|

|

|

|

|||||

|

|

|

BILL Holdings BILL continues to gain momentum as transaction fee revenues increased 17% year over year to $252.1 million in the third quarter of fiscal 2025. This growth was largely driven by an 11% increase in Total Payment Volume (TPV), which reached $79.4 billion, reflecting rising payment volume and the company’s transaction-based income.

Growing adoption of BILL’s integrated financial operations platform, which served more than 488,600 businesses at the end of the fiscal third quarter, is positively impacting top-line growth. The platform processed 30 million transactions during the reported quarter, up 16% year over year. Enhanced offerings, such as Instant Payments, Local Transfer and Supplier Payments Plus, are expanding high-fee payment options and attracting larger enterprises to the network, contributing to stronger monetization and broader platform engagement.

While TPV showed solid year-over-year growth, BILL acknowledged some headwinds during the quarter. Customer spending came in slightly below expectations, resulting in a slight sequential decline in TPV and transactions per customer. However, this impact was partially mitigated by a favorable payment mix, as a greater share of high-margin transactions helped support monetization.

BILL’s long-term outlook remains constructive, driven by its continued investments in AI, ERP integrations and payment innovations, which are deepening user engagement and positioning the company for sustainable, volume-driven growth.

BILL operates in a growing, competitive fintech landscape, increasingly challenged by larger, more diversified players with deeper market reach.

Global Payments GPN offers a robust global merchant processing and software ecosystem, handling over 50 billion transactions annually. GPN excels in high-volume credit-debit payments and issuer solutions, largely through its TSYS and Worldpay platforms. GPN’s strategic acquisitions, strong cash flows and expansive global footprint position it for sustained long-term growth.

Meanwhile, Intuit INTU, with flagship products like QuickBooks and TurboTax, continues to expand into AP/AR automation. Intuit’s tightly integrated small business ecosystem, brand strength and ongoing investments in AI and user experience give it a compelling edge. Both GPN and INTU present formidable competition to BILL’s niche focus on SMB financial workflows.

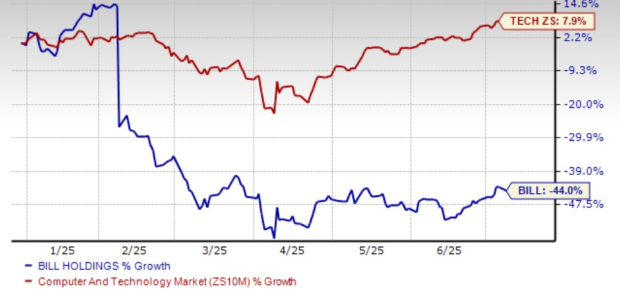

BILL’s shares have dropped 44% year to date, underperforming the broader Zacks Computer and Technology sector’s return of 7.9%.

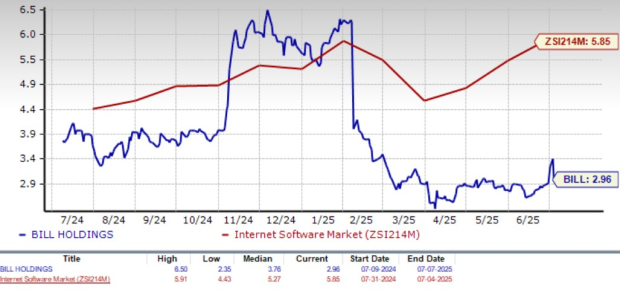

From a valuation standpoint, its forward 12-month Price/Sales of 2.96X compares with the industry’s 5.85X. BILL has a Value Score of D.

The Zacks Consensus Estimate for fiscal 2025 earnings is pegged at $2.07 per share, reflecting a 6.7% increase over the past 60 days. The earnings estimate reflects a 2.36% year-over-year decline.

BILL currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-15 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite