|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Boyd Gaming currently trades at $80.83 and has been a dream stock for shareholders. It’s returned 337% since July 2020, more than tripling the S&P 500’s 96.3% gain. The company has also beaten the index over the past six months as its stock price is up 12.5%.

Is now the time to buy Boyd Gaming, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the momentum, we're sitting this one out for now. Here are three reasons why we avoid BYD and a stock we'd rather own.

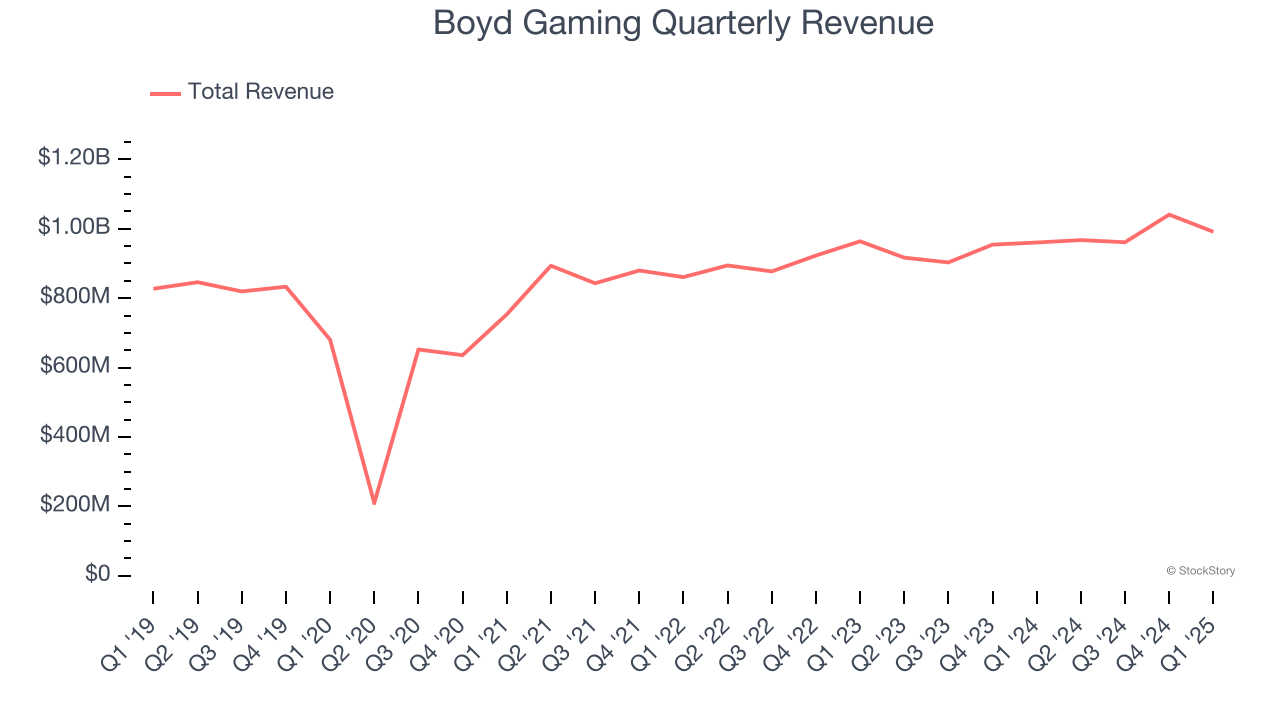

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Boyd Gaming grew its sales at a sluggish 4.5% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Boyd Gaming’s revenue to stall, a deceleration versus its 4.5% annualized growth for the past five years. This projection is underwhelming and implies its products and services will see some demand headwinds.

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Boyd Gaming historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 13.8%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

Boyd Gaming isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 12.6× forward P/E (or $80.83 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of our top software and edge computing picks.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Feb-19 | |

| Feb-15 | |

| Feb-12 | |

| Feb-12 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite