|

|

|

|

|||||

|

|

|

Astronics Corporation ATRO recently acquired Envoy Aerospace, a Federal Aviation Administration (“FAA”) Organization Designation Authorization (“ODA”) provider, in a deal worth $8 million. This move has enhanced Astronics’ position in critical high-demand areas like aircraft connectivity, in-seat power, and cabin modifications, as airlines invest in upgrades tied to connectivity and lease returns.

With ODA services in short supply, Envoy’s expertise gives Astronics a competitive edge by accelerating FAA approvals for Supplemental Type Certificates (STCs) and Parts Manufacturer Approvals (PMAs), thereby strengthening ATRO’s regulatory and certification capabilities.

As Envoy’s current programs continue under the Astronics umbrella, the company is better positioned to capture growth in aerospace retrofits and in-flight entertainment. For investors, this acquisition signals Astronics’ strategic expansion into high-margin, fast-growing aviation segments, potentially boosting its long-term value. This, in turn, might attract more stakeholders interested in aerospace stocks to add ATRO to their portfolio.

However, a prudent investor knows that a single acquisition, particularly one under $100 million, should not be the sole basis for making a significant investment decision. While the Envoy deal strengthens Astronics’ strategic positioning, it’s important to take a broader view. Let’s now delve into Astronics’ recent stock performance, potential growth drivers, valuation and any associated risks to make a more comprehensive and informed investment decision.

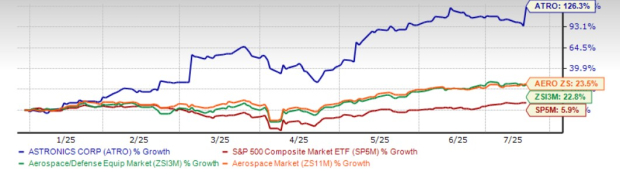

Astronics' shares have surged a solid 126.3% in the year-to-date period, outperforming both the Zacks Aerospace-Defense Equipment industry’s rise of 22.8% and the broader Zacks Aerospace sector’s gain of 23.5%. It also came above the S&P 500’s return of 5.9% in the same time frame.

Other industry players like Leonardo DRS DRS and Curtiss-Wright Corp. CW have delivered a similar stellar performance year to date. Shares of DRS and CW have surged 47.2% and 33.4%, respectively, in the said period.

As geopolitical tensions continue to rise, such as the ongoing conflicts between Russia and Ukraine, and tensions between Israel and Iran, global defense budgets are seeing a steady uptick. This has fueled growing demand for military aircraft and related technologies.

Astronics, which supplies mission-critical systems used in combat aircraft, has been benefiting from this trend. In the company’s last reported quarter, its military aircraft unit posted a robust 95% year-over-year sales improvement. With conflict-driven defense spending likely to remain strong in the near term, ATRO remains well-positioned to see continued momentum in its military aircraft business.

On the other hand, amid surging global air travel demand, airlines are expanding fleets and upgrading passenger experiences, driving increased demand for advanced cabin power systems and in-flight entertainment and connectivity (IFEC) solutions. This trend stands to benefit Astronics, which provides important commercial aircraft components like lighting and safety systems, electrical power and seat motion systems, aircraft structures and avionics products to the commercial transport market. Notably, this market’s sales are driven by increased new aircraft production and aftermarket airline retrofit programs.

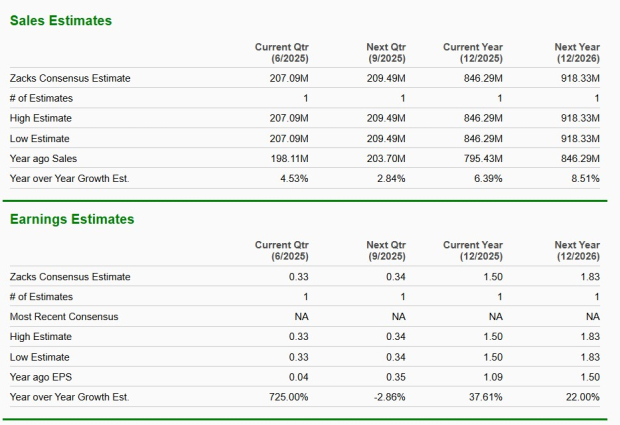

In line with this, ATRO’s near-term earnings and sales estimates, as mentioned below, reflect solid growth prospects for the company.

The Zacks Consensus Estimate for 2025 sales suggests year-over-year growth of 6.4%, while that for 2026 sales indicates an improvement of 8.5%.

The 2025 and 2026 bottom-line estimates also show a similar improving trend.

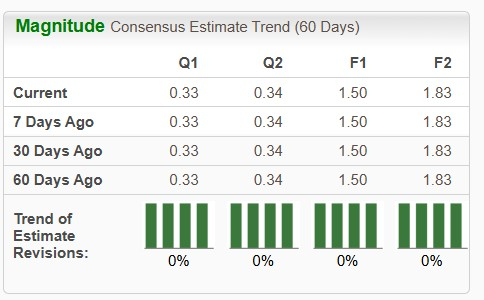

However, no movement has been observed in the stock’s near-term earnings estimates over the past 60 days, which reflects a wait-and-watch approach from analysts in terms of its earnings-generating capabilities.

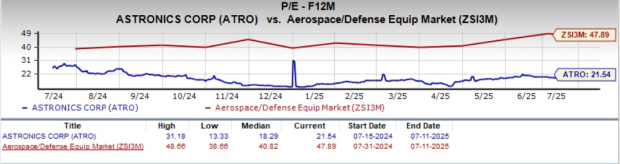

In terms of valuation, ATRO’s forward 12-month price-to-earnings (P/E) is 21.54X, a discount to the industry average of 47.89X. This suggests that investors will be paying a lower price than the company's expected earnings growth compared to that of its industry average.

Other industry peers, on the contrary, are trading at a premium to ATRO. While DRS is trading at a forward 12-month P/E of 40.31X, CW is trading at 35.93X.

The primary challenges that aerospace-defense stocks like ATRO, CW, and DRS continue to face include varying levels of supply-chain pressures stemming from the residual impacts of the COVID-19 pandemic, shortages of raw materials, cost increases, and a rise in labor costs and labor shortages, particularly for skilled labor.

Moreover, the recently imposed heightened tariff on the import of goods from almost all trading partners of the United States is likely to exacerbate the supply-chain challenge, which, altogether, might cause a delay in the delivery of finished products by ATRO. This, in turn, may hurt its operational results.

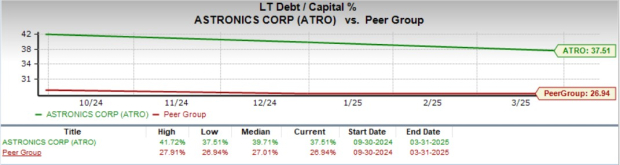

Further, Astronics is highly leveraged at the moment compared to its peer group, as reflected in its elevated long-term debt-to-capital ratio. This indicates the company’s increased reliance on debt financing, which may heighten financial risk, limit flexibility in capital allocation and affect the company’s ability to operate smoothly, particularly during economic downturns, thereby raising concerns for its investors.

To conclude, investors interested in ATRO stock should wait for a better entry point, considering its elevated debt levels, supply-chain pressures, and stagnant near-term earnings estimate revisions, which raise valid concerns.

However, existing shareholders might continue to retain this Zacks Rank #3 (Hold) stock in their portfolio, given its strong year-to-date performance, solid sales outlook and discounted valuation.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-26 |

This Defense Stock Is Resisting Market Weakness. Here's Where To Get In.

DRS

Investor's Business Daily

|

| Mar-26 |

Curtiss-Wright Holds Support, Eyes Entry Amid Defense Spending Boom

CW -5.19%

Investor's Business Daily

|

| Mar-24 | |

| Mar-23 | |

| Mar-12 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite