|

|

|

|

|||||

|

|

|

Sterling Infrastructure, Inc.’s STRL shares are currently trading at a forward 12-month price-to-earnings (P/E) ratio of 25.29, a roughly 19.5% premium to the Zacks Engineering - R and D Services industry average of 21.16, and higher than its five-year median.

The STRL stock appears overvalued, especially when compared with other peer companies such as AECOM ACM, Fluor Corporation FLR and KBR, Inc. KBR, all of which are trading at lower values than Sterling. AECOM, Fluor and KBR have a forward P/E of 20.5, 19.44 and 11.74, respectively.

Is STRL’s premium valuation justified at the present moment? Let us have a look at its share price performance, earnings estimates movement and fundamental factors that can impact its valuation.

So far this year, shares of Sterling Infrastructure have gained 35.8% compared with the industry’s and the S&P 500’s increases of 8.1% and 5.4%, respectively. The STRL stock has also outperformed the broader Construction sector's 2.3% rise during the same period.

Stable E-Infrastructure Demand: This Texas-based e-infrastructure, building and transportation solutions provider is capitalizing on rising data center demand, fueled by Artificial Intelligence and digital transformation trends. The company is expanding its E-Infrastructure platform through disciplined bidding, strong execution and consistent activity in key transportation markets.

In the first quarter of 2025, data center-related revenues grew nearly 60% year over year, driven by accelerated customer timelines and Sterling’s role in large-scale builds. The segment also benefited from growth in e-commerce and smaller industrial developments, creating a more balanced mix and reducing reliance on a single trend.

Sterling Infrastructure expects mid-to-high teens revenue growth for the segment in 2025, with margins in the mid-20%. The company’s visibility into multi-year projects, supported by structural trends in AI, e-commerce and onshoring, suggests that it is well-positioned to benefit from continued investment in digital infrastructure.

Strong Backlog: STRL maintains a solid backlog, providing clear visibility into upcoming work and supporting steady earnings growth prospects over the next few years.

At the end of the first quarter of 2025, the total backlog stood at $2.1 billion, up 17% year over year on a pro-forma basis, driven by a 27% rise in the E-Infrastructure Solutions backlog, which reached $1.2 billion. In addition, the company reached the high end of its $750-million target for future-phase opportunities, bringing total visibility close to $2 billion in E-Infrastructure projects.

With E-Infrastructure projects gaining increasing strategic focus, sustained data center demand is expected to remain a key driver of margin strength going forward. The company’s gross margin of the backlog stood at 17.7% at the end of the first quarter of 2025, up 100 basis points from 16.7% at the end of 2024, positioning it well to capitalize on robust demand trends and execute its expanding pipeline of high-margin work in the years ahead.

Transportation Infrastructure Poised for Growth: Sterling Infrastructure’s Transportation Solutions segment remains on track for profitable growth, supported by a strong backlog and steady bid activity as the company moves through the second half of the Infrastructure Investment and Jobs Act (IIJA) funding cycle. The Transportation Solutions segment’s backlog stood at $861 million at the end of the first quarter of 2025, up 11% year over year, providing healthy revenue visibility.

Sterling Infrastructure expects Transportation Solutions to deliver mid-single-digit revenue growth and mid-teen operating profit growth in 2025. The company continues to see strong demand in its core Rocky Mountain and Arizona markets, with robust bid pipelines and a disciplined focus on complex infrastructure work that delivers better returns.

Ongoing federal investment under the IIJA and progress on a potential follow-on infrastructure bill strengthen the company’s long-term prospects.

Strategic Expansion Drive: Sterling Infrastructure continues to strengthen its E-Infrastructure platform through acquisitions to expand its reach in high-growth, mission-critical markets like data centers and semiconductors. This inorganic growth approach aligns with Sterling’s focus on scaling capabilities across the full project lifecycle and unlocking revenue streams through organic expansion and targeted M&A.

On June 17, 2025, Sterling Infrastructure signed a definitive agreement to acquire CEC Facilities Group, LLC, a specialty electrical and mechanical contractor based in Irving, TX, for $505 million. The deal, expected to close in the third quarter, will add CEC to Sterling’s E-Infrastructure Solutions segment, enhancing its presence in Texas and other key regions.

CEC’s strong backlog, end-to-end service offerings, and focus on complex electrical systems for fast-growing sectors are expected to create cross-selling opportunities, supporting Sterling’s return on invested capital (ROIC) and long-term growth strategy. (Read more: Sterling Expands E-Infrastructure Platform With CEC Buyout, Stock Up)

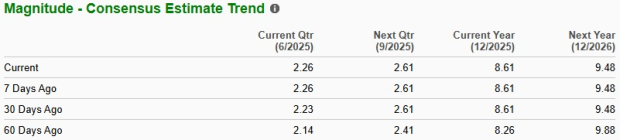

Wall Street analysts remain optimistic about STRL’s earnings potential. Over the past 60 days, earnings estimates for 2025 have been revised upward to $8.61 per share from $8.26. The estimate indicates growth of 41.2% from that reported a year ago. Conversely, AECOM, Flour and KBR’s earnings in the current year are likely to witness increases of 13.9%, 8.2 % and 15%, respectively, year over year.

Despite its high valuation, Sterling Infrastructure’s fundamentals continue to justify investor confidence. The company’s strong E-Infrastructure segment, supported by structural demand for data centers, AI and onshoring, remains a key earnings driver with healthy margins and multi-year project visibility.

Its Transportation Infrastructure business is also well-positioned for steady growth, underpinned by robust federal funding and disciplined project selection. Meanwhile, Sterling’s latest strategic acquisition reinforces its commitment to expanding in mission-critical sectors through targeted M&A.

With rising earnings estimates and solid backlog trends, this Zacks Rank #2 (Buy) company still has the potential to deliver profitable growth that supports its premium valuation.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-15 |

Sterling, IBD's Stock Of The Day, Soars 370% In One Year. It Could Climb Even More.

STRL

Investor's Business Daily

|

| Apr-14 | |

| Apr-14 |

Dow Jones Futures: What To Do As Nasdaq, Nvidia Win Streaks Hit 10 Days; ASML, Bank Of America On Tap

STRL

Investor's Business Daily

|

| Apr-10 | |

| Apr-08 | |

| Apr-08 | |

| Apr-07 | |

| Apr-06 | |

| Apr-06 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Mar-25 | |

| Mar-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite