happening with Incyte.

Last month, the FDA approved Monjuvi (tafasitamab-cxix) for a new cancer indication.

Monjuvi, in combination with Rituxan (rituximab) and Revlimid (lenalidomide), was approved for the treatment of adult patients with relapsed or refractory follicular lymphoma, a type of slow-growing blood cancer.

The drug is already approved, in combination with Revlimid, for the treatment of adult patients with relapsed or refractory diffuse large B-cell lymphoma who are not eligible for autologous stem cell transplant.

Incyte gained worldwide exclusive global rights for tafasitamab from MorphoSys AG in February 2024. Tafasitamab is marketed as Monjuvi in the United States and as Minjuvi in the ex-U.S. markets.

The label expansion of the drug should boost sales of the drug.

INCY’s announcement of a new global collaboration with Qiagen QGEN benefited the stock.

The collaboration is aimed at developing a novel diagnostic panel to support INCY’s pipeline of investigational treatments for myeloproliferative neoplasms (MPNs), a group of rare blood cancers.

Per the agreement with Incyte, QIAGEN will develop a multimodal panel utilizing next-generation sequencing (NGS) technology to detect clinically relevant gene alterations in hematological malignancies.

Further, the panel will be validated on the Illumina NextSeq 550Dx platform for use with whole blood samples. QIAGEN will also assist with regulatory submissions and market access efforts in the United States, the EU and certain Asia-Pacific regions.

In May 2025, the FDA approved a label expansion of oncology drug Zynyz (retifanlimab-dlwr), a PD-1 inhibitor. The regulatory body has now approved Zynyz in combination with platinum-based chemotherapy (carboplatin and paclitaxel) for the first-line treatment of adult patients with locally recurrent or metastatic squamous cell carcinoma of the anal canal (SCAC).

Simultaneously, the FDA approved Zynyz as a monotherapy for treating locally recurrent or metastatic SCAC in adult patients whose disease progressed or who are intolerant to platinum-based chemotherapy.

Zynyz is also indicated in the United States for the treatment of adult patients with metastatic or recurrent locally advanced merkel cell carcinoma.

Incyte’s efforts to develop new drugs diversify its portfolio and add an incremental stream of revenues.

Encouraging uptake of new drugs like Pemazyre, Monjuvi and Tabrecta is contributing to its top-line growth.

The label expansion of these drugs is expected to boost sales.

Incyte’s lead drug, Jakafi, is a JAK1/JAK2 inhibitor approved for the treatment of polycythemia vera (PV) in adults who have had an inadequate response to or are intolerant of hydroxyurea; intermediate or high-risk myelofibrosis (MF), including primary MF, post-polycythemia vera MF and post-essential thrombocythemia MF in adults; steroid-refractory acute graft-versus-host disease (GVHD) in adult and pediatric patients 12 years and older; and chronic GVHD after failure of one or two lines of systemic therapy in adult and pediatric patients aged 12 years and older.

Sales in all indications continue to be strong and should maintain momentum going forward.

Jakafi is marketed by Incyte in the United States and by Novartis NVS as Jakavi in ex-U.S. markets. Incyte earns royalties from NVS on sales outside the country.

The FDA’s approval of the cream formulation of ruxolitinib for the treatment of mild to moderate atopic dermatitis (AD), under the brand name Opzelura, has been a significant boost for the company. The drug has also been approved for the topical treatment of non-segmental vitiligo in adult and pediatric patients aged 12 years and above. The approval makes Opzelura the first and only topical formulation of a JAK inhibitor approved in the United States. The uptake of Opzelura has been strong.

While the uptake of recently approved drugs has been good and a potential approval of the additional drugs should diversify its portfolio, INCY is heavily dependent on Jakafi for its top-line growth.

Moreover, competition has increased for some of Jakafi’s approved indications. The FDA’s approval of GSK plc’s GSK Ojjaara for the treatment of intermediate or high-risk MF, including primary MF or secondary MF (post-polycythemia vera and post-essential thrombocythaemia), in adults with anemia, poses a concern.

Jakafi is also expected to lose patent protection in a few years. The FDA recently extended the review period for the supplemental new drug application (sNDA) for ruxolitinib cream seeking approval for the treatment of children 2-11 years old with mild to moderate AD.

The target action date has been extended by three months to Sept. 19, 2025, to provide the FDA with the time to review additional chemistry, manufacturing and controls data on the 0.75% strength submitted by Incyte in response to a recent information request by the regulatory body.

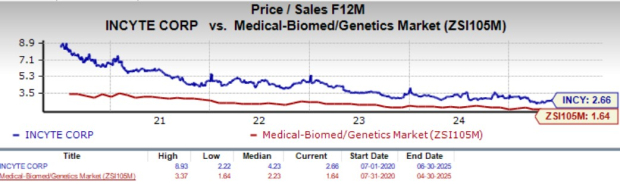

Going by the price/sales ratio, INCY’s shares currently trade at 2.66x forward sales, lower than its mean of 4.23x but higher than 1.64x for the biotech industry.

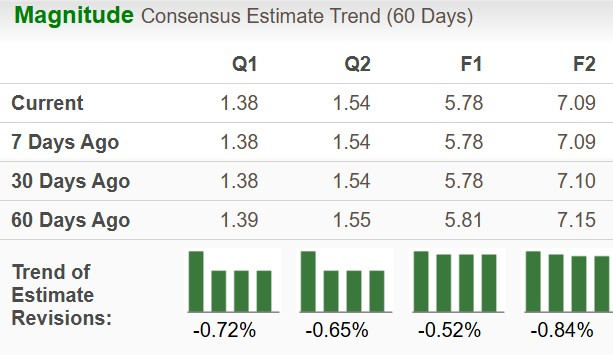

The Zacks Consensus Estimate for 2025 earnings per share (EPS) has moved down to $5.78 from $5.81 over the past 60 days. During the same timeframe, the EPS estimate for 2026 has moved south to $7.09.

Large biotech companies are generally considered safe havens for investors interested in this sector. Incyte’s recent rally has been positive, and potential label expansion of existing drugs and the launch of new drugs should generate incremental revenues and drive share price gains.

However, generic competition for Jakafi is a major headwind as it accounts for more than 65% of total revenues. Incyte has recently appointed Bill Meury as its president and chief executive officer (CEO).

With a new CEO at the helm, it remains to be seen which direction the business takes and how the pipeline evolves over time. Hence, we advise a wait-and-watch stance for prospective investors as of now.

INCY currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Slate Medicines raises $130m in funds to progress anti-PACAP treatments

NVS

Pharmaceutical Technology

|

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite