|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Las Vegas Sands LVS is doubling down on the premium mass gaming segment in Macau, positioning it as a central pillar of long-term growth. This strategic shift reflects evolving market dynamics, where the traditional base mass market has become increasingly competitive and less lucrative, especially as visitation patterns remain lopsided toward lower-spending day-trippers.

During first-quarter 2025, executives acknowledged a tougher operating environment in Macau, noting that opportunities in the base mass segment have narrowed. In response, LVS has been focusing on leveraging its top-tier assets, particularly the newly completed 2,400-room Londoner Grand, to attract higher-value customers. The premium mass segment has shown greater resilience and higher profitability, aligning well with the company’s upscale portfolio.

The pivot also involves greater emphasis on smart tables, side bets and tailored gaming experiences that increase player engagement and boost hold rates. Though EBITDA margins in Macau were under pressure this quarter, management expects improvement as revenues from the premium mass ramps up and the full inventory of the Londoner property comes online.

This approach is not without risks. The premium mass arena is becoming increasingly crowded and LVS must defend its share amid stiff competition. However, with scale, product diversity and luxury appeal on its side, the company appears well-positioned to capitalize on the segment’s long-term potential.

Ultimately, while short-term volatility in Macau may persist, LVS’ premium mass push could provide the foundation for durable growth, if execution keeps pace with ambition.

Two key rivals, Wynn Resorts WYNN and MGM China, a subsidiary of MGM Resorts International MGM, are also aggressively targeting the premium mass segment in Macau, intensifying competition for high-value customers.

Wynn Resorts has long been associated with luxury and VIP clientele, but is increasingly tailoring its offering toward premium mass players. Its refurbished properties in Cotai and premium-focused marketing campaigns position Wynn Resorts as a formidable player in this space.

Meanwhile, MGM China is expanding its premium mass footprint by enhancing floor space and product offerings at its MGM Cotai and MGM Macau resorts. The company has also leaned into digital tools and loyalty programs to deepen engagement with premium mass guests.

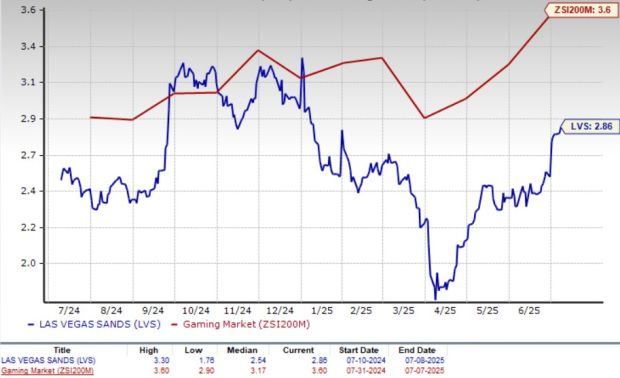

LVS’ shares have gained 15.6% in the past month compared with the industry’s growth of 7.6%.

LVS Price Performance

Despite the recent gain, LVS is priced at a discount relative to its industry. It has a forward 12-month price-to-sales ratio of 2.86, which is below the industry average.

LVS P/S (F12M)

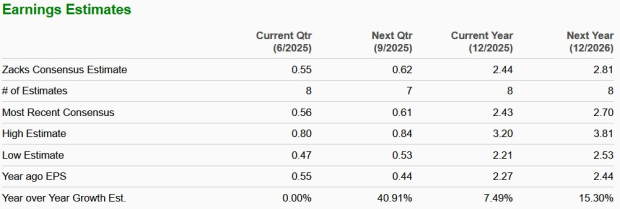

The Zacks Consensus Estimate for 2025 and 2026 earnings per share is pegged at $2.44 and $2.81, indicating a rise of 7.5% and 15.3%, respectively.

The company currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-14 | |

| Feb-13 |

Stocks to Watch Friday Recap: Applied Materials, Coinbase, DraftKings

WYNN +5.14%

The Wall Street Journal

|

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite