|

|

|

|

|||||

|

|

|

Capital One Financial Corporation COF shares touched a 52-week high of $215.62 in yesterday’s trading session. This comes after the firm passed the Federal Reserve’s 2025 stress test on Friday, displaying sufficient capital on hand to absorb hundreds of billions of dollars in losses.

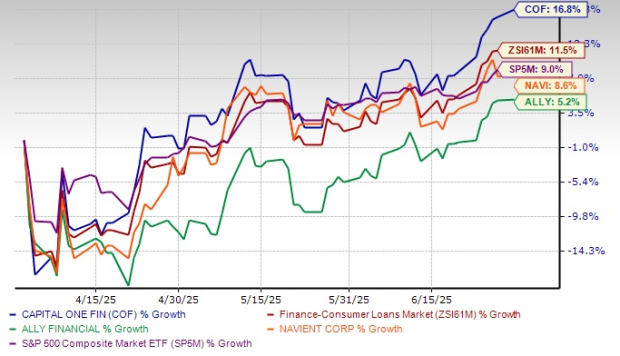

Over the past three months, the COF stock has gained 16.8%, outperforming the industry’s rise of 11.5% and the S&P 500 Index’s 9% growth. Moreover, the stock has performed better than its peers, Ally Financial ALLY and Navient Corporation NAVI. The ALLY stock has moved up 5.2%, whereas shares of Navient have rallied 8.6% in the same time frame.

Does the COF stock have more upside left despite touching its 52-week high? Let us find out.

Robust Inorganic Expansion Strategy: Over the years, Capital One's revenues have been driven by opportunistic acquisitions. Last month, COF acquired Discover Financial in an all-stock transaction valued at $35.3 billion, unlocking substantial value for shareholders. In 2023, it acquired Velocity Black, bolstering the delivery of exceptional consumer experiences attributable to its innovative technology.

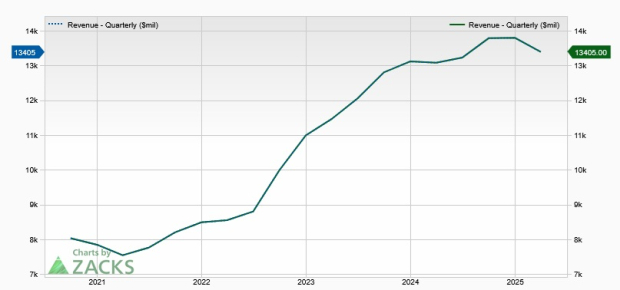

Although COF’s total revenues declined marginally in 2020, the metric witnessed a five-year (2019-2024) compound annual growth rate (CAGR) of 6.5%, with the upward momentum continuing in the first quarter of 2025.

Solid Card Business: The performance of Capital One’s Credit Card segment has been impressive. The company’s revenue prospects look encouraging, given its solid credit card and online banking businesses, and decent loan demand. While in May 2024, COF ended its card partnership with Walmart, its 2017 acquisition of Cabela Incorporated’s credit card operations bodes well.

In the first quarter of 2025, the Domestic Credit Card division, which accounted for 94.9% of credit card net revenues, reflected an improvement in loans held for investment. Strong growth opportunities in card loans and purchase volumes will likely continue despite an intensely competitive environment.

Increasing Net Interest Margin: The company’s net interest margin (NIM) has been rising, driven by the high-rate regime. In 2024, NIM expanded to 6.88% from the 2023 level of 6.63%. The uptrend continued in the first quarter of 2025.

COF’s efforts to scale its business, along with relatively high rates and steady demand for credit card loans, will likely keep benefiting NIM growth.

Solid Balance Sheet Position: As of March 31, 2025, Capital One had total debt (securitized debt obligations plus other debt) worth $41.8 billion, and the total cash and cash equivalents balance was $48.6 billion, which makes it well-positioned in terms of its liquidity profile and earnings strength.

Moreover, after slashing the quarterly dividend by 75% in 2020 based on the Federal Reserve’s requirements, Capital One restored the same to 40 cents per share in the first quarter of 2021, which was then hiked 50% to 60 cents in July 2021.

COF also has a share repurchase plan in place. In January 2022, it authorized a repurchase program of up to $5 billion in shares, while in April 2022, it announced an additional $5 billion worth of buybacks (effective from the third quarter of 2022). As of March 31, 2025, $3.88 billion worth of repurchase authorization remained.

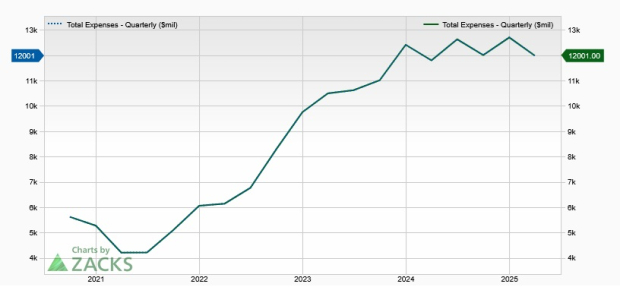

Rising Expense Base: COF has been witnessing a persistent rise in expenses. Though expenses declined in 2020, the metric saw a CAGR of 6.8% over the last five years (ended 2024). The increase was mainly because of a rise in marketing costs (saw a CAGR of 14.9% in the same time frame) and inflationary pressure. The uptrend in costs continued in the first quarter of 2025.

Given the company’s investments in technology and infrastructure, as well as inorganic expansion efforts, expenses are anticipated to remain elevated. The rise in the cost of modern tech talent and continued investments in growth opportunities will strain annual operating efficiency in the near term.

Deteriorating Asset Quality: Capital One’s provision for credit losses and net charge-offs (NCOs) have increased amid the tough macroeconomic backdrop. Though the company recorded a provision benefit in 2021, provision for credit losses witnessed a CAGR of 13.4% over the last five years (2019-2024). Likewise, NCOs recorded a CAGR of 11.4% in the same time frame.

While provisions declined in the first quarter of 2025, the company’s credit quality is expected to remain under pressure due to the tough macroeconomic outlook and persistent inflation.

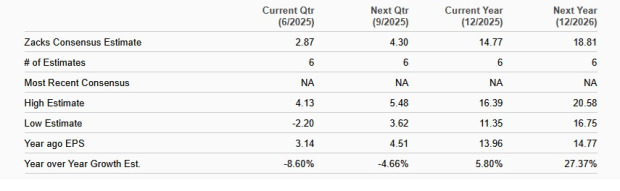

Analysts are optimistic regarding Capital One’s earnings growth potential. Over the past 30 days, the Zacks Consensus Estimate for the company’s 2025 and 2026 earnings has been revised 16.9% and 4.7% upward, respectively. The estimated figures reflect respective year-over-year growth rates of 5.8% and 27.4%.

In a relatively high interest-rate environment, Capital One is well-positioned for top-line growth, supported by strength in its credit card business. Moreover, a robust balance sheet position and strategic acquisition efforts will further aid growth.

However, increasing expenses because of the company’s investments in technology and infrastructure will likely hurt the bottom line to an extent. Also, poor asset quality might hamper growth.

In terms of its valuation, the COF stock appears expensive compared with the industry. It has a P/E (F1) ratio of 14.41, which is above the industry’s 11.51.

Thus, while analysts seem optimistic regarding COF’s earnings growth prospects, investors should not rush to buy the stock now, given that it is trading at a premium. Instead, they should keep this stock on their radars and wait for an attractive entry point. Those who already own the COF stock in their portfolios can hold on to it because it is less likely to disappoint over the long term.

Currently, COF carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-25 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite