|

|

|

|

|||||

|

|

|

Serve Robotics Inc. SERV and Uber Technologies, Inc. UBER are both tapping into the fast-evolving autonomous delivery space, although their approaches diverge significantly. Serve Robotics is building a vertically integrated sidewalk robot delivery platform, while Uber is embedding autonomous vehicle technology through partnerships into its expansive ride-hailing and food delivery network.

The global autonomous delivery market is gaining momentum, driven by advancements in robotics, sensor technologies and AI-based fleet management systems. Per the report, the global autonomous last-mile delivery market is projected to reach $6.2 billion by 2030, driven by the rapid adoption of ground robots and drones across sectors like retail, logistics and healthcare. This growth is powered by rising consumer demand for faster, contactless delivery options and increasing investments in autonomous delivery solutions worldwide.

Serve Robotics is one of the few public pure plays in sidewalk delivery automation. Its autonomous robots are already operating in high-density urban areas, delivering food and goods on behalf of partners like Shake Shack Inc. SHAK and Mister O1. Meanwhile, Uber remains a dominant player in global mobility and food delivery and is exploring AV integration through collaborations with Waymo, Aurora and other tech providers.

Against this backdrop of rising automation and shifting urban logistics, both SERV and UBER offer unique value propositions. But the real question is: Which stock has a more compelling upside? Let’s examine the case for each.

Serve Robotics is executing a focused strategy to transform urban delivery through autonomous sidewalk robots. In the first quarter of 2025, SERV added 250 new Gen 3 robots to its fleet, bringing the total to more than 300. This expansion helped boost delivery volume by more than 75% quarter over quarter. Management expects second-quarter delivery volume growth to be in the range of 60-75%. New market entries like Miami, Dallas and soon Atlanta are helping expand the company’s geographic reach.

Beyond delivery, SERV is beginning to monetize its platform in new ways. The company has started generating recurring software revenues from licensing its autonomy and fleet management stack to partners, including a major European automaker and industrial robotics companies. The company also provided an update on its software and data platform, highlighting it as a core differentiator in its business model.

Its robotic platform — comprising advanced technologies for building and managing autonomous fleets — along with proprietary vehicle-generated data used to train AI models, continues to unlock new commercial opportunities. While still in its early stages, this diversification could significantly boost margins and reduce reliance on any single revenue stream over time.

Financially, Serve maintains a strong balance sheet with $198 million in cash as of the first quarter of 2025. The company raised $91 million earlier this year and chose to self-fund its 2,000-unit fleet buildout, eliminating roughly $20 million in potential financing costs through 2026. While still unprofitable (posting a $7.1 million adjusted EBITDA loss in the first quarter), SERV's operating leverage is likely to pave the path for improvement as utilization increases and high-margin software revenue scales.

Uber is rapidly solidifying its position as a key enabler in the autonomous vehicle (AV) space through a platform-first approach. The company is forming strategic alliances with leading AV firms, including Waymo, Aurora, May Mobility and Momenta, to drive growth. This partnership-driven model allows Uber to integrate cutting-edge AV capabilities into its global mobility and delivery ecosystem while maintaining a capital-light structure. In the first quarter of 2025, the company launched approximately 100 Waymo vehicles in Austin and reported solid feedback regarding the same.

Uber’s Delivery segment is also scaling profitably. In the first quarter, the company reported delivery incremental margins of 9%, driven by advertising revenues, an improved cost structure, and expanding contributions from grocery and retail. Membership programs like Uber One and merchant-funded promotions are helping Uber drive greater order frequency and stickiness.

On the innovation front, Uber is leveraging AI to optimize dynamic pricing, reduce insurance costs and enhance safety through driver behavior analytics. These efforts, combined with automation in support functions and customer engagement, are enabling Uber to grow profitably while improving service reliability and user experience.

Meanwhile, Uber’s AV ambitions are gaining real-world traction through scalable, cross-market deployments. While macro risks and regulatory scrutiny remain, Uber’s ability to scale both its core businesses and emerging automation initiatives positions it well for long-term growth. Uber is focused on unlocking growth in suburban and low-density markets.

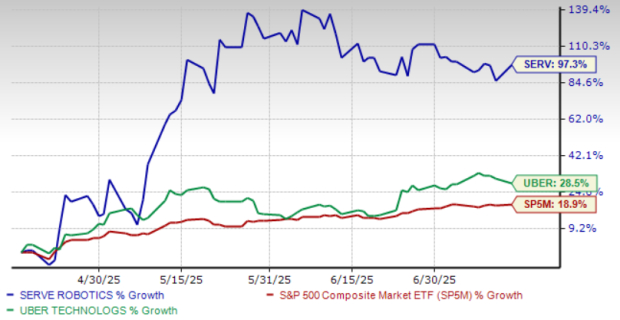

Serve Robotics stock has surged 97.3% in the past three months, significantly outpacing the S&P 500’s rise of 18.7%. Meanwhile, Uber shares have risen 28.5% in the same time.

SERV & UBER Stock Three-Month Price Performance

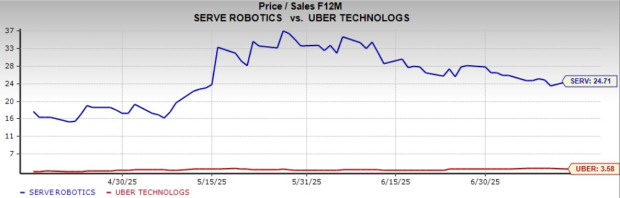

Serve Robotics is trading at a forward 12-month price-to-sales (P/S) multiple of 24.71, well above UBER’s forward 12-month P/S multiple of 3.58.

Uber Technologies appears to be in a stronger position than Serve Robotics at this stage owing to its mature operating model, global platform scale and disciplined expansion into autonomous vehicle integration. The company’s ability to leverage strategic AV partnerships while maintaining strong free cash flow and margin expansion reflects a high degree of execution maturity. Its diversified exposure across mobility, delivery, and logistics provides stability and long-term optionality as AV deployments scale.

While Serve Robotics is gaining traction in sidewalk-based autonomous delivery and beginning to monetize its platform through software licensing, it remains an early-stage player with a narrower market focus. The company’s rapid fleet expansion and early revenue streams are encouraging, but execution risks remain as it scales to new geographies and transitions toward recurring revenues. Its high valuation implies aggressive growth assumptions that may be tested in the coming quarters.

Uber’s global reach, proven profitability and partner-driven AV strategy provide it with a more robust foundation to navigate the competitive and regulatory complexities of the autonomous delivery space.

UBER currently carries a Zacks Rank #2 (Buy), while SERV has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite