|

|

|

|

|||||

|

|

|

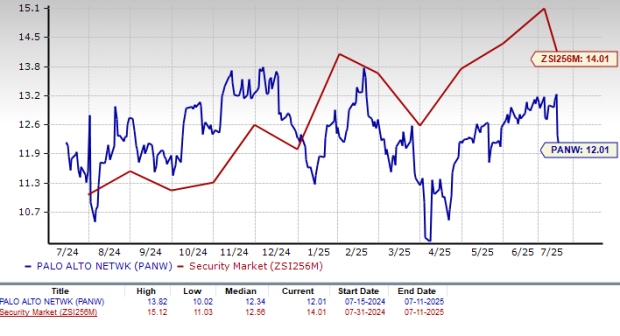

Palo Alto Networks, Inc. PANW is currently trading at a discounted valuation, making it an intriguing stock for investors to consider when deciding whether to buy, hold or sell. With a forward 12-month price-to-earnings (P/E) ratio of 52.56, PANW is significantly cheaper than the Zacks Security industry average of 102.75.

It also trades at a lower valuation compared to rivals, such as CrowdStrike CRWD, CyberArk CYBR and Zscaler ZS. Currently, CrowdStrike, CyberArk and Zscaler have P/E multiples of 117.61, 86.89 and 82.05, respectively. Palo Alto Networks’ forward 12-month price-to-sales (P/S) ratio of 12.01 is also below the industry average of 14.01, further reflecting its reasonable valuation.

The discounted valuation of Palo Alto Networks’ share price raises the question: Should investors buy, hold or sell PANW stock?

Palo Alto Networks is well-positioned to benefit from the rising demand for advanced cybersecurity solutions. According to Fortune Business Insights, the global cybersecurity market is projected to expand from $193.73 billion in 2024 to $562.72 billion by 2032, representing a massive addressable market. As cyber threats become more sophisticated, enterprises are increasingly prioritizing multi-layered security platforms, a trend that directly contributes to PANW’s strengths.

The company’s continued innovation in AI, automation and cloud security reinforces its competitive lead. Its strategic partnership with NVIDIA to develop AI-powered private 5G security solutions reflects its focus on next-generation technologies. This collaboration strengthens PANW’s capabilities in protecting data and networks in 5G environments, a rapidly growing market segment.

Moreover, Palo Alto Networks’ transition to a platform-based model has been a game-changer. By bundling multiple security products into a comprehensive cybersecurity platform, the company generates recurring revenue streams, boosting financial stability and customer stickiness.

PANW’s platformization strategy has enabled PANW to secure more than 90 net new platform deals in the third quarter of fiscal 2025 alone. On its recent earnings call, PANW also announced that its customers with multiple platformizations grew nearly 70% year over year, contributing massively to the top line.

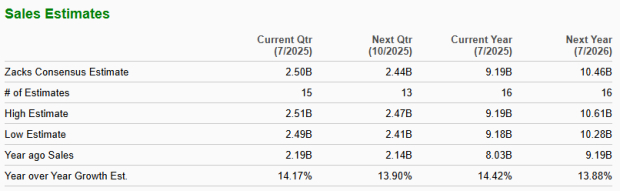

Despite a bright long-term prospect, Palo Alto Networks is experiencing a slowdown in its sales growth. Notably, the company’s revenue growth rate has been in the mid-teen percentage range over the past year, a sharp contrast from the mid-20s percentage in fiscal 2023. In the recently reported financial results for the third quarter of fiscal 2025, revenues grew 15.7% year over year. Also, in the first two quarters of the fiscal year, the growth rate had been around 14%.

The Zacks Consensus Estimate for fiscal 2025 and 2026 indicates revenue growth to remain in the mid-teen percentage range.

Another concern is the slowing growth of Next-Generation Security (NGS) annual recurring revenue (ARR), a key metric for Palo Alto Networks' long-term financial health. The company has reported five consecutive quarters of decelerating NGS ARR growth, with fiscal 2025 projections suggesting a further slowdown to 31-32% growth compared to the 45%+ growth in previous years. While this is still impressive, the decelerating momentum has disappointed investors, considering the rising demand for cloud security and AI-powered solutions.

Additionally, PANW is experiencing shortened contract durations and a slowdown in transition to PANW’s cloud-based artificial intelligence (AI)-powered platforms from its legacy platforms. Palo Alto Networks’ Cortex Cloud platform, which is a replacement for one of its key offerings, Prisma Cloud, is still in its early stages and has not yet achieved the scale necessary to optimize cost efficiencies, leading to PANW experiencing contraction in margin.

Moreover, PANW’s $1 million-plus deals are shifting from multi-year payments to annual payments, causing the shortening of the sales cycle and affecting top-line stability. These factors, along with the United States' stance toward China, Europe and other major economies related to tariffs, have kept the stock highly volatile in recent times.

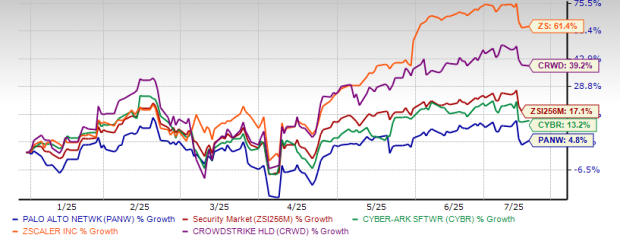

Year to date, shares of Palo Alto Networks have risen 4.8%, underperforming the industry’s growth of 17.1%. The stock has also underperformed its peers, including CyberArk, CrowdStrike and Zscaler. Shares of CyberArk, CrowdStrike and Zscaler have soared 13.2%, 39.2% and 61.4%, respectively, year to date.

Palo Alto Networks shares have dipped below their 50-day moving average, a bearish technical signal that indicates the potential for continued downward pressure in the short term.

Palo Alto Networks remains a leader in cybersecurity, with a strong long-term growth trajectory, continued AI-driven innovation and a shift toward a more predictable recurring revenue model. However, slowing revenue and NGS ARR growth rates suggest that near-term upside may be limited.

Despite these headwinds, Palo Alto Networks’ discounted valuation offers some downside protection. This discounted pricing makes PANW an attractive long-term hold, particularly for investors seeking exposure to cybersecurity growth at a fair price.

Currently, Palo Alto Networks carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Zscaler Earnings Top Estimates, Sales Outlook Slightly Above Views. Cybersecurity Stock Falls.

ZS +7.49%

Investor's Business Daily

|

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite