|

|

|

|

|||||

|

|

|

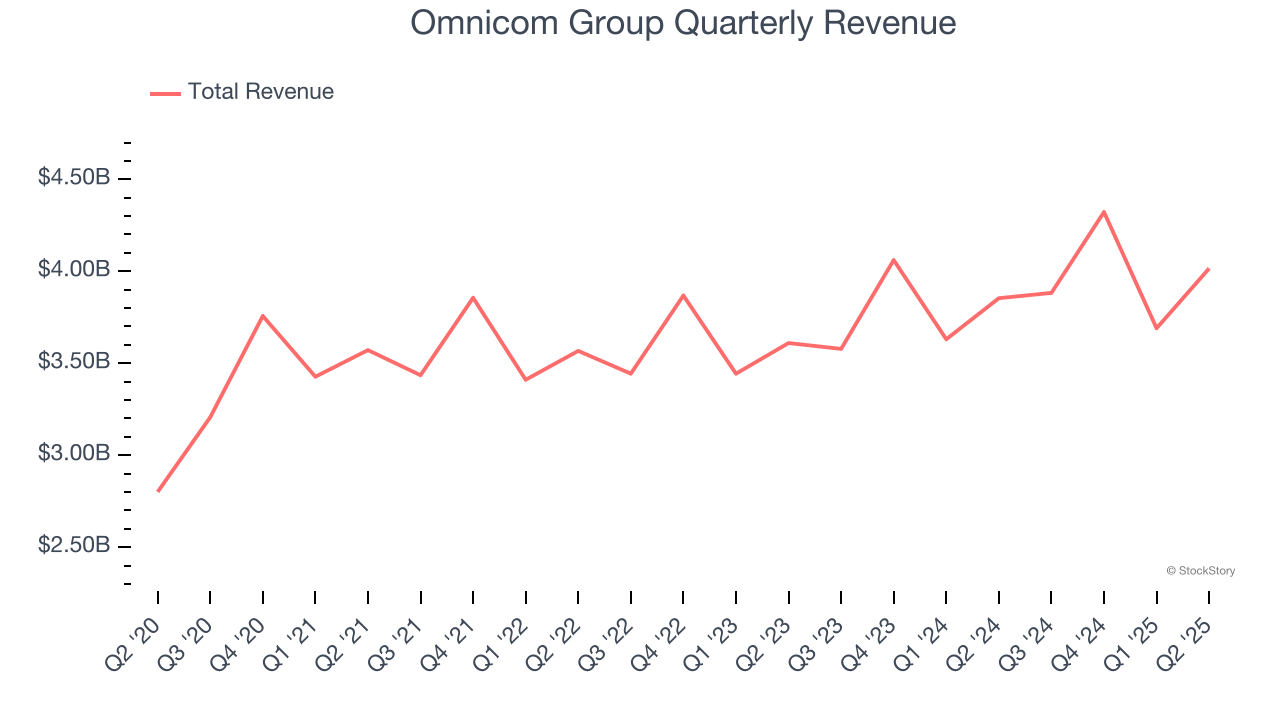

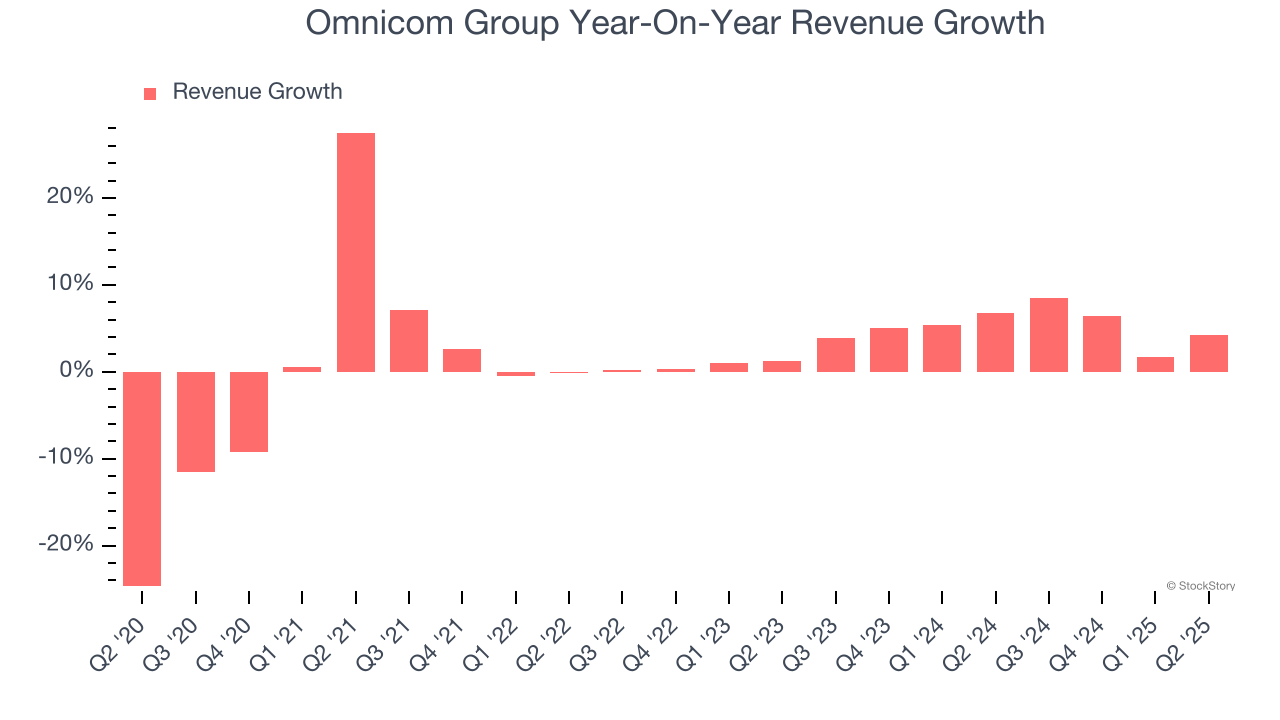

Global advertising giant Omnicom Group (NYSE:OMC) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 4.2% year on year to $4.02 billion. Its non-GAAP profit of $2.05 per share was 0.8% above analysts’ consensus estimates.

Is now the time to buy Omnicom Group? Find out by accessing our full research report, it’s free.

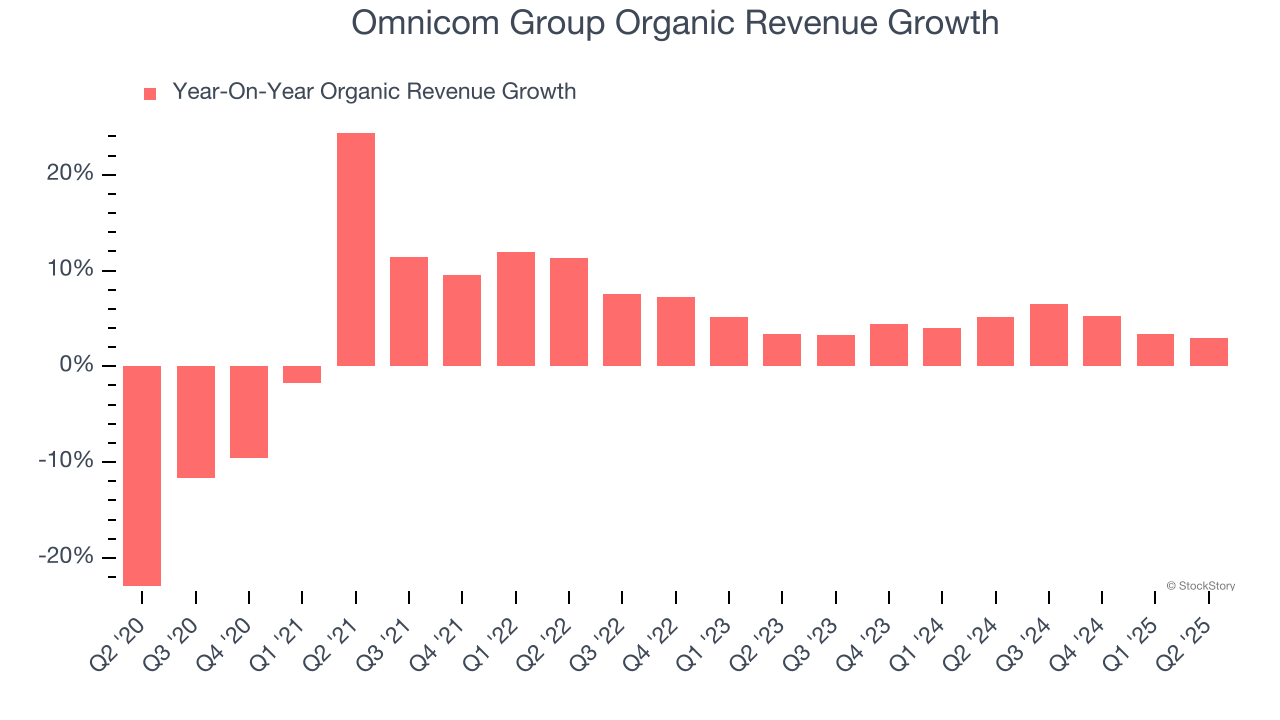

"We delivered solid 3.0% organic revenue growth this quarter even in the face of ongoing macroeconomic and geopolitical uncertainty - underscoring once again the resilience and agility of our business," said John Wren, Chairman and Chief Executive Officer of Omnicom.

With a vast network of creative agencies that helped craft some of the most memorable ad campaigns in history, Omnicom Group (NYSE:OMC) is a strategic holding company that provides advertising, marketing, and communications services to many of the world's largest companies.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $15.91 billion in revenue over the past 12 months, Omnicom Group is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To accelerate sales, Omnicom Group likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, Omnicom Group’s 2.6% annualized revenue growth over the last five years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Omnicom Group’s annualized revenue growth of 5.2% over the last two years is above its five-year trend, suggesting some bright spots.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Omnicom Group’s organic revenue averaged 4.4% year-on-year growth. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Omnicom Group reported modest year-on-year revenue growth of 4.2% but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 2.6% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

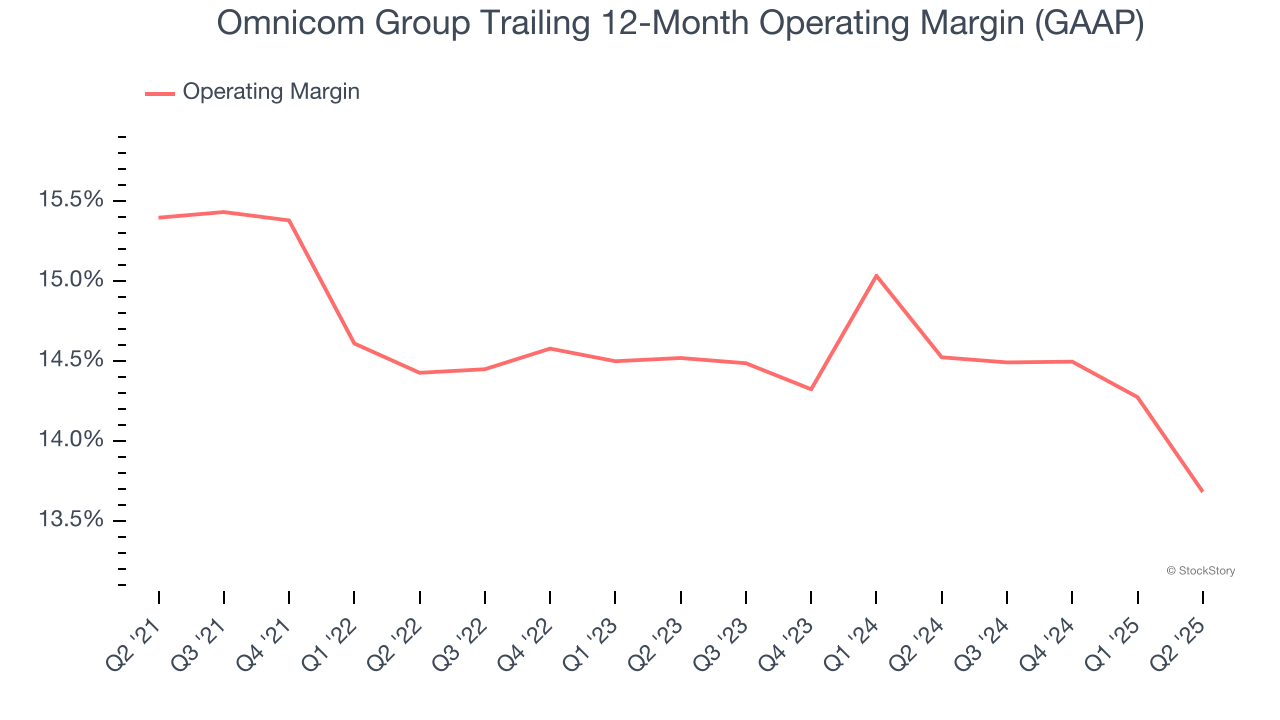

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Omnicom Group has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average operating margin of 14.5%.

Looking at the trend in its profitability, Omnicom Group’s operating margin decreased by 1.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q2, Omnicom Group generated an operating margin profit margin of 10.9%, down 2.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

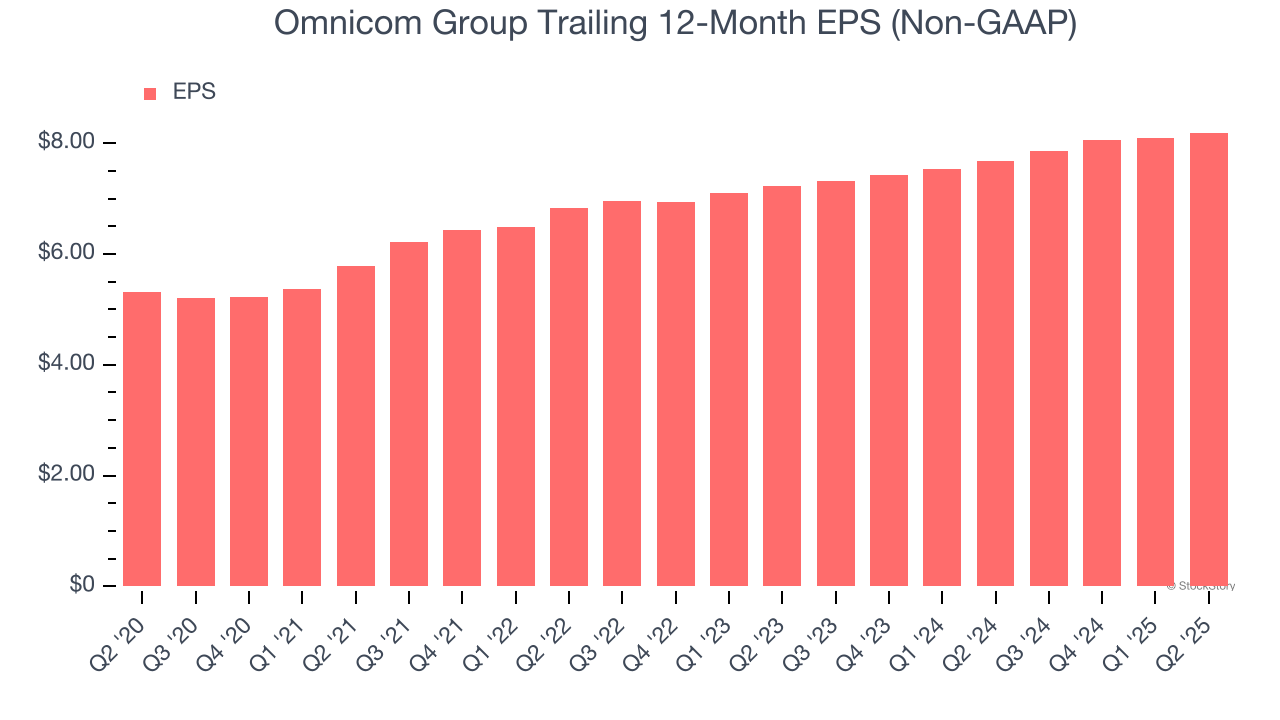

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Omnicom Group’s EPS grew at a solid 9% compounded annual growth rate over the last five years, higher than its 2.6% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

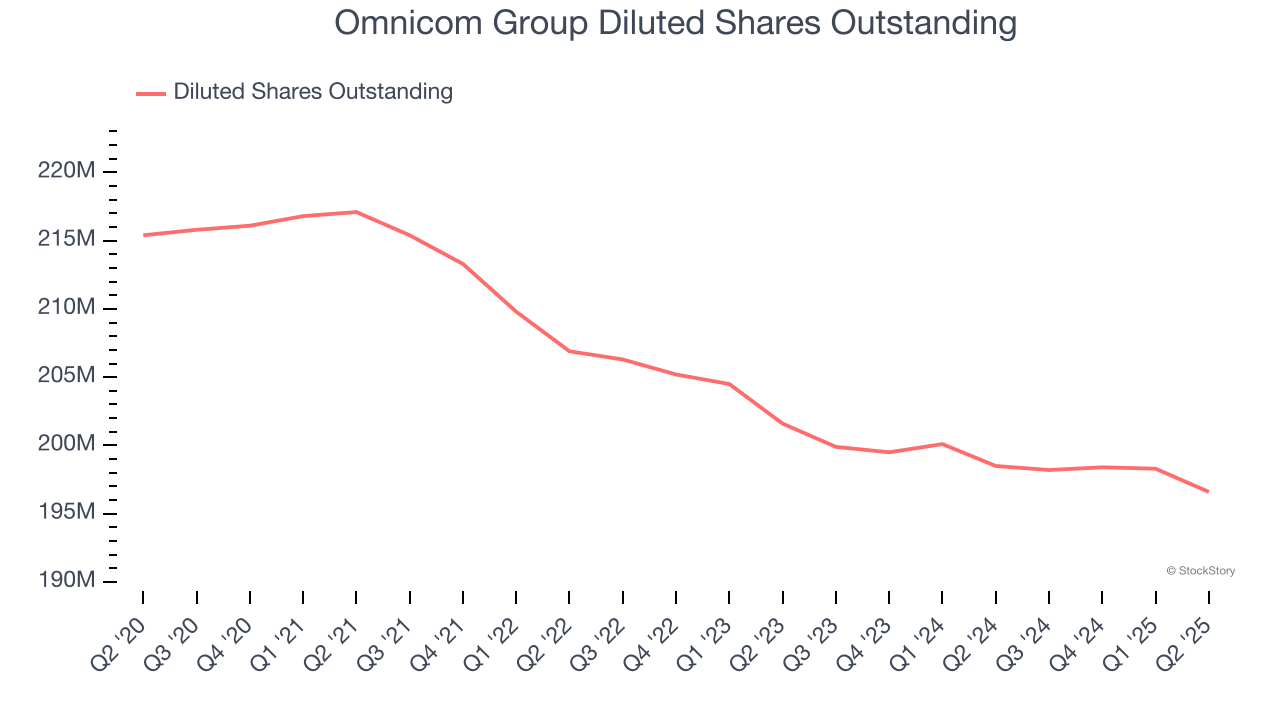

Diving into Omnicom Group’s quality of earnings can give us a better understanding of its performance. A five-year view shows that Omnicom Group has repurchased its stock, shrinking its share count by 8.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q2, Omnicom Group reported EPS at $2.05, up from $1.95 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Omnicom Group’s full-year EPS of $8.19 to grow 5.9%.

It was good to see Omnicom Group narrowly top analysts’ revenue and EPS expectations this quarter. On the other hand, its EBITDA missed. Still, this print had some key positives. The stock traded up 2% to $72.25 immediately after reporting.

So do we think Omnicom Group is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| 4 hours | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-04 | |

| Feb-04 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Jan-29 | |

| Jan-26 | |

| Jan-14 | |

| Jan-13 | |

| Jan-12 | |

| Jan-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite