|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Applied Materials AMAT and KLA Corporation KLAC are both key players in the semiconductor equipment market, serving distinct roles in the chip manufacturing process. While AMAT develops equipment for deposition, etching, and inspection across a wide range of semiconductor nodes, KLAC specializes in process control and metrology systems.

With the artificial intelligence (AI) boom to continue driving growth for the semiconductor industry, the question remains: Which stock is a better investment pick today? Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which offers a more compelling investment case.

Applied Materials is experiencing strong traction in its Sym3 Magnum etch system, Cold Field Emission eBeam technology, gate-all-around, backside power delivery, and 3D DRAM technology nodes crucial for developing high-performance processing and memory chips used for AI and HPC workloads.

AMAT’s Sym3 Magnum etch system has generated more than $1.2 billion in revenues since its launch in February 2024. Furthermore, in the second quarter of fiscal 2025, the management projected AMAT's revenues from DRAM customers to grow more than 40% in fiscal 2025. Earlier, AMAT reported that its revenues from advanced semiconductor nodes crossed $2.5 billion in 2024 and it expected the figure to double in fiscal 2025 as customers’ adoption of its GAA and backside power delivery solutions grows.

However, Applied Materials is grappling with the trade restrictions imposed by the U.S. government on its semiconductor equipment sales to China. AMAT’s revenues from the 200mm equipment sales have been hampered by the U.S. government’s recent stance toward China. The company is also facing restrictions in servicing some Chinese clients, causing an overall decline in Applied Global Services’ revenues.

AMAT’s weakness in the Chinese market has further been exacerbated by the inflow of newer players like Scaria, which has started providing products that overlap with Applied Materials. A cyclical slowdown in AMAT’s IoT, Communications, Automotive, Power, and Sensors (ICAPS) segment has also stagnated the overall performance.

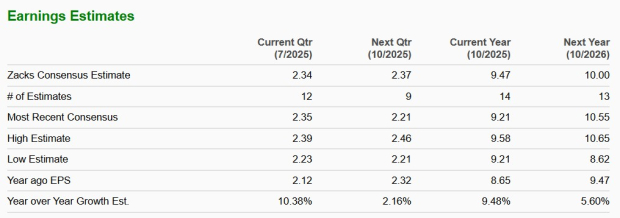

The Zacks Consensus Estimate for fiscal 2025 signals single-digit growth in both bottom and top lines. The consensus mark for revenues and EPS indicates year-over-year growth of 6% and 9.5%, respectively.

The rising demand for AI chips is also ramping up the demand for advanced process control and process-enabling solutions provided by KLA Corporation. KLAC’s advanced packaging solutions are also experiencing robust traction on the back of AI and high performance computing.

The company, in its third-quarter fiscal 2025 earnings, projected that its advanced packaging business will touch $850 million in 2025 from $500 million in 2024. Furthermore, as HBM production requires high-reliability, high-precision process control to meet performance requirements and reduce redundancy, KLAC’s advanced process control solutions will continue to experience robust traction in this space.

Per a research by Verified Market Reports, the semiconductor process control market is expected to witness a CAGR of 7.2% from 2026 to 2033. KLA Corporation held a significant market share of more than 56% in 2024, driven by strong demand for optical patterned wafer inspection and expansion in Advanced Wafer Level Packaging.

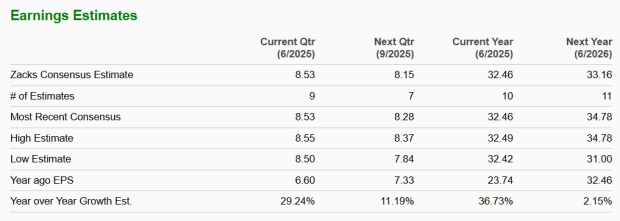

The Zacks Consensus Estimate for fiscal 2025 signals single-digit growth in both bottom and top lines. The consensus mark for revenues and EPS indicates year-over-year growth of 22.7% and 36.7%, respectively.

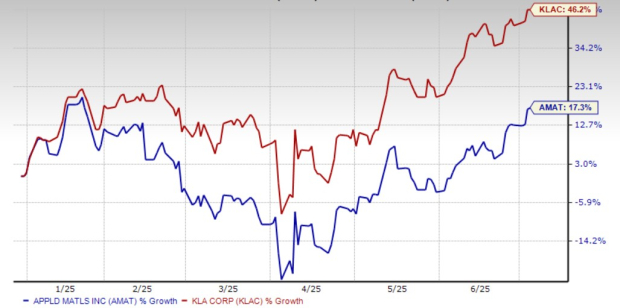

Year to date, shares of Applied Materials and KLA Corporation have gained 17.3% and 46.2%, respectively.

Both AMAT and KLAC are trading at forward 12-month price-to-sales multiples of 5.10X and 10.11X, above their one-year median of 4.86X and 10.11X, respectively, over the past year.

Both AMAT and KLAC are essential players in the semiconductor equipment space, but KLA Corporation has the advantage of possessing a stronger market share in its specialized domain. While KLAC carries a Zacks Rank #2 (Buy), AMAT has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 9 hours | |

| 12 hours | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite